Taxing Algorithmic Wealth: Why the AI Age Demands a New Capital Levy

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

AI is shifting income from wages to profits and capital That will intensify wealth-tax, capital-tax, and AI-tax debates If governments wait, unemployed growth will weaken fiscal legitimacy

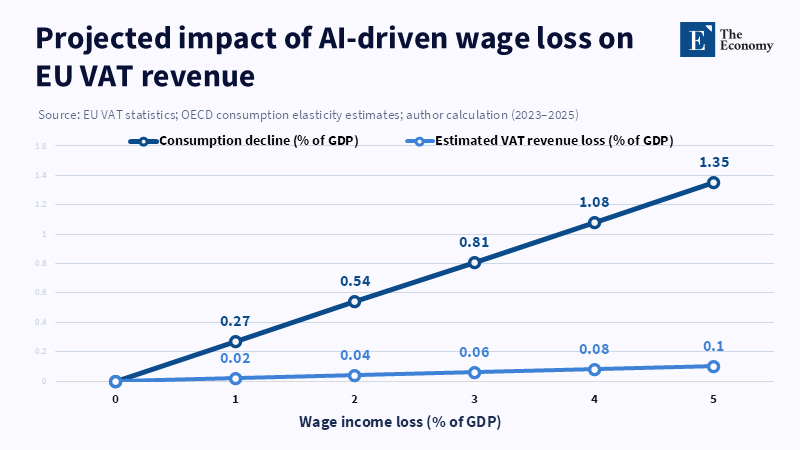

According to data compiled by Forbes, in 2025, the world’s 2,000 largest publicly traded companies generated nearly $4.9 trillion in profit on revenues totaling $52.9 trillion. This statistic is significant not only due to its magnitude but also because it reflects a major political realignment. Increasingly, economic gains attributed to the AI-driven economy are accruing to corporate balance sheets, intangible assets, and capital owners rather than to workers (Investment in Intangible Assets Surges, led by Funding for Software and Databases Amid AI Boom, 2025). When firms leverage algorithms, models, and automated systems to expand output without proportionally increasing their payrolls, the traditional fiscal equilibrium begins to break down (The Impact of Aging and Automation on the Macroeconomy and Inequality, 2021). The critical fiscal challenge shifts from solely protecting workers facing income loss toward determining how states should tax the disproportionate benefits flowing to firms and investors during labor displacement or compression (Tax Policy Reforms 2025, n.d.). Within this context, proposals for ultra-rich taxes, wealth taxes, capital taxes, or “AI taxes” do not emerge as marginal responses but as anticipated political strategies to address a novel distribution of economic power (French PM Bayrou and left-wing opposition determined to tax wealth of ultra-rich, 2025).

The Reemergence of Taxation Questions in the AI Economy

Throughout much of the twentieth century, advanced economies operated under a relatively broad fiscal framework in which firms employed labor, workers earned wages, households consumed, and governments taxed these income and expenditure streams. Although this model did not eradicate inequality, it established a wide social base for public finance. AI challenges this arrangement by enabling the scaling of output, coordination, and decision-making with diminished reliance on labor (Georgieva, 2024). Technologies such as generative AI systems, automated workflows, and increasingly sophisticated software agents can drive productivity growth without a commensurate increase in payrolls (Generative AI and the SME Workforce, n.d.). Consequently, a growing portion of income may shift toward profits, capital gains, and rents linked to data, computation, intellectual property, and platform economies.

Hence, discussions about AI and taxation should not be confined to simplistic slogans such as whether “robots should pay taxes.” Machines do not have legal personhood, which precludes direct tax liabilities, but this rhetoric persists because it echoes an underlying concern: the technological replacement of labor tends to centralize economic returns, placing pressure on governments to tax these gains more heavily (Gueorguiev & Nakatani, 2021). The essential question is not about taxing robots per se but about whether the abnormal profits arising from labor-substituting automation should continue to receive preferential fiscal treatment compared to the wages they supplant (Milmo, 2024).

This phenomenon is already evident in macroeconomic distribution trends. According to a recent IMF article, although the trend of declining labor share of income has been ongoing and capital returns have often recovered faster than wages after market shocks, AI may intensify this pattern by allowing leading firms to boost production while employing fewer workers. When this dynamic takes hold, the political rationale for taxation evolves. Citizens become less inclined to endorse a system that fully taxes labor income while allowing concentrated gains from automation, intellectual property, and financial wealth to remain relatively untaxed. Under these circumstances, arguments supporting wealth, capital, and AI-specific taxes begin to converge (Optimal taxation, minimum wage constraint in a model of capital-skill complementarity, 2025).

The Connection Between AI Profits and Wealth Taxation Politics

The case for revising the tax structure grounded in the advent of AI originates not primarily from public outrage but from fundamental political economy considerations. If AI enhances output while shrinking the labor-based income tax base, a greater proportion of taxable resources will reside in corporate profits, capital income, equity valuations, and concentrated private wealth. Existing tax systems, developed for industrial economies that rely on wage labor, may struggle to capture these returns equitably (Optimal taxation, minimum wage constraint in a model of capital-skill complementarity, 2025). This situation is expected to reintroduce complex debates that many governments have long eschewed: how to tax significant fortunes, excess returns, concentrated ownership, and winner-take-most capital configurations effectively.

