The AI Job Shock Will Be Harder to Absorb Than the China Shock

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

AI can raise productivity without creating enough jobs to offset the losses Unlike the China shock, the AI shock may keep production at home while still weakening careers The real policy challenge is not just skills, but who captures the gains from automation

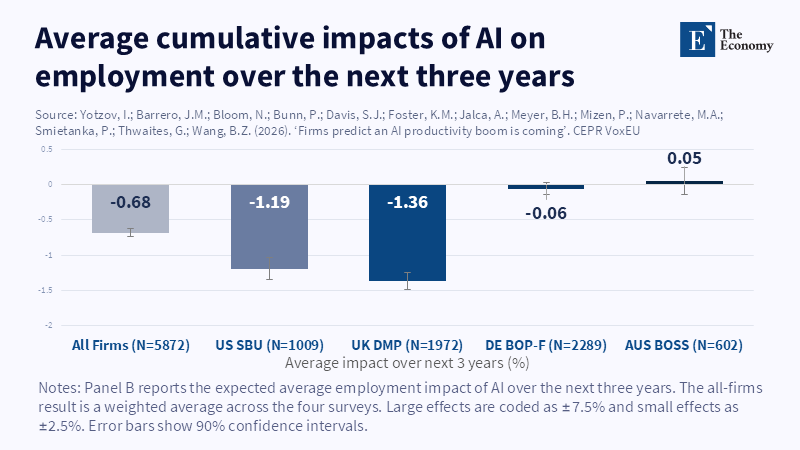

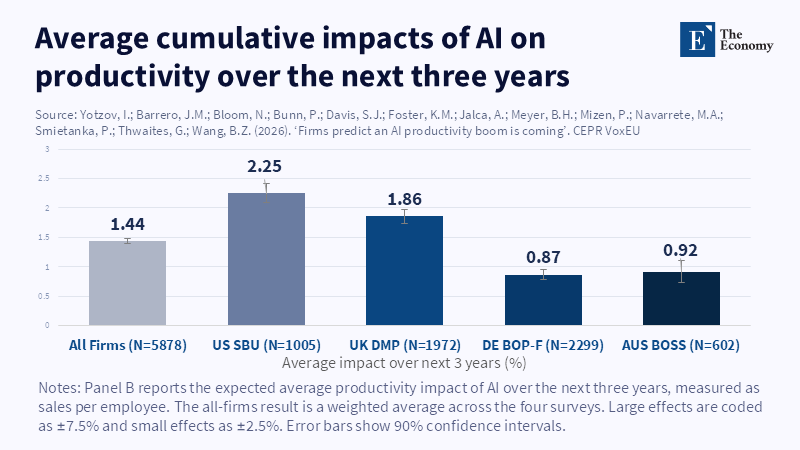

There is already a clear warning in the data about the upcoming disruption in the labor market. A large international survey of over 5,000 senior executives shows that, so far, artificial intelligence has had little impact on employment or productivity. According to the OECD, the impact of AI on productivity has been limited so far, which may explain why its effect on wages and employment has also been modest. For this reason, the coming AI-related job disruption should not be seen simply as another skills gap or a stage in digital modernization. Instead, it is better understood as a new kind of economic disruption that keeps production domestic and supports dominant firms, while leaving many workers with weaker bargaining power, fewer entry opportunities, and less secure careers.

The AI Job Disruption Differs from the China Shock

The AI job disruption differs from previous offshoring experiences. Both the trade shock from China and the AI shock start with productivity gains, but they affect the labor market differently. The China shock moved production overseas, where goods could be made more cheaply. Consumers benefited from lower prices, but many industrial communities lost jobs, wages, and confidence. Studies found that increased competition from China led to higher unemployment, lower labor participation, and reduced wages in affected local labor markets. Depending on the approach, Chinese import competition accounted for 20% to nearly 50% of the manufacturing job decline between 1990 and 2007. Some research even points to Chinese imports as a key reason for the broader decline in U.S. employment during the 2000s. The process was clear: factories closed, supply chains shifted, and entire regions faced economic damage.

In contrast, the AI job disruption is less visible because output often remains within the same firm, city, or country. For example, a logistics firm no longer needs to outsource overseas to cut planning staff if software can now manage scheduling and forecasting internally. Similarly, a law firm might retain work in-house by using AI for document drafting. This key difference alters the political landscape—winners and losers are geographically and organizationally closer. A recent study by Bloom and colleagues showed that regions with higher human capital, like large cities and much of the West Coast, experienced significant job shifts from manufacturing to services after the China shock, while areas with lower skills and greater dependence on manufacturing, mainly in the Midwest and South, saw far less job reallocation. According to the latest International Labour Organization index, about 25% of jobs worldwide are exposed to generative AI, and in high-income countries, this rises to 34%, with clerical work at the highest risk. Unlike the China shock, the effects of AI disruption are likely to be less geographically concentrated and more likely to impact office jobs, including those that previously served as entry points for graduates and junior staff.

