Physical AI Is China’s Next Two-Front War

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

China’s physical AI race is about reliable robot labor, not viral demos China has the scale and cost edge, as it did with EVs The hard test is quality, safety, and real factory use

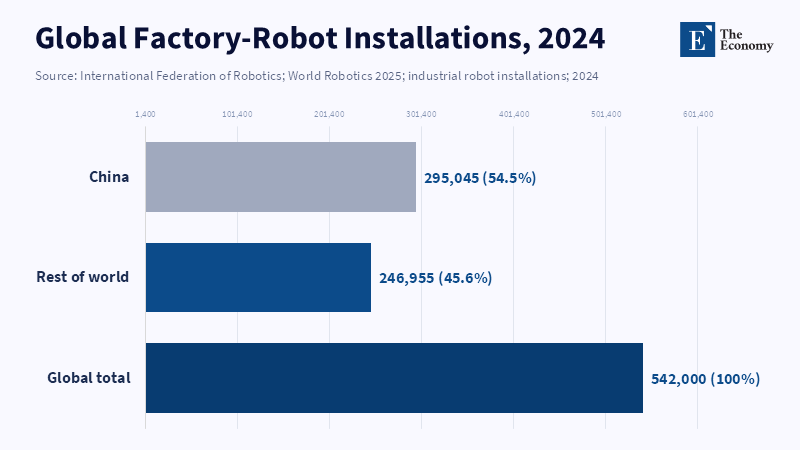

More than half of all industrial robots newly installed worldwide in 2024 went into Chinese factories. That single fact is more significant than any viral YouTube video of a human-shaped robot running at full tilt, dancing, pouring tea, saluting the troops. China is not starting its race for physical AI from the laboratory bench; it's starting from a world-class machine-building industry, with suppliers, factories, subsidies, engineers and buyers all in motion. And that is why the real challenge is the next one. Physical AI is not just a new app layer. It is AI that must lift, grasp, walk, sort, inspect, bear heat, evade humans, repair itself and prove ROI in real factories. China has demonstrated that it can win the efficiency war once a technology becomes practical to produce. It is yet to be proved that inexpensive humanoids can produce predictable work. The gap between them will determine the next industrial battle.

Physical AI: China's Third Test of Industrial Power

The more useful way to interpret the current Chinese push on physical AI isn't as a sci-fi tale of man and robot sharing a house, but rather as another form of industrial policy strategy, this time following batteries, electric vehicles, solar panels, telecoms gear, and semiconductors. The bet is simple: if AI is escaping from the screens and into the machinery, the nation that happens to make the machinery might win the market before the rules of the competition are written elsewhere. China's plan is to use physical AI to both accelerate its own economic growth and to consolidate a dominant supply chain position. One vision is factories with robots, robot suppliers, and standards that make a Chinese robot ecosystem essential. It's not whether a humanoid will wow in 90 seconds, but whether a Chinese company will be able to make motion translate into work the customer can afford to pay for.

Far more challenging than the electric cars game and more optimistic than the high-end chips story. In EVs, China harnessed large scale, its battery value chain, intense rivalry and a state umbrella to cut costs and develop capabilities rapidly. First, it mastered the mass production layer, then the software, design, charging infrastructure and export quality layers fell into place. For advanced chips, China's state-mandated ambitions hit a roadblock: While capital can finance the fab, it cannot replicate the complex processes of sophisticated lithography, yields, packaging and the faith of end users in killer AI silicon in the immediate future. Physical AI sits somewhere in between: it has an EV, like hardware trajectory, as its component parts (motors, batteries, cameras, castings and assembly) can be scaled up, but a chip, like performance constraint, as reliable labor requires accuracy, perception, safety and stable performance in chaotic environments

The timeline is also crucial. The simple growth phase of the EV market has been over for 5 years. Prices have reduced enough times to train people to expect more for less & the margins are slim. The free trade world is getting more & more protectionist. For the players who already have the core industries in batteries, motors, sensors, semiconductors, casting & software resources, physical AI just provides the next huge market to leverage all of their earlier EV infrastructures & investments. That is why the robot push is not only about robots. It is also about what happens when EV firms, battery suppliers and local governments search for the next market that can absorb their industrial capacity. A humanoid robot is a new product; it also means reuse & utilization of factory capacities, data systems, batteries, rising labor costs in the local society, government support, etc.

