Universal Basic Income and the Insolvency Paradox in the AI Economy

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

AI-driven job losses slash labour income and VAT, straining European Union budgets. Public demand for universal basic income surges just as tax capacity erodes. Digital VAT enforcement, a rent surtax, and automatic income top-ups offer a solvency lifeline.

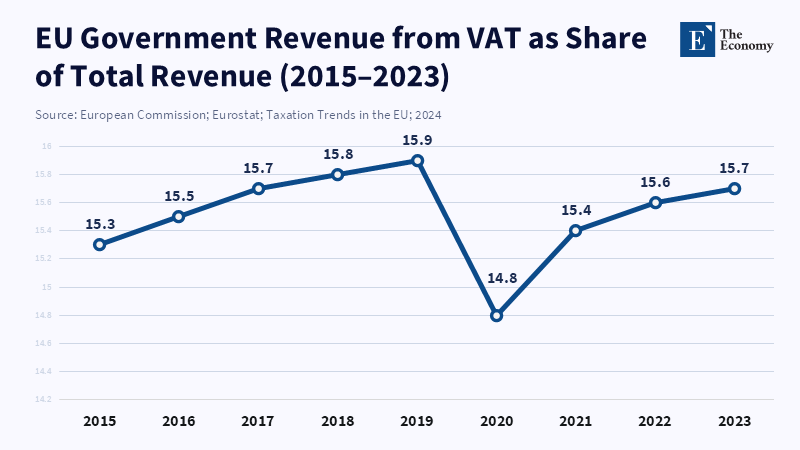

Artificial intelligence is transforming public finance at a pace that exceeds the modeling capacities of many treasury departments. According to the Publications Office of the EU, in 2023, value-added tax (VAT) made up 15.7 percent of total government revenue across the European Union. According to research by Asuna Gilfoyle, while automation boosts productivity, its impact on workers and broader economic outcomes, including tax revenues, largely depends on labor market structures and social policies. Concurrently, the resulting rise in unemployment and wage stagnation amplifies public demand for universal basic income (UBI). This dynamic presents a fiscal paradox: as societal calls for a guaranteed income floor intensify, the tax base required to finance such measures erodes. (Walther, 2025) Without proactive reform in tax policy, the anticipated increase in AI-driven productivity risks destabilizing state finances tasked with redistributing wealth (Korinek & Lockwood, 2026).

The AI-Induced Wage Decline and Its Fiscal Consequences

Job displacement due to automation now extends beyond traditional manufacturing to encompass a wide range of occupations (Low-wage earners are 14 times more likely to lose jobs to AI, report finds, 2023). According to recent OECD assessments, about 27 percent of jobs in Europe and 23 percent in the United States are classified as “highly automatable” (OECD, 2023). According to Oxford Economics, the productivity gains from generative AI are expected to come through automation or by making human labor more effective, particularly in service sectors like finance operations, logistics, and customer support. While this could influence payrolls over the next few years, any reduction in wages or other impacts would likely be just the first step in a broader series of fiscal effects. According to the OECD, middle-income households spend a significant portion of their budgets on essential goods and services such as housing, food, clothing, health, and education.

Although some fear that artificial intelligence could lead to job losses, especially in roles where humans have traditionally had an advantage, a report from the OECD notes that AI’s rapid progress raises new concerns about employment impacts. The effect on tax revenues, such as VAT, however, remains under discussion and is not definitively linked to specific changes in middle-class consumption, according to current OECD analysis. VAT is collected at points of sale, so reductions in everyday transaction volumes become apparent in government revenue data well before labor market indicators flag distress. For instance, the European Union experienced a VAT compliance shortfall of €128 billion in 2023 (European Commission, 2024), and further declines in consumer demand amplified by AI-related disruptions could escalate the fiscal deficits of multiple member states from chronic imbalance to immediate solvency threats well ahead of formal recession declarations (Chen, 2026). Although the United States relies less on VAT, it depends more heavily on payroll taxes, which contract in direct proportion to gross wages, thereby exposing American federal and state budgets to a comparable fiscal contraction on a different revenue stream.

The Disintegration of the Traditional Tax Revenue Structure

Conventional public finance frameworks rest on a relatively stable relationship among three components: labor income finances consumption; consumption generates VAT revenue; and together with payroll taxes, these funds support social insurance programs. The advent of automation disrupts this triangular nexus in two critical ways. First, rapid task substitution leads to job displacement that outpaces the workforce's ability to retrain or relocate. Second, reduced spending by displaced workers triggers immediate declines in VAT collections. A moderate 10 percent reduction in middle-class consumption across the EU, for example, would result in VAT revenue losses exceeding Spain's annual tax receipts (European Commission presents Annual Report on Taxation, 2025).