The AI Job Disruption Benefits Firms Faster Than Workers

The AI job disruption tends to benefit firms faster than workers. One reason it can be underestimated is uneven adoption by businesses. By late 2023, only around 3.8% to 3.9% of U.S. companies reported using AI for production, though the rate was higher in information and professional sectors. This might seem too small to cause concern. However, individual workers have adopted AI tools far more rapidly. A representative U.S. survey in late 2024 showed that nearly 40% of adults aged 18 to 64 used generative AI to some extent, with 21.8% using it at work in the previous week. The technology is spreading before many companies have fully adjusted their jobs around it. This matters because labor market disruptions often come after AI use becomes entrenched in organizational practices rather than just experimental. Real change occurs when managers stop tinkering with tools and start redesigning workflows, staffing, and promotion systems around them.

Early productivity data is also concerning. Workers in the U.S. survey reported that generative AI saved them about 5.4% of work hours, roughly equating to a 1.1% productivity gain across the economy. Although preliminary, this shows labor inputs can shrink before national stats fully reflect the change. Another study in March 2026 of firms that had been using AI for over a year found average productivity improvements of 11.5% and a 4% net reduction in employees, with early-career roles most affected. The World Economic Forum adds that 40% of employers expect to cut jobs where AI automates tasks. This pattern highlights that businesses benefit before any social safety net catches up. Capital gains happen quickly, while workers are often told retraining alone will handle the rest.

Education Cannot Absorb the AI Job Disruption Alone

This is why treating the AI job disruption as a typical education issue is risky. Education remains important, but the skills challenge is less intense yet more unforgiving than many expect. OECD research shows most workers affected by AI won’t need deep technical AI skills. According to the OECD, while specialized AI skills are important in some roles, many AI-affected jobs do not require advanced expertise. Most workers need a solid understanding of how AI works, its strengths and limitations, how to verify AI-generated outputs, and how to effectively use AI alongside their own knowledge. But current training offerings are limited. Across Australia, Germany, Singapore, and the U.S., only 0.3% to 5.5% of training courses include AI content. So there are two problems: the system is slow to produce advanced specialists and also fails to give broad AI literacy, which is becoming as essential as reading or basic digital skills.

More importantly, education cannot recreate jobs that companies no longer want. The old idea was clear: learn new tools, climb the career ladder, and let technology increase your value. But AI threatens that ladder itself. Reducing routine entry-level work in fields like law, finance, design, software, and administration means fewer opportunities for young workers to gain judgment and experience. Therefore, the problem can’t be fixed by adding just one AI class or certificate. Schools and trainers must rethink their approach: create shorter, modular credentials, link training more closely with real-time labor market data, include more supervised projects, and focus on skills AI can’t replace easily—things like making judgments under uncertainty, communicating across contexts, building client trust, coordinating work, and spotting errors. Education still matters greatly, but it won’t be enough to absorb a labor-saving shock driven by firm choices rather than just a lack of skills training.

Policy Must Respond Before the AI Job Disruption Deepens

A better policy starts by rejecting the assumption that productivity gains alone will offset local and personal losses. The China shock showed job losses concentrated and communities weakened for years. Unemployment remained high for at least 10 years following major trade impacts. The AI shock might be more widespread, but the lesson remains: adjustment takes longer than expected, and market forces alone offer little comfort to those who lose career paths. Therefore, policymakers need more than reskilling funds. They should consider wage insurance, income support during transitions, portable benefits for workers on short-term contracts, and targeted hiring subsidies for young workers. Transparency also matters: companies claiming large AI efficiency gains should disclose how these affect jobs and early-career hiring.

People often respond by saying that while some jobs will disappear, new ones will appear. At a high level, this is true. The World Economic Forum predicts 170 million jobs will be created globally by 2030, with 92 million displaced, for a net gain of 78 million. But this doesn’t negate the disruption to AI jobs. It only shows that gross numbers can hide deep inequalities. New jobs don’t appear in the same places, at the same time, or for the same people as the ones lost. The China shock created national gains but local devastation. AI can do the same internally, enriching top firms and workers while hollowing out the middle of the career structure. The goal shouldn’t be to slow useful technology but to create a social agreement that prevents productivity growth from quietly shifting security, income, and bargaining power away from workers.

The initial warning remains valid. When firms predict that AI will increase output and productivity but reduce employment, policymakers need to recognize that the challenge is not just teaching people to use new tools. The deeper issue is who benefits when machines do more of the work. The China shock hurt places because production moved away. The AI shock can harm careers even when production stays put, making it subtler and, in some ways, more threatening. It might look like success in national economic figures while opportunities shrink inside firms, schools, and labor markets. Education systems should adapt quickly, but governments must do more than rely on schools to fix a structural shock after the fact. They should prepare for the reality that AI-driven job disruption involves power, bargaining, distribution, and the conditions under which a highly productive economy still allows people to build stable working lives.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Acemoglu, D., Autor, D., Dorn, D., Hanson, G.H. and Price, B. (2014) Import Competition and the Great U.S. Employment Sag of the 2000s. NBER Working Paper No. 20395. Cambridge, MA: National Bureau of Economic Research.