Such issues are particularly salient in sectors characterized by the predominance of intangible and scalable assets. Proprietary foundational AI models, exclusive datasets, cloud infrastructure, and entrenched network effects often generate returns that resemble economic rent more than typical competitive profits. Current corporate tax regimes frequently struggle to tax these rents adequately, especially as firms engage in profit shifting, allocate intellectual property across jurisdictions, or arrange their operations in low-tax jurisdictions. As a result, substantial AI-related gains may accumulate in situations where the public sector captures only a limited portion (Base erosion and profit shifting (BEPS), n.d.).

This reality partly explains the resurgence of debates over wealth taxes and ultra-rich taxes in Europe and beyond. When voters observe a widening disparity between societal demands and the concentration of private wealth, they tend to support fiscal measures targeting the wealthiest (Fund, n.d.). Although not all wealth tax proposals are optimally designed—some impose excessive burdens on illiquid family assets, remain susceptible to avoidance, or fail to distinguish between productive investment and rent extraction—the general trajectory is unambiguous. As AI intensifies economic concentration, political demands to tax concentrated benefits are likely to grow correspondingly.

According to a 2025 OECD report, while tax policy reforms addressing excess profits, capital income, and net wealth are underway in many countries, the report does not specifically mention an "AI tax" as part of these broader movements. The political salience of the term derives from its explicit connection between taxation and automation-induced displacement. However, from a fiscal policy perspective, the more pertinent query is which tax instrument can most effectively reclaim AI-driven gains associated with concentration without impeding productive innovation.

Targeting Mechanisms for an AI Tax

A well-designed AI tax should avoid penalizing every firm that adopts new software technologies or indiscriminately taxing productivity improvements. Such an approach would be overly blunt. A more precise focus is on the segment of super-normal returns that emerges when automation decouples firm scale from labor input, allowing sustained high profit margins driven by advantages in data, computing resources, intellectual property, or market power (Automation and the Rise of Superstar Firms, 2025).

This leads to a design principle akin to a capital levy on extraordinary returns rather than a straightforward per-robot tax. According to the OECD, one approach could involve introducing an incremental surtax on returns exceeding a certain threshold, using measures such as profitability or return on invested capital to distinguish regular business earnings from unusually high profits, which are commonly linked to concentrated rents. The goal would not be to tax all investments at higher rates, but rather to recapture some of the gains that companies obtain through extensive use of labor-replacing automation, which the current tax system may not adequately address.

Executing such a system calls for complete anti-avoidance measures, requiring governments to confront issues such as profit shifting, intangible asset allocation, and multinational corporate structures. This discussion inherently intersects with systems such as the OECD’s global minimum tax and prior negotiations on digital services taxes. Lessons from these debates underscore that delays in policy responses facilitate artificial capital mobility, even though actual economic activity depends on public infrastructure, juridical frameworks, skilled labor, and community energy systems (Fund, 2018). An AI tax that ignores these challenges risks becoming ineffective.

Critics contend that imposing taxes on AI-generated returns could inhibit innovation, encourage corporate relocation, or depress investment. While these concerns justify careful consideration, their magnitude is often exaggerated. Leading AI companies tend to cluster within regions with dense networks of talent, infrastructure, financing, research institutions, and institutional stability—ecosystems constructed over decades through public investment (Venture capital investments in artificial intelligence through 2025, n.d.). Therefore, a transparent levy on extraordinary gains can be interpreted as a component of the social contract underpinning the innovation system rather than an antagonistic burden.

Moreover, a nuanced tax regime could differentiate between rent extraction and socially beneficial reinvestment. Firms allocating substantial resources toward worker retraining, cooperative research projects, public-interest data infrastructure, or broad dissemination of productivity-enhancing tools might qualify for tax credits or offsets (The Federal Research and Development (R&D) Tax Credit, 2026). Such provisions would align with fiscal policy aimed at distributing AI-related benefits more equitably, rather than merely extracting revenue after concentration.

The Political Dynamics Underpinning Rising Fiscal Pressure

The lasting relevance of this debate rests on democratic legitimacy. Fiscal systems serve not only to raise revenue but also to signal social values regarding beneficiaries, contributors, and the social contract governing technological change. Should AI adoption yield conspicuous advantages for shareholders, founders, and dominant firms while wage growth stagnates and job security deteriorates, pressure for redistribution will intensify and become difficult to deflect (Rockall et al., 2025). Under these conditions, proposals for wealth taxes, billionaire levies, capital gains surcharges, and AI-specific taxes are more likely to reinforce one another than to compete.

According to the OECD, the growing concentration of wealth among high-net-worth individuals and concerns about their comparatively low tax burdens have fueled political debates that increasingly call for taxing extreme wealth, windfall profits, concentrated capital, and gains from automation. While the terminology may vary, the expectation for tax systems to handle these issues is consistent. Citizens seek fiscal policies that address a technological context in which economic growth no longer guarantees widespread income inclusion. The more AI appears to enlarge private fortunes while diminishing labor’s economic role, the stronger the call for tax reform becomes.

