When Consumption Fades: AI Job Loss and the Coming Erosion of the VAT Base

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

AI job loss can reduce consumption fast That can shrink the VAT base and strain budgets Europe may face the pressure first

In 2023, value-added tax (VAT) accounted for 20.5% of total tax revenue across OECD countries. This observation is more than just a mere accounting detail; it indicates that in numerous advanced economies, a substantial portion of public finances depends on household consumption. Concurrently, discussions related to artificial intelligence (AI) tend to conceptualize labor market disruptions primarily as issues of skills or future productivity enhancement. This perspective is considerably narrow. The principal fiscal risk emerges early: if firms reduce their workforce in anticipation of productivity gains from AI, wage income may decline before productivity improvements are realized, output expands, or alternative tax bases are established to offset lost consumption revenue. This schedule sequence conveys significant implications for nations heavily reliant on VAT. The initial fiscal impact of AI-based labor displacement may not manifest as abrupt corporate insolvency or a sharp GDP contraction but rather as a gradual weakening of the taxable consumption base.

VAT Base Erosion as the Initial Fiscal Transmission Channel

Most discourse on automation begins and ends with labor employment market impacts: job losses, retraining efforts, firm restructuring, and eventual economic adjustment. However, governments depend not on long-run equilibria but on current revenue streams. This necessitates greater focus on the erosion of the VAT base. According to the OECD Economic Surveys: Australia 2026, household spending is influenced by factors like rising mortgage costs and changes in terms of trade, which in turn affect government revenues in countries that depend heavily on consumption taxes. The report does not address the specific impact of AI on fiscal revenues prior to changes in the production sector. As Brookings has noted, as AI systems generate increasing economic value and labor becomes a less accurate proxy for taxable capacity, relying exclusively on taxing human consumption may prove insufficient to sustain the state. This concern gains urgency once job losses begin to suppress current demand, rather than only in speculative long-term scenarios including artificial general intelligence (AGI).

Europe appears particularly vulnerable due to a convergence of two factors. First, VAT rates are comparatively high; OECD data from early 2024 indicate that 23 OECD countries imposed standard VAT rates of 20% or higher, 21 of which are European Union members (Consumption Tax Trends 2024, n.d.). Second, AI adoption is accelerating across European enterprises, with Eurostat reporting an increase from 8.0% in 2023 to 13.5% in 2024 among firms with at least ten employees, notably more prevalent among large firms (20% of EU enterprises use AI technologies, 2025). This combination—high VAT dependence coupled with rapid, uneven AI integration—exposes European public finances to fiscal risks if labor income declines. Consequently, it is imperative that Europe addresses AI not solely as a matter of productivity enhancement but also as a challenge to fiscal stability.

The United States confronts a similar demand-side challenge despite the absence of a federal VAT. The fiscal impact in the US will manifest as weaker state and local sales tax revenues, reduced income tax collections, and increased pressure on social transfer programs if AI suppresses hiring or wage growth. More fundamentally, tax systems predicated on widespread employment and consumption become precarious when economic expansion does not translate into proportional wage growth. The assumption that financial condition naturally follows technological development must be reconsidered. In an era marked by growth without commensurate employment gains, total output may rise while households' taxable capacity deteriorates.

Firms Respond to Anticipated AI Benefits Rather than Verified Outcomes

The fiscal concern intensifies when acknowledging that firms regularly adjust labor strategies in anticipation of expected AI-induced productivity gains rather than confirmed improvements. Unlike typical business cycles, in which employment changes follow firm-level adjustments, AI appears to precipitate earlier labor reductions. A January 2026 analysis from the Harvard Business Review documented instances in which firms implemented layoffs based on AI’s potential impact, with leading executives indicating that many white-collar roles could soon become redundant. This difference between anticipated and realized productivity is critical: management decisions based on expected efficiency gains may lead to hiring freezes and layoffs before productivity improvements appear in official statistics. For tax authorities, this temporal mismatch is significant, as revenue declines might emerge during a period when productivity gains have yet to materialize or are localized.

