China’s Growth Model Has Reached the Reform Stage

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

China’s export-led growth model is reaching its limits Without structural reform, weak demand and labour strain will grow China’s next phase depends on stronger domestic foundations

Nearly one-third of that 5% expansion in 2025 came from net exports. That fact alone speaks volumes about the Chinese way of growing more than any slogan in any five-year plan. While last year net exports increased 1.6 percentage points on the year, private domestic demand remained weak, there was no inflation and the current account surplus widened to 3.3 percent of GDP. That is not a healthy second phase. It is evidence that China is still running on an old engine as its old edge diminishes. The real question now is not whether China will still be able to make more steel, batteries, cars, chips and machines to make machines. It can. It is whether the Chinese growth model will generate enough broad income, stable jobs and household security to substitute for the former miracle of exporting itself to prosperity. This is the reform phase China has reached. And now stasis is a greater peril than slip.

The reasons why the Chinese growth model is losing its old edge

The Chinese growth model still delivers solid headline productivity. In 2025, exports grew 6.1%, industrial output grew 5.9% and manufacturing value added was 34.7 trillion yuan, another quarter of GDP. And China's imports reached a historic 18.48 trillion yuan in 2025, ranking it the world's second-largest import market for the seventeenth consecutive year, according to the State Council Information Office. A healthy, late-industrializing economy should not be so reliant on the export engine while households breathe down its neck. It should cultivate stronger internal momentum. Instead, China appears to be great at utilizing the supply side and quite poor at cultivating final consumption inside the country's borders. That's the message. It's not that China is bereft of an industrial base. It's that the industrial base is doing more of the heavy lifting than the household component and that's a more unstable foundation for the coming decade.

That property slump made the earlier imbalance harder to mask. According to the IMF, housing investment shrank from 12.3% of GDP in 2020 to 6.1% of GDP in 2025. Official Chinese data show that the floor space of newly built commercial buildings sold in 2025 was 881.01 m2, 8.7% down from 2024. For nearly years, property did more than just carry China's construction boom. It boosted local finances, household wealth, employment, and consumer confidence. Once that pillar weakened, the authorities faced two options: move income and security toward households, so domestic demand can pick up, or intensify support for manufacturing, transport, and export competitiveness. Beijing largely chose the latter. This can keep the economy performing reasonably well for quite some time, but it does not address the demand problem. It pushes it on. A country can replace a weak property market with a bigger industrial base. It cannot replace weak households with more factories forever.

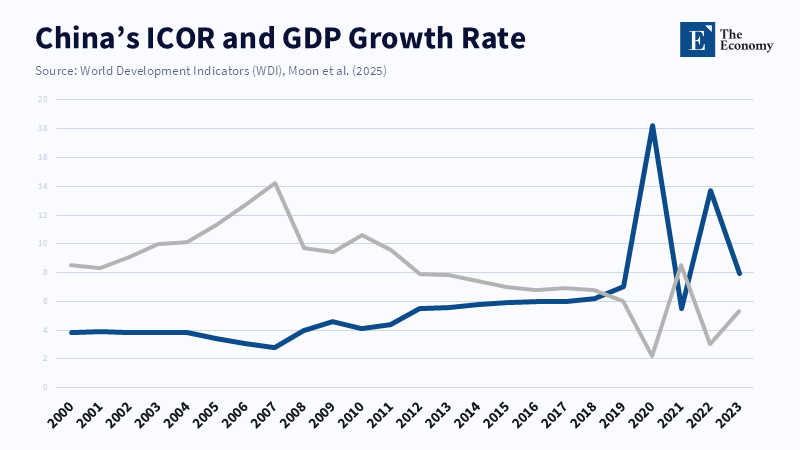

This is why the most common defense of the current strategy, which has to do with how fast China has been upgrading, makes the argument somewhat narrower. Yes, China indeed has been upgrading at a pretty rapid pace. Yes, the upgrades still matter somewhat for its power projection and, to a degree, for its productivity. But what doesn't yet matter enough to outperform the old growth model by a lot is the macroeconomy and the labor absorption it could bring. It turns out manufacturing accounted for about 24.7% of China's gross domestic product. In 2005, not for high-end manufacturing alone, which accounted for only roughly 6%. Context is important here. Those high investment rates, much higher than the world averages, are not necessarily a sign of technological failure. They are a sign of a rising nation with a strong, productive desire, but an excessively rebalanced demand. The danger doesn't lie in technological failure. The danger lay in creating an increasingly advanced version of the world's oldest story: excess supply, insufficient gains in household income and too much dependence on demand coming from outside.

