Japan’s Hydrogen Gamble Is About More Than Decarbonisation

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

Japan’s hydrogen strategy is not just climate policy; it is a sovereignty bet Solar is cheaper today, but Japan fears dependence on China-led clean-tech supply chains The real task is to expand renewables while keeping hydrogen only for sectors where it can truly cut emissions

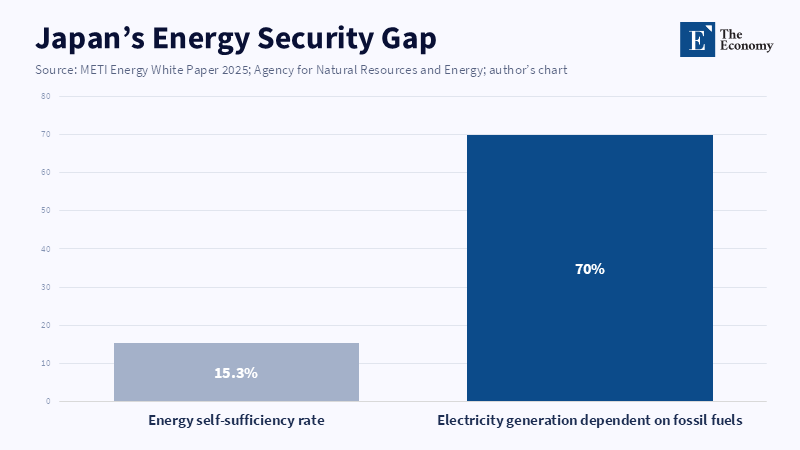

Japan's energy problem is illustrated by one stark figure: 15.3%. Its energy self-sufficiency rate for FY2023. This was the lowest in the G7. This means Japan still depends on imported energy for most of the fuel that keeps its factories, trains, data centers and homes running. Japanese energy policy therefore, is not simply climate policy, but national power policy. This also helps explain why the Japanese hydrogen strategy is something more than a rejection of cheap solar power. The hydrogen strategy can be seen as a gamble, as a high-risk, high-reward response to the dilemma: Solar is cheap, fast, and predictable, much of the solar supply chain is dominated by China and solar implies reliance on an adversary; hydrogen is expensive and unpredictable but implies a chance to build a domestic industry and reduce reliance on both imports of fuels and imports of know-how.

The Japan hydrogen strategy is a sovereignty bet

Standard criticism holds that Japan is placing too much strategic weight on hydrogen and ammonia, while solar is cheap and available. That critique is fair. It is also incomplete. The Japan strategy is about more than climate: it is about industry, trade, the grid and national identity. The dilemma is not perfect hydrogen versus perfect solar; the dilemma is a choice between kinds of reliance, between an inability to provide our own fuel or a loss of the capability to design and manufacture our own energy systems, especially from China. This is the logic of the strategy.

This is the crucial mind-shift. It is not that Japan isn't committed to the fight against climate change-it is; but instead is trying desperately not to become the passive buyer of the next round of Asian industrial growth. The revolution in solar manufacturing was won by China, and the supply chain in batteries also resides largely in China. Korea still competes aggressively in the business of high-end manufacturing in the battery, fuel cell, ship and advanced clean industry sector. In Japan's case, a post-war manufacturing powerhouse, the political cost of handing over the high-end part of energy systems to either China or Korea is substantial, immeasurable in yen per kWh. The logic might escape a spreadsheet, but it is politically comprehensible in a cabinet room.

The stakes are so high that it's a sovereignty strategy. Japan's recently revised strategy calls for use targets for approximately 3mt H2 by 2030, 12 mt H2 by 2040 (including ammonia) and 20 mt H2 by 2050. There are 15+ trillion Yen committed in public and private funds over the next 15 years to the hydrogen and ammonia supply chain. The Hydrogen Society Promotion Act 2024 offers approved projects 15 years of price gap support, plus an additional 10 years of supply security; it's not an incremental incentive for a niche fuel; it is an enduring state strategy for an industry that has yet to materialize.

Solar is cheaper, but dependence is the hidden price

The strongest criticism of the Japanese hydrogen strategy is its reliance on existing solar capacity. Solar is not fringe; it is mainstream. Global PV capacity already exceeds 2.2TW and more than 550 GW was installed in 2024. Japan's solar capacit, is growing too. Renewables accounted for about 26.7 percent of Japan’s electricity generation in 2024, with solar alone contributing around 11.4 percent.