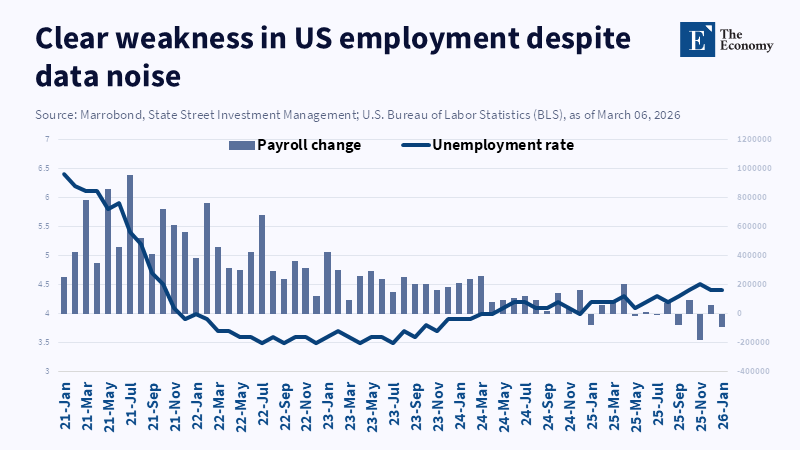

Current labor market observations offer some corroboration. According to Morningstar, the Bureau of Labor Statistics reported that nonfarm payroll employment in the United States fell by 92,000 in February, sharply contrasting with the 60,000-job increase expected, highlighting concerns about emerging softness in the labor market (Statistics, 2026). Similarly, commentary in Fox Business, referencing a CEO’s description of an “invisible layoff,” highlights employer perception of AI-powered shifts in hiring practices. Although these sources do not conclusively prove causal relationships, they jointly suggest that labor demand may be weakening as firms act ahead of measurable data.

This timing issue directly implicates VAT systems. If labor reductions occur based on anticipated AI efficiencies, government revenue from payroll-related taxes and consumption taxes declines immediately. However, compensatory gains may remain within corporate margins, investments, or financial markets rather than translate into increased household demand. Brookings has stressed the need for tax systems to evolve in response to an economy where value creation is less dependent on human labor. The fiscal vulnerability arises from the initial fragmentary onset of labor market shifts, which may strain public revenue even before comprehensive AI adoption unfolds. Thus, the absence of fully developed AGI does not preclude fiscal instability; partial anticipatory labor reductions can suffice to erode household spending power.

Europe’s Particular Exposure

Europe’s tax system amplifies its susceptibility to early VAT base erosion due to the structural prominence of VAT within public finance. OECD data point to the centrality of VAT to advanced economies and the high standard rates concentrated in Europe. Concurrently, Eurostat reports increasing AI adoption, especially among larger firms, which tend to have greater capacity for labor reductions. This twofold trend heightens fiscal exposure: enterprises best positioned to implement AI-driven workforce changes may see early declines in consumption tax receipts before these changes are reflected in GDP metrics. Europe thus faces a scenario in which advances in firm-level efficiency coexist with a contracting tax base underpinning social services.

The risk intensifies if income losses disproportionately affect low- and middle-income households, who generally allocate a larger proportion of their income to consumption than wealthier groups. Their spending adjustments occur more rapidly in response to wage declines, rendering the VAT base more sensitive than aggregate macroeconomic indicators indicate (Taxing Wages 2025, n.d.). Reductions in labor income do not merely impair individual welfare; they systematically depress taxable consumption in essential sectors such as food services, retail, transport, household goods, and local services (Labour income and productivity: OECD Compendium of Productivity Indicators 2023, n.d.). Consequently, governments confront simultaneous revenue shortfalls and increased demand for social support. The concept of “governing the age of unemployed growth” aptly captures this fiscal challenge, wherein declining consumption coincides with rising social needs.