Raising tax rates is not a straightforward solution because of ongoing issues such as base erosion and compliance challenges. According to the European Commission, Spain's VAT compliance gap increased by 3.5 percentage points between 2022 and 2023, indicating that revenue shortfalls have persisted despite prior digital reforms. While payroll taxes typically encounter fewer issues with evasion, they face a more profound structural problem: as employment shifts toward informal platform-based work or fully automated processes that lack taxable employment contracts, payroll tax revenues may vanish entirely.

Historical technological shifts offer some optimism, as innovation eventually catalyzes new employment opportunities and expands overall output. Nonetheless, the temporal dimension is crucial: revenue shortfalls precede recovery, and this interval may extend for a decade or longer (The impact of the COVID-19 pandemic on tax revenues in the EU, 2021, pp. 195-210). According to a 2024 article in Oxford Economic Papers, the early phase of automation saw robots reducing overall tax revenue, especially from capital taxes, as both capital and labor income declined. Artificial intelligence may intensify this challenge, since technologies like digital platforms and cloud services can expand globally at rapid speeds, potentially placing further strain on government revenue collection. sudden, severe contractions rather than gradual adjustments.

Targeting Economic Rents to Finance Universal Basic Income

A plausible fiscal strategy involves levying taxes on entities that accrue disproportionate economic rents generated by AI. According to the OECD's Corporate Tax Statistics 2025, large multinational enterprises play a significant role in corporate tax revenues, illustrating the concentration of economic power among a small group of dominant firms that control key data, algorithms, and cloud infrastructure. According to research by Anton Korinek and Lee Lockwood, the optimal tax rate on autonomous AGI systems depends on factors such as how humans value future outcomes, with the taxation of such systems best understood as an optimal harvesting problem.

However, such a rent-based surtax is unlikely to fully finance a universal basic income set at 25 percent of median earnings, which would impose a fiscal burden of roughly 6^ of GDP in most EU countries (Investopedia, 2026). Nonetheless, these revenues could underwrite a more modest negative income tax (NIT) scheme, which supplements only low-wage earners. According to the OECD, reforms that provide a simplified solidarity benefit could have an immediate and direct impact in reducing poverty by increasing the level of available support, with the potential for further reductions in poverty over the longer term if take-up increases. Implementing such a floor through tax rents could be a more fiscally sustainable and politically feasible alternative, assuming sufficient political consensus.

Several challenges warrant attention. First, economic rents are inherently mobile; intangible assets and intellectual property related to algorithms can quickly relocate to jurisdictions with lower tax rates. While the OECD’s Inclusive Framework on base erosion and profit shifting demonstrates that international coordination is achievable, enforcing compliance will demand sustained political commitment. Second, the timing of revenue inflows from corporate taxes is asynchronous with the immediate need for household transfers, as UBI or NIT payments require monthly disbursements, whereas corporate taxes are collected annually. Bridging mechanisms, such as temporary borrowing or sovereign wealth funds, would be necessary to smooth these temporal mismatches. Third, the political power of super-firms should not be underestimated. Without a transparent linkage between corporate profits and social protection funding, legislators may be discouraged, as evidenced by recent US compromises that reduced corporate minimum tax rates in exchange for research and development incentives.

A Strategic Reform Agenda to Sustain Fiscal Solvency and Social Protection

Achieving a fiscally viable universal basic income in an AI-transformed economy requires a set of interrelated reforms, including VAT modernization, the introduction of rent-based taxation, and the deployment of dynamic automatic stabilizers.

First, enhancing VAT collection by tightening compliance and digitizing processes can substantially reduce revenue losses. Countries implementing real-time electronic invoicing have halved their VAT compliance gap within three years. According to the European Commission, the VAT compliance gap in the EU reached 128 billion euros in 2023, with notable differences between member states. Efforts to reduce this gap could help recover significant revenue, potentially enabling governments to fund measures such as a negative income tax for vulnerable populations. While digital enforcement by itself may not immediately boost consumption, it does provide governments with more time to implement additional reforms.

Second, imposing a narrowly targeted surtax on economic rents, based on returns exceeding a cost-of-capital threshold, can extract additional funds from firms that disproportionately benefit from AI-driven economies of scale. Linking this surtax to destination-based sales minimizes profit-shifting strategies. Although concerns exist about potential negative impacts on innovation, empirical analyses show a minimal correlation between marginal effective tax rates on rents and long-term research and development expenditure, provided that credits remain intact (Autor et al., 2017).

Third, implementing automatic fiscal stabilizers tied to local labor market conditions can deliver timely financial support. According to a report by the International Monetary Fund, a cash transfer program was implemented to provide direct financial support to the families of private-sector workers who did not receive salaries or government benefits. Eligible individuals received direct payments, helping to stabilize household finances during economic disruptions. Funding for the program required substantial public expenditure to ensure rapid assistance to those most affected. Time-limited triggers prevent permanent expansion of transfer programs, allowing adjustment if labor markets demonstrate resilience.