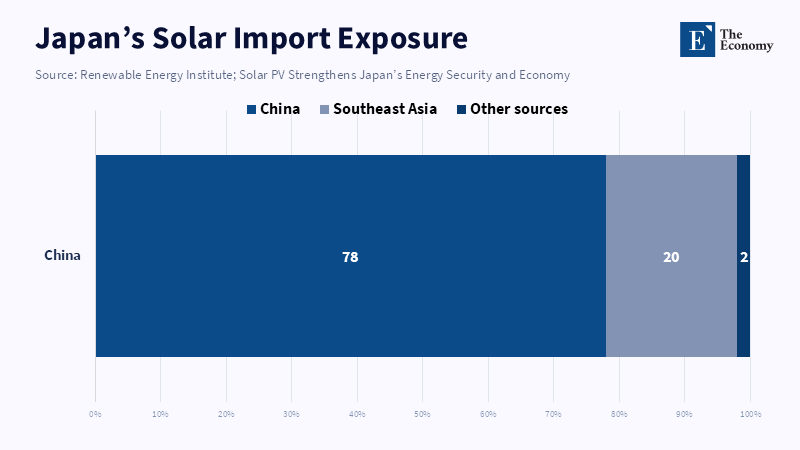

The problem, in China's dominance, is clear. China commands more than 80 percent of each major stage in manufacturing. China accounted for roughly 78% of the import value of modules to Japan in 2025 and Southeast Asia accounted for around 20%. The domestic market accounts for roughly 34% of module sales in Japan, by value, including overseas production (2024), but does not constitute domestic control and the upstream segments of polysilicon and ingot production were lost entirely and it is this that, at times of export restrictions, sanctions, trade disputes, or supply chain disruptions, is a strategic vulnerability. It doesn't have a fuel import component but has an import technology component. For Japan, whose entire post-war economic and social identity rests on its capabilities as a manufacturer, the idea of a clean energy system based on Chinese-manufactured high technology carries a political weight that is difficult to calculate in terms of cost per kWh.

For Japan, therefore, it's a sovereignty gambit. Imported solar panels provide energy independence after installation (you don't need to import fuels to generate electricity, a key advantage over coal or gas). The development phase does, however, rely on a supply chain that Japan doesn't own. The Japanese hydrogen strategy is an attempt to reverse the situation. If Japan can produce, deliver, store and consume the hydrogen, or ammonia, using systems built here in Japan, then it has an opportunity to export not just the energy, but the hardware, the ships, the turbines, the tanks, the compressors, the trading architecture, the safety standards, the fuel cell technology. It may not deliver for every home and every passenger car, but it has the potential for industrial sectors, shipping, aviation, the high-temperature sector and for seasonal storage.

The grid argument is stronger than critics admit

The second factor that underpins the Japanese hydrogen strategy is that the Japanese electricity grid is already complex and hard to redevelop quickly. The grid operates at two different frequencies in the east and the west of Japan, limiting large-scale power transfer between the two; it runs through steep mountains, slowing down the process of constructing power lines, placing wind turbines and solar arrays; the reopening of nuclear power is highly politically sensitive; and although offshore wind potential is huge, the technology is still not being developed quickly enough. 10GW offshore by 2030 and 30-45GW by 2040 seems a tall order given that only ~5.1GW were under development at the end of 2024. This is a major gap to bridge.

Hydrogen provides the promise of utilizing the existing grid more effectively. It could be delivered via ports, tanks, ships and into industrial zones, it can be co-fired in existing coal plants, it could be used in gas turbines and industrial boilers. It's not efficient and it's not always cheap, and in some cases, it's a way of propping up existing fossil fuel infrastructure, but it provides a political route away from requiring a radical overhaul of the electricity system, and a buy-in from all regions, utilities, and voters.

However, it is certainly the case, as argued by the critics, that this bridge may serve as a trap. Burning ammonia alongside coal will reduce direct emissions at the plant site but it does not make coal green. Imported hydrogen could generate considerable indirect emissions if, when being produced, liquefied, converted, transported and reconverted, it is not carefully managed. Blue hydrogen can be used as an instrument to continue the use of gas. Green hydrogen would be wasted if burnt when direct electrification is cheaper. The market for hydrogen at the international level is also underdeveloped, while low-emissions projects with commitments for investments could be three-to-five-fold by 2030, there are no firm offtake commitments for anything near the potential capacity expressed in project announcements. Demand is still weak.

This water-to-energy rhetoric must therefore be disciplined. Water surrounding Japan is abundant; Japan needs energy to make it into hydrogen. If Japan relies on carbon-intensive sources, then the climate case weakens. If renewable, Japan has to build tremendous renewable electricity capacity domestically or import hydrogen from regions that can supply it at a low cost from renewable electricity sources. This comparison to the Middle East's past rise due to oil has an impact because it brings out the idea of national resurrection. However, the Middle East rose to economic prominence on an oil source that was both dense, inexpensive to mine and easy to transport, Hydrogen is the opposite: diffuse, costly to transport and difficult to price

The gamble must become disciplined, not bigger

A proper policy for Japan should not compare "hydrogen and solar?" It sets up the policy problem in the wrong context. Japan needs solar electricity today; it should soon build offshore wind; it should use nuclear if safe and palatable; it needs storage where appropriate; it should use molecular energy where electron energy cannot be used; it needs to use hydrogen where this is appropriate. Japan's policy should not have a general hydrogen strategy but should focus on where it is needed: a tool to de-carbonize industrial sectors and to supply clean feedstocks, use it in shipping, aviation and power generation (backup), and in industrial clusters. Every yen of public funding provided to projects must show actual carbon reduction potential, manage import risks, identify potential for exports and confirm demand.