Acemoglu, D., Autor, D., Dorn, D., Hanson, G.H. and Price, B. (2016) ‘Import Competition and the Great US Employment Sag of the 2000s’, Journal of Labor Economics, 34(S1), pp. S141–S198.

AInvest (2026) ‘AI’s Real Enterprise Impact: Productivity Gains vs. Workforce Costs’. AInvest, 26 February.

Aldasoro, I., Gambacorta, L., Pál, R., Revoltella, D., Weiss, C. and Wolski, M. (2026) AI Adoption, Productivity and Employment: Evidence from European Firms. CEPR Discussion Paper No. 21082. Paris and London: CEPR Press.

Autor, D.H., Dorn, D. and Hanson, G.H. (2013) ‘The China Syndrome: Local Labor Market Effects of Import Competition in the United States’, American Economic Review, 103(6), pp. 2121–2168.

Autor, D.H., Dorn, D. and Hanson, G.H. (2022) ‘On the Persistence of the China Shock’, Brookings Papers on Economic Activity, 2021(2), pp. 381–476.

Bick, A., Blandin, A. and Deming, D.J. (2024) The Rapid Adoption of Generative AI. NBER Working Paper No. 32966. Cambridge, MA: National Bureau of Economic Research.

Bick, A., Blandin, A. and Deming, D.J. (2025) ‘The Impact of Generative AI on Work Productivity’. On the Economy, Federal Reserve Bank of St. Louis, 27 February.

Bloom, N., Handley, K., Kurmann, A. and Luck, P.A. (2024) The China Shock Revisited: Job Reallocation and Industry Switching in U.S. Labor Markets. NBER Working Paper No. 33098. Cambridge, MA: National Bureau of Economic Research.

Breaux, C. and Dinlersoz, E. (2023) ‘How Many U.S. Businesses Use Artificial Intelligence?’. America Counts: Stories, U.S. Census Bureau, 28 November.

Gardels, N. (2026) ‘How The AI Job Shock Will Differ From The China Trade Shock’. Noema Magazine, 16 January.

Green, A., Salvi del Pero, A. and Verhagen, A. (2023) ‘Artificial intelligence, job quality and inclusiveness’. In: OECD Employment Outlook 2023: Artificial Intelligence and the Labour Market. Paris: OECD Publishing.

Gmyrek, P., Berg, J., Kamiński, K., Konopczyński, F., Ładna, A., Nafradi, B., Rosłaniec, K. and Troszyński, M. (2025) Generative AI and Jobs: A Refined Global Index of Occupational Exposure. ILO Working Paper No. 140. Geneva: International Labour Office.

HealthManagement.org (2026) ‘AI Adoption Brings Productivity Gains and Job Cuts’. HealthManagement.org, 10 March.

Li, Y., Wan, Y. and Xie, S. (2025) ‘The employment effects of regional market integration: Evidence from China’, Journal of Asian Economics, 101, article 102053.

OECD.AI (2023) ‘AI-Driven Job Losses Threaten White-Collar Careers’. OECD.AI, 14 May.

Organisation for Economic Co-operation and Development (2024) Training Supply for the Green and AI Transitions: Equipping Workers with the Right Skills. Getting Skills Right. Paris: OECD Publishing.

Organisation for Economic Co-operation and Development (2025) Bridging the AI Skills Gap: Is Training Keeping Up?. Paris: OECD Publishing.

World Economic Forum (2025a) The Future of Jobs Report 2025. Geneva: World Economic Forum.

World Economic Forum (2025b) ‘Future of Jobs Report 2025: 78 Million New Job Opportunities by 2030 but Urgent Upskilling Needed to Prepare Workforces’. Press release, 7 January.

Yotzov, I., Barrero, J.M., Bloom, N., Bunn, P., Davis, S.J., Foster, K.M., Jalca, A., Meyer, B.H., Mizen, P., Navarrete, M.A., Smietanka, P., Thwaites, G. and Wang, B.Z. (2026a) Firm Data on AI. NBER Working Paper No. 34836. Cambridge, MA: National Bureau of Economic Research.

Yotzov, I., Barrero, J.M., Bloom, N., Bunn, P., Davis, S.J., Foster, K.M., Jalca, A., Meyer, B.H., Mizen, P., Navarrete, M.A., Smietanka, P., Thwaites, G. and Wang, B.Z. (2026b) ‘Firms predict an AI productivity boom is coming’. VoxEU, CEPR.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.