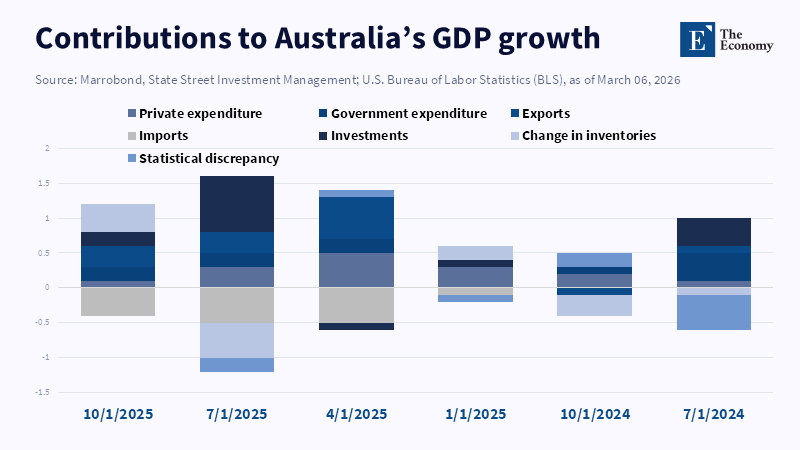

The second figure, illustrating Australia’s GDP growth components over time, reinforces this point. Positive headline growth can mask underlying shifts whereby public spending, exports, or investment compensate for weakening private consumption. Under such conditions, consumption-based tax systems become increasingly vulnerable (Global energy crisis and government responses drive a significant fall in tax levels in OECD countries, 2023). This reasoning extends beyond Australia, underscoring the need for policymakers to decouple growth metrics from fiscal resilience. During AI-driven transitions, economic expansion and the robustness of the VAT base could diverge, with output growth occurring alongside a contraction of the taxable consumption pool.

Anticipating Fiscal Challenges and Policy Responses

Reconciling VAT with its function as a revenue stream linked to labor income rather than a passive levy alters the policy imperative toward immediacy. Governments must avoid waiting for unequivocal, widespread unemployment before responding, as fiscal deterioration may already be underway. Near-real-time monitoring of indicators such as hiring freezes, reduced hours, wage stagnation, and consumption declines within VAT-sensitive sectors becomes essential. Additionally, diversification of revenue sources is necessary. Fiscal systems heavily reliant on mass consumption taxation become less sustainable as labor’s share of income contracts. Brookings suggests that tax frameworks have to adjust to evolving patterns of economic value accumulation rather than remain anchored in legacy tax categories. While this does not imply universal adoption of “robot taxes,” it calls for serious consideration of taxation approaches targeting concentrated corporate gains, capital income, and supernormal profits generated by AI.

This perspective also contextualizes the current debate in the United States over implementing a federal VAT. Critics highlight administrative difficulties and political opposition within a system distinguished by entrepreneurship, uneven state taxation, and concerns about price pass-through. These critiques are valid but also reveal a broader lesson: introducing a VAT is neither a panacea nor a guarantee of fiscal stability. The fundamental issue is that tax regimes designed around broad-based labor income and consumption struggle to maintain stable tax revenue when firms increase output without proportionate payroll growth. Within this context, consumption taxes risk becoming reactive indicators of fiscal stress rather than reliable revenue bases.

Accordingly, policy responses ought to prioritize strategic redesign rather than reactive measures. Short-term demand-stabilization policies, enhanced labor-market safety nets, and the investigation of alternative revenue sources—such as capital-gains taxes, levies on excess economic rents, or taxation of AI-induced profit concentration—will be necessary. The optimal combination will vary across national contexts. However, the key policy error is to frame AI predominantly as an innovation success, thereby neglecting the warning signs of a contracting consumption base. Initial VAT erosion may manifest subtly, through diminished spending, uneven tax receipts, and widening disparities between productive firms and fiscally constrained governments. By the time aggregate data confirm the trend, the fiscal structures established prior to widespread AI adoption may already be compromised.

References

Altus, K. (2026) ‘The invisible layoff: AI is quietly locking Americans out of the job market, CEO warns’, Fox Business, 6 March.

Brookings Institution (2026) Public finance in the age of AI: A primer. Washington, DC: Brookings Institution.

Brookings Institution (2026) The future of tax policy: A public finance framework for the age of AI. Washington, DC: Brookings Institution.

Davenport, T.H. and Srinivasan, L. (2026) ‘Companies are laying off workers because of AI’s potential—not its performance’, Harvard Business Review, 29 January.

Eurostat (2025) ‘20% of EU enterprises use AI technologies’, Eurostat News, 11 December.

OECD (2023) ‘Global energy crisis and government responses drive a significant fall in tax levels in OECD countries’, OECD News Release, 6 December.

OECD (2024) Consumption Tax Trends 2024. Paris: Organisation for Economic Co-operation and Development.

OECD (2025a) Revenue Statistics 2025. Paris: Organisation for Economic Co-operation and Development.

OECD (2025b) Taxing Wages 2025. Paris: Organisation for Economic Co-operation and Development.

OECD (n.d.) ‘Labour income and productivity’, in OECD Compendium of Productivity Indicators 2023. Paris: Organisation for Economic Co-operation and Development.

State Street Investment Management (2026) ‘February payroll shock flags AI job loss risk’, Weekly Economic Perspectives, 9 March.

The Unseen and the Unsaid (n.d.) ‘Why a value-added tax is the wrong fit for the United States’.

U.S. Bureau of Labor Statistics (2026) ‘Total nonfarm payroll employment down by 92,000 in February 2026’, The Economics Daily, 11 March.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.