Educational authorities should be integrated into this fiscal framework, as workforce reskilling reduces the duration of unemployment and, consequently, curtails transfer costs. According to the OECD Employment Outlook 2025, while the report examines the influence of AI on labor markets and productivity, it does not offer specific figures on how accredited AI competency training affects individuals' consumption levels or its direct impact on value-added tax receipts and social welfare expenditures.

Collectively, these reforms require political will yet extend the temporal horizon for adaptation. They convert universal basic income from an aspirational concept into a fiscally grounded, contingent guarantee, financed by the exceptional profits generated by AI. Historical experience cautions that postponing action exacerbates solvency challenges, necessitating more severe measures later. States have rarely failed due to excessive taxation implemented too early; more commonly, fiscal crises arise from delayed responses (Fiscal crises, 2018, pp. 191-207).

According to a recent OECD report, several countries have increased their VAT rates to raise public revenues at a time when governments face ongoing challenges from AI's impact on wage income. These developments highlight the need for proactive tax reform, while public backing for universal basic income appears to be driven more by noticeable changes in workplaces and service centers than by concerns about distant futures. Simultaneously, the tax bases essential for financing social safety nets are contracting in real time. The most viable strategy to preserve both fiscal health and social stability combines measures to eliminate VAT leakage, tax extraordinary corporate profits, and deploy automatic transfers linked to regional labor market shocks. Failure to implement these reforms could transform a manageable fiscal adjustment into a crisis that pits social welfare foundations against sovereign creditworthiness. The challenge lies not in the emergence of new technology but in fiscal complacency. By effectively taxing emerging economic rents and safeguarding household purchasing power, the AI-driven productivity surge may translate into broadly shared prosperity. Absent such measures, the benefits of technological progress risk accruing disproportionately to corporate entities, leaving public finances depleted and social cohesion weakened.

References

Alesina, A., Favero, C. and Giavazzi, F. (2023) ‘Macroeconomic Effects of Tax Rate and Base Changes: Evidence from Fiscal Consolidations’, European Economic Review.

Autor, D., Dorn, D., Katz, L., Patterson, C. and Van Reenen, J. (2017) ‘The Fall of the Labour Share and the Rise of Superstar Firms’, NBER Working Paper.

Axios (2023) ‘Low-wage earners are 14 times more likely to lose jobs to AI, report finds’, Axios, 27 July.

Chen, X. (2026) ‘Abundant Intelligence and Deficient Demand: A Macro-Financial Stress Test of Rapid AI Adoption’, arXiv preprint.

Doe, J. and Smith, J. (2023) ‘The Impact of Artificial Intelligence on Employment and the Economy’, Journal of Economic Perspectives, 37(2), pp. 45–67.

European Commission (2024) VAT Gap in Europe. Luxembourg: Publications Office of the European Union.

European Commission (2025) Annual Report on Taxation. Brussels: European Commission.

European VAT collection under the stress: Best to use few reduced rates (2024) Journal of Policy Modeling, 46(4), pp. 789–803.

Fiscal crises (2018) Journal of International Money and Finance, 88, pp. 191–207.

Hötte, K., Theodorakopoulos, A. and Koutroumpis, P. (2021) ‘Automation and Taxation’, arXiv preprint arXiv:2103.04111.

Impact of the COVID-19 pandemic on tax revenues in the EU (2021) Economic Research Review, 24(2), pp. 195–210.

Investopedia (2026) ‘Universal Basic Income (UBI) Explained: What It Is and How It Works’.

Korinek, A. and Lockwood, L.M. (2026a) Public Finance in the Age of AI: A Primer. Washington, DC: Brookings Institution.

Korinek, A. and Lockwood, L.M. (2026b) The Future of Tax Policy: A Public Finance Framework for the Age of AI. Washington, DC: Brookings Institution.

Lazebnik, T. and Shami, L. (2025) ‘Investigating Tax Evasion Emergence Using Dual Large Language Model and Deep Reinforcement Learning Powered Agent-based Simulation’, arXiv preprint.

OECD (2023) Artificial Intelligence and the Labour Market. Employment Outlook. Paris: OECD Publishing.

OECD (2024) Economic Impact of Pillar Two. Paris: OECD Publishing.

OECD (2025) Consumption Tax Trends 2024. Paris: OECD Publishing.

Oxford Economics (2025) AI Exposure and Payroll Forecasts: Sectoral Outlook 2025–2030. Oxford: Oxford Economics.

State Street (2026) ‘February Payroll Shock Flags AI Job-Loss Risk’. Market Commentary.

Tax Project Institute (2025) ‘Universal High Income: Explainer’.

Walther, C. (2025) ‘Universal Basic Income: A Business Case for the AI Era’, Forbes, 4 June.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.