Europe has particular significance in this debate, given its relatively advanced stage in political discussions concerning wealth taxation, social protections, and coordinated tax policies compared to the United States (Tax Policy Reforms 2025, n.d.). While Europe has yet to resolve the design issues involved, it is likely to be an early adopter of integrated wealth- and AI-based tax policies (Tax Policy Reforms 2025, n.d.). The changing dialogue will likely shift from questions of fairness to considerations of state capacity: how governments can finance adjustment programs, maintain legitimacy, and provide public goods when economic gains are concentrated more narrowly than under prior economic paradigms.

Consequently, timely policy intervention is critical. Delays in reform are likely to worsen political tensions, leading to countermeasures characterized by incoherence and social conflict. Historical experience indicates that postponement amid fiscal and social crises rarely produces nuanced reform, but rather precipitates hastily enacted policies and unstable political coalitions (Going to extremes: Politics after financial crises, 1870–2014, 2016, pp. 227-260). A carefully calibrated tax on AI-powered super-normal returns affords a more defensible and stable alternative to reactive, crisis-driven taxation.

Technological revolutions have historically compelled states to reconsider the taxation of wealth; AI will present comparable challenges (Rockall et al., 2025). The pivotal question concerns not the rhetorical appeal of the term “AI tax” but whether democratic institutions can adapt their revenue structures swiftly enough to prevent the concentration of machine-age wealth from undermining public legitimacy. Failure to do so will likely render demands for ultra-rich taxes, wealth taxes, capital taxes, and AI-specific levies an inescapable reality rather than theoretical constructs.

References

Brookings Institution (2025) The future of tax policy: A public finance framework for the age of AI. Washington, DC: Brookings Institution.

Brynjolfsson, E. and McAfee, A. (2025) The age of AI and the new economics of concentration. Cambridge, MA: MIT Press.

Chen, Y. and Ren, D. (2025) ‘Optimal taxation, minimum wage constraint in a model of capital-skill complementarity’, The Quarterly Review of Economics and Finance, 103, 102036.

Congressional Research Service (2026) The Federal Research and Development (R&D) Tax Credit. Washington, DC: Congressional Research Service.

Forbes (2025) Forbes Global 2000: The world’s largest public companies. Jersey City, NJ: Forbes.

Frøseth, T.M. (2026) ‘Taxing rents in the age of automation’, Journal of Public Economics, 241, 105219.

Funke, M., Schularick, M. and Trebesch, C. (2016) ‘Going to extremes: Politics after financial crises, 1870–2014’, European Economic Review, 88, pp. 227–260.

Georgieva, K. (2024) ‘AI will transform the global economy. Let’s make sure it benefits humanity’, IMF Blog, 14 January.

Gueorguiev, N. and Nakatani, R. (2021) ‘Sharing the gains of automation: The role of fiscal policy’, IMF Blog, 18 November.

Hötte, K., Somers, M. and Theodorakopoulos, A. (2021) ‘Technology and taxes in an automated economy’, Journal of Economic Behavior & Organization, 189, pp. 945–963.

International Monetary Fund (2014) Fiscal policy and income inequality. Washington, DC: International Monetary Fund.

International Monetary Fund (2018) ‘Policy responses to capital flows’, IMF News, 11 October.

Korinek, A. and Lockwood, L.M. (2026) Public finance in the age of AI: A primer. Washington, DC: Brookings Institution.

Lee, K.-F. (2024) AI 2041 and the economics of machine-scale production. New York: Currency.

Le Monde (2025) ‘French PM Bayrou and left-wing opposition determined to tax wealth of ultra-rich’, Le Monde, 11 February.

Milmo, D. (2024) ‘Balance effects of AI with profits tax and green levy, says IMF’, The Guardian, 17 June.

Nayebi, A. (2025) ‘An AI capability threshold for rent-funded universal basic income in an AI-automated economy’, arXiv, 2505.18687.

OECD (2020) Base erosion and profit shifting (BEPS). Paris: OECD Publishing.

OECD (2025a) Generative AI and the SME workforce: New survey evidence. Paris: OECD Publishing.

OECD (2025b) Tax Policy Reforms 2025: OECD and selected partner economies. Paris: OECD Publishing.

OECD (2026) Venture capital investments in artificial intelligence through 2025. OECD Policy Briefs, No. 50. Paris: OECD Publishing.

Rockall, E.J., Tavares, M.M. and Pizzinelli, C. (2025) AI adoption and inequality. IMF Working Paper 2025/—. Washington, DC: International Monetary Fund.

Stähler, N. (2021) ‘The impact of aging and automation on the macroeconomy and inequality’, Journal of Macroeconomics, 67, 103278.

Wang, Z., Li, X. and Chen, R. (2025) ‘Geography, compute and public infrastructure in AI cluster formation’, Research Policy, 54(7), 105001.

World Intellectual Property Organization (2025) ‘Investment in intangible assets surges, led by funding for software and databases amid AI boom’, WIPO Press Release, 9 July.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.