Refiming Chinese growth model should begin at the household level

However, the second phase of the growth transition, which becomes popularly labeled as a shift to consumption, is a bit more nuanced. China does not need a Shopping Campaign; it needs a profound shift in security and income to households. The per capita disposable income of China, according to the China National Bureau of Statistics, in 2023 increased 6.3% over the previous year. This isn't a cultural flaw; this is a policy choice. Households would accumulate savings if they feel pension contributions are too low, health expenses are uncertain, education and housing are too costly and their future income is unstable, which makes cutting back on consumption not irrational, but defensive. Therefore, the demand problem in China isn't about belief signals, but about how risk is structured for ordinary households.

That argument is important because China does have a safety net, an extensive one, but it is often shallow in a way that fails to induce rebalancing. As explained in its report, given China's long, term growth and fiscal challenges, Phase 2024 of the retirement age reform set out by the IMF will be necessary; Ministry officials, however, expressed concern that benefits from the resident pension program would be a “little bit on the shallow side benefits are not high by international standards on average, while monthly pensions are modest in relation to rural per capita income. He added that the resident pension program today is enjoyed by more than 550 million people. By implication, the problem is not whether China has social policy; it's whether the social policy can be robust, portable and equitable enough to reduce precautionary savings nationwide. If the safety net is wide but shallow, it can't. It can prevent suffering from occurring, but it cannot yet engender the household trust that an enduring domestic demand model requires.

This is where the case for structural reform ceases to be a simple matter of equity. It becomes a case for growth. Raising social expenditure, particularly in rural China and accelerating urban reform of the hukou system, has the potential to boost consumption by as much as 3% of GDP in the medium term, according to the IMF. The World Bank restates this argument in much broader terms: higher social protection, a more attractive climate for business, a cleaner transfer of property rights and more sustainable urban finance. All of these are part of a more resilient demand base. That's the choice facing Beijing: whether it wants to continue to regard consumption as nothing more than the incidental output of industrial upgrading, or to view household security as a productive form of infrastructure. Only the latter can deliver a larger, internal market of the Chinese growth model on par with the weaker returns coming from exports and property.

The China growth model now faces a labor problem, not just a demand problem

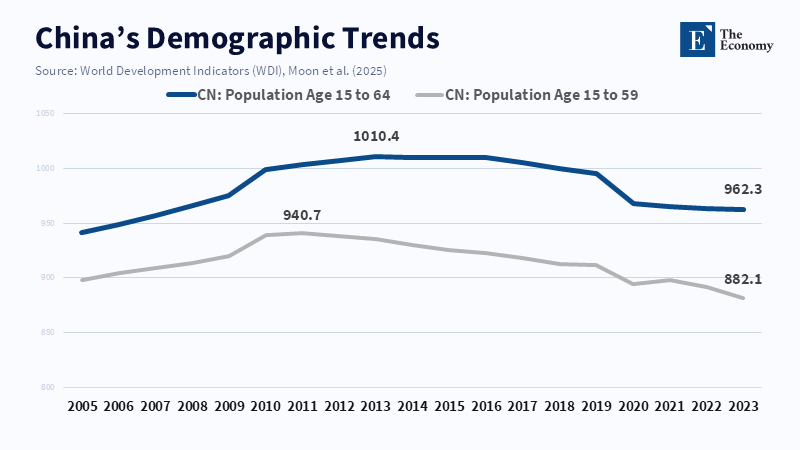

The long-term reason why reform can no longer wait is labor. China’s export model had thrived at an unprecedented scale when the country still enjoyed a huge demographic dividend, rapid urbanization, migrant inflows and a wide pool of cheap labor willing to enter factories. Such conditions are already in the process of ceasing to exist. The IMF projects medium-term growth will be even slower owing to a shrinking labor force, weaker return on investment and a slowdown in productivity growth. KIEP notes the working-age population has been shrinking since 2013. According to official Chinese government statistics, the total number of migrant workers reached 299.73million in 2024, an increase of 2.2million over the previous year and a sign of a steep slowdown when compared with previous decades. This means the conventional way of using the export industry to absorb excess labor is losing momentum just as China continues to lack an equally convincing substitute on the demand side.

Official headline unemployment rates can mask that. China's snapshot urban unemployment rate averaged 5.2% in 2025, which is not too bad. But the experience of young people is substantially worse. Data from the National Bureau of Statistics of China suggest that the urban unemployment rate was 5.1% in December 2025 and an annual average of 5.2%. Official figures did not include the unemployment rate for 16 to 24-year-olds other than students and those not in training. A growth model that modernizes production but puts young people in endless queues remains a fragile advanced model. It is a model with the distribution problem. It generates strategic capacity more quickly than it creates widespread employment and that is where the social stress begins.