The Efficiency War Has Already Begun, Robots Are Not EVs

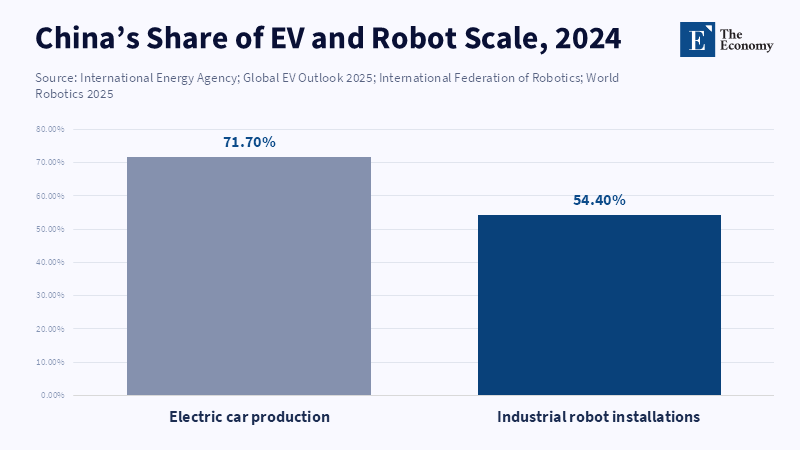

The efficiency war is within China's comfort zone. In 2024, In 2024, Chinese electric car sales exceeded 11 million, and EVs accounted for almost half of all car sales in China. Chinese factories produced 12.4 million electric vehicles in the year, a massive, more than 70 percent share of the entire planet. These figures help to understand the speed with which Chinese EVs transitioned from knockoff copies of global automobiles to world-class offerings. Volume-driven component costs are lower, making model overhauls faster and beating international rivals. The quality wasn't perfect, but it was good enough to reset customer expectations. Once consumers had the option of acquiring long-range, big-screen, spacious, cab, high-speed-charging vehicles at a sizable discount, the edge held by the premium brands vanished. This is the same playbook Chinese industrial robot manufacturers want to use when developing physical AI.

Early robot pricing trends point toward similar patterns. Unitree introduced the R1 humanoid at 39,900 yuan, at the edge of a significant reduction from the previous G1 model. Chinese robotics companies are moving fast from showroom pilots and early shipments into research, education, services and pilots for factory projects. The entire industrial robotics ecosystem in which they will participate already has an enormous footprint in China. There were approximately 2.027 million industrial robots operating on China's factory floors in 2024, with 295,000 new installations that year; local suppliers extracted a domestic market share of over half for the first time. This is important: physical AI will not be powered by a noble handful of genius products; rather, it will be powered by accessible joints, sensors, actuators, training fixtures, maintenance and spare parts. China is building that very costly ladder.

But robots aren't cars. Market success for a car depends on attractiveness, acceptable safety and a lower price than the alternative. But market success for a robot is in the context of each 24 hours. It has to generate enough revenue to cover its own costs during that timeframe. A cheap humanoid that constantly needs babysitting, constantly breaks down, freezes in different lights, or struggles to grip things at all is not cheap; it's a further management expense. Such a comparison provides a gross, order-of-magnitude range of its impact: 10,000 fully functioning humanoids would be less than a drop in the ocean of China's manufacturing workforce and robots already in operation. The first impact isn't going to be mass substitution of work, but its fragmentation, robots replacing limited, boring, dangerous and highly repetitive tasks in warehouses, electronics plants, car manufacturing facilities and inspection centers. That will happen first on a local basis, then nationally.

The Quality War is the Hard Part

It should therefore be noted that half-marathon stories should be read with some reservations. They show their engineering skills, their endurance and their speed, but none of them show readiness for factory work. Indeed, at the Beijing marathon of 2025, a robot runner finished the race in 2hr40min42sec. One year later, the Honor robot managed to run the same course in 50 minutes and 26 seconds, a stunning result. Around 40% of those robots were equipped with autonomous navigation, a measure of real progress. However, a marathon is a highly controlled task and has an evident goal. Moving a robot in a factory has many more small anomalies: a cable is curved, a tray isn't where it was expected, an employee is walking in front, an object is oily, a box gets ripped. A useful robot is one that can do more than move.

The quality war is a war over boring metrics. Uptime matters more than a viral clip. Mean time between failures matters more than a smooth expression. So does the number of human interventions per hour, battery life, safety certification, grasp success, repair time and the ability to work beside people without slowing them down. This is where Tesla, Xpeng, Unitree, UBTech, AgiBot, Boston Dynamics and many others are competing. Tesla wants to take the discipline of making electric vehicles and the AI training that goes with them and apply it to Optimus; Xpeng is trying to use the autonomous driving stack on a physical AI platform. The initial use cases for the Iron humanoid will be enterprise: factory, inspectors and work partners. The Chinese edge isn't so much in that every robot is on the cutting edge of technology, but that a lot of firms are experimenting, copying and cutting costs simultaneously.