That could keep Japan from the biggest danger in its hydrogen strategy: sunk-cost nationalism, which can lead a nation to overinvest in something merely due to prior investments already made, a tendency that leads to uneconomical projects to persist far beyond their lifespan and strategic investments turning into policy traps. No fossil fuel-driven hydrogen projects with a weak direct carbon footprint should be allowed to persist beyond the near term; such projects, whether utilizing supply chains powered by fossils or weak Carbon Capture, will not justify large public investments. Where cheaper and cleaner alternatives based on direct electrical inputs are readily available, these must be the preferred choice, not patriotism; there should be no patriotic defense of bad investment.

Patriotism has a role, but only in motivating a nation to achieve what the world views as impossible; there are numerous cases where belated industrial investments such as South Korea's semiconductor market rise, have become dominant global industries. Japan is well placed to do the same in several areas along the value chain with its industrial base, such as Kawasaki's liquid hydrogen carriers, its expertise in fuel cells through Toyota, trials in steel manufacturing, its growing ammonia supply chain and its hydrogen market design frameworks. Whether those strengths will be properly concentrated or dispersed over too broad a front to make a tangible impact remains a critical question.

The ideal Japan hydrogen strategy would involve an ambitious industrial program that recognizes three vital facts: solar is the cheapest technology available and has to be deployed as rapidly as possible; China's dominance in clean technology is a strategic concern that must be countered without a nationalist techno-competition; while hydrogen is still too costly for many uses today, its potential value in the future sectors means it cannot be disregarded; a clever country can reconcile all three facts simultaneously.

Japan's 15.3 percent energy self-sufficiency cannot be ignored while crafting policy and is one of the reasons that Japan has looked into hydrogen technology at great cost from the outside. Low energy self-sufficiency cannot justify the risks and Gamble of the policy and can instead justify sound investments; Japan should not abandon hydrogen and only import solar power, nor use hydrogen as a mask for more affordable clean electricity alternatives and the policy direction must be far more concentrated. Japan must invest quickly in solar and storage; it must upgrade the grid where and when necessary; it should invest urgently in offshore wind and, only where deep security and deep decarbonization could be achieved, hydrogen; should these investments be concentrated in a coherent way, Japan's hydrogen strategy would be less a diversion and more an investment in a few sectors of the future within its control.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Agency for Natural Resources and Energy (2024) ‘Hydrogen Society Promotion Act Enacted. Toward a Forthcoming Hydrogen-based Society. Part 2: Utilization of Clean Hydrogen’. Tokyo: Ministry of Economy, Trade and Industry.

Agency for Natural Resources and Energy (2025) Energy White Paper 2025: Summary. Tokyo: Ministry of Economy, Trade and Industry.

Agency for Natural Resources and Energy (2025) ‘Japan’s Offshore Wind Power Generation Now and the Future’. Tokyo: Ministry of Economy, Trade and Industry.

Institute for Sustainable Energy Policies (2025) ‘2024 Share of Electricity from Renewable Energy Resources in Japan’. Tokyo: Institute for Sustainable Energy Policies.

International Energy Agency (2022) Solar PV Global Supply Chains. Paris: International Energy Agency.

International Energy Agency (2025) Global Hydrogen Review 2025. Paris: International Energy Agency.

International Energy Agency (2025) World Energy Investment 2025. Paris: International Energy Agency.

Masson, G., van Rechem, A., de l’Epine, M. and Jäger-Waldau, A. (2025) Snapshot of Global PV Markets 2025. Paris: IEA Photovoltaic Power Systems Programme.

Matsuno, T. (2025) ‘Japan’s Hydrogen Gamble: What the World Can Learn from This High-Stakes Energy Bet’. World Economic Forum, 29 April.

Ministry of Economy, Trade and Industry (2023) Overview of Basic Hydrogen Strategy. Tokyo: Ministry of Economy, Trade and Industry.

Temocin, P. (2026) ‘Japan’s Hydrogen Pivot Is a Detour from Real Decarbonisation’. East Asia Forum, 29 April.

Tochibayashi, N. and Kutty, N. (2024) ‘Hydrogen Is Developing Fast in Japan, Edging Nearer to Wider Use in Society’. World Economic Forum, 10 April.

Zissler, R. (2026) ‘Solar PV Strengthens Japan’s Energy Security and Economy’. Renewable Energy Institute, 2 February.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.