This also informs the policy lesson for educators, administrators and labor planners. It is not an obvious solution to argue that more STEM intakes, more AI training and more high-end tech programs will alone cure the transition. Indeed, BigMacro data suggests China's urban youth unemployment rate excluding students was still at 16.9% as of November 2025, far above the overall rate. From this, it does not follow that the high youth unemployment and job, technology mismatch is merely a skills shortage problem, despite continued manufacturing reports of targeted occupation shortages. It is a manifestation of uneven demand. Training policy can assist, but cannot fix a macro model in which too much income circulates among producers and too little in the household. In this environment, education systems threaten to become holding zones for delayed entry into the labor force rather than pathways into stable employment. A more prosperous services sector, healthier local demand and more transferable insurance are just as relevant as more high-tech credentials.

China's Growth Model Reform Becomes the Pro, Growth Choices Now

None of this suggests that China is heading for a collapse and that is an important point. According to one IMF report, China's growth moderation is seen as structural rather than temporary, with predictions that if no major changes are implemented, the average annual growth rate could be expected to fall to around 3.8% during 2025 2030. The report does suggest that China still has the capacity for growth before the pace slows further, that it still retains policy capacity, and that it still has industrial depth that other countries would envy – but this is precisely where the issue of reform lies. Structural reform is easiest when the state still has resources, administrative control and scope to sequence change; it becomes much more difficult when tighter conditions of lessening growth, aging populations and increased trade friction limit options. The point is not that industrial policy should finish; it is that industrial policy without a more profound rebalancing will result in diminishing social and macroeconomic rates of return.

The other standard argument is that increased social expenditure or increased transfers to households would undermine competitiveness. This is the exact opposite of right. China's latest competitiveness problem is not that households are excessive consumers. It is that they are still too modest in consumption, which requires the overuse of the export sector and public or quasi-public investment to fill in this aggregate demand gap. OECD economists expect higher social transfers to help increase China's household consumption (often and more often), but also recognize that with the safety net so thin, savings must remain high. The IMF and World Bank, meanwhile, make a case for increased social safety nets and reforms in the hukou regime as a necessary (though possibly not sufficient) condition to reach a sustainable and more balanced growth trajectory. Simply put, higher security for households is not harmful. It is, in fact, an effective way to take off pressure to overshoot in the search for growth with excess supply, depressed prices and widening external surpluses. That is how a mature economy can guarantee both resilience and competitiveness.

Instead of congratulating ourselves that we have found the key, we should take this headline as a warning, not as a victory lap. Even according to the IMF, China experienced a much more moderate 5% growth in 2015, in part driven by exports. Structural reforms, which were once a side feature of Chinese growth, are now thrust front and center. China can make world-class sectors. It can pivot up the value chain. But the true challenge beyond comparative advantage is creating an economy capable of sustaining internal demand, cushioning displaced workers, channeling productivity into broad, based income and material well-being rather than ever higher output; transportable benefits, deeper hukou reform, resilient local taxation and more equal distribution of income by households. The country that internalized the production chapter is now challenged to master the social chapter. That is the real next step of growth.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

China.org.cn (2026) ‘China’s imports in 2025 hit record value of 18.48 trillion yuan’, China.org.cn, 14 January.

Garcia-Macia, D., Jain-Chandra, S., Kothari, S. and Xu, Y. (2026) ‘How China’s economy can pivot to consumption-led growth’, IMF News, 18 February.

Huld, A. and Zhou, Q. (2026) ‘China Manufacturing Tracker 2026’, China Briefing, 1 April.

International Monetary Fund (2026) People’s Republic of China: 2025 Article IV Consultation—Press release; staff report; and statement by the Executive Director for the People’s Republic of China. Country Report No. 2026/044. Washington, DC: International Monetary Fund.

Jin, K. (2026) ‘Can China grow from within?’, China-US Focus, 10 April.

King’s College London (2024) ‘The structural limits to China’s economic growth model’, China Week, 4 November.

Moon, J. (2026) China’s growth in transition: Structural shifts and medium- to long-term prospects. World Economy Brief 26-9. Sejong: Korea Institute for International Economic Policy.

National Bureau of Statistics of China (2026) ‘Statistical communiqué of the People’s Republic of China on the 2025 national economic and social development’, 28 February.

Saich, A. (2026) ‘Xi doubles down on state-led growth’, East Asia Forum, 12 April.

Xinhua News Agency (2025) ‘China’s migrant workers see steady income rise in 2024’, 30 April.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.