The semiconductor warning still remains. China has not failed and given up on all chip endeavors: it has penetrated legacy and NAND chips; it has been able to substitute equipment and source locally; it has entered the domestic market. It is a different picture in memory with high bandwidth and, more radically, in AI with advanced computations. Yield, packaging, heat control, access to tooling and customer confidence are not solved in slogans. Nor can a physical AI be bifurcated in this way. All Chinese firms might end up flooding the globe with cheaper humanoids for school, trade fairs, light service and simple factory experimentation; yet those trusted to get real industrials would be those that could prove reliably scalable. This would still be an entrepreneurial enterprise, not a structural emulation of power. China's problem should not be one of failed moving robots but of failed low-margin service robots that never emerge as high-trust laborers.

What should the focus of Physical AI Policy be next? The right policy should be neither hysteria about losing jobs nor blind faith in automation. That means institutions for education and retraining should learn to prepare a robot,working workforce to live in a world of integrated production, rather than cling to a nostalgically preserved, robotless one. Colleges dedicated to education for the workforce and workforce agencies should see physical AI for what it is: a shop,floor,level system designed to be operated, maintained and managed by employees who will now need some skills, including understanding and collecting data, reprogramming robots and maintaining quality control systems. No administrator should use coding as the default career path for every student; many future entries into the workforce will be transitory and practical and involve being able to read diagnostic logs, refine work processes and maintain the safety of coworkers.

There is only one real option for policymakers. It is a measurement. Public funds should be directed away from demonstrations and toward costing,clocked tasks and robot cost and toward robot operation hours, between maintenance, frequency of robot downtime, the variety of objects it can manipulate, the programming time for each new task, the safety incident count and the length of the payback period. Policies should require companies to report this data in an accessible, standardized form. Procurement should support pilot programs in care facilities, ports, factories, logistics centers and hazardous environments, but only when those programs include countermeasures for human supervision, liability and worker retraining. A robot that replaces a dangerous lift is different than one that replaces a reliable job with unchanged output.

The first criticism will be along the lines of: "Sure, but this seems too risk-averse. The first criticism is obvious: if China waits for perfect quality, it may lose the market. But caution is not stagnation. It is how adoption becomes durable, but it also provides the basis for a sustainable customer base. Just as people bought EVs for the price and the range, managers will buy robots because they are performant in systems output and quantifiable risk. The game isn't between humans and machines, but between those economies that can best channel labor, data and hardware. China seems to have a sure shot in the first round of physical AI due to its cheapness and its mature industrial sector, but the second round will be unforgiving. If the latter is cheap, the former will be reliable.

The starting number is still the pivot. A country that now has 54 percent of the world's factory robots is already shaping the way forward. Yet physical AI is not install and forget. It will demand evidence. China's next great industrial leap will be no success unless affordable robots can prove themselves to be workers, not just moving machines. This will be the difference between a true revolution in industrial technology and just another export wind. The challenge is to measure the right things. Count fewer makeovers, more finish lines. Count less noise, more uptime, less ink, higher ROI. The ascendency of the physical AI industry will come not from the speediest robot, but the one that can work, fail, learn and clock on again.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Acemoglu, D. and Restrepo, P. (2020) ‘Robots and Jobs: Evidence from US Labor Markets’, Journal of Political Economy, 128(6), pp. 2188–2244.

Baptista, E. and Chen, L. (2026) ‘Humanoid Robots Race Past Humans in Beijing Half-Marathon, Showing Rapid Advances’, Reuters, 19 April.

Graetz, G. and Michaels, G. (2018) ‘Robots at Work’, The Review of Economics and Statistics, 100(5), pp. 753–768.

Hamlin, K. (2025) ‘China’s Chip Champions Miss Their Cue’, Reuters Breakingviews, 2 December.

International Energy Agency (2025) Global EV Outlook 2025. Paris: International Energy Agency.

International Federation of Robotics (2025) World Robotics 2025: Industrial Robots. Frankfurt am Main: VDMA Services GmbH.

Li, Q. and Woo, R. (2025) ‘China’s Unitree Prices New Humanoid Robot at Deep Discount to 2024 Model’, Reuters, 25 July.

Mo, L., Pan, C. and Potkin, F. (2025) ‘Chipmaker CXMT Plans Shanghai Listing with $42 Billion Valuation, Sources Say’, Reuters, 21 October.

Zhang, L. and Xing, Y. (2026) ‘Beijing Bets on Embodied Intelligence to Secure Structural Power’, East Asia Forum, 23 April.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.