CEO Compensation Is a Market-Cycle Problem, Not Only a Pay-Ratio Problem

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

Judge CEO pay by market cycles, not outrage High pay can reflect real risk and value saved Boards must reward skill, not market luck

One number puts reason out of count on why the CEO pay debate keeps missing its best question. The median S&P 500 CEO made $17.1 million in 2024. The median worker on the same survey made $85,419. It would take 192 years for that median worker to buy a median CEO's paycheck. The number is stunning. It draws you to anger without bringing you to analysis. The better policy question is not whether CEO pay seems excessive. It is. The harder question is whether CEO pay fluctuates fairly with the market cycle, with outcomes and with the risk that the CEO faces. If pay puffs up in a bubble and pegs down in a slump, skill is unlikely.

CEO Compensation Must Be Judged Across Bull and Bear Markets

The classical debate over CEO pay is ratio talk culminating in a verdict. That is too thin a foundation. Pay ratios reveal the social dimension of the firm, but not whether the contract was appropriate. A better way to analyze pay practices is to examine their cyclicality. During a bull market, higher asset prices lift many firms in unison; during a bear market, they may drag most firms down, even if the CEO acts brilliantly. In designing a pay policy for the CEO, it would be wise to quantify what part of the pay was attributable to the tide. A second question is which portion may be attributable to firm-specific efforts and the third question is how big a role is played by the board's exercise to retain a capable leader who can absorb the stress. The reframed question is more relevant today, because the bulk of CEO pay is more and more equity-based; stock awards are not an incidental thank-you, they are the principal component of Pay. With rising markets, pay can trend up; with falling markets, wealth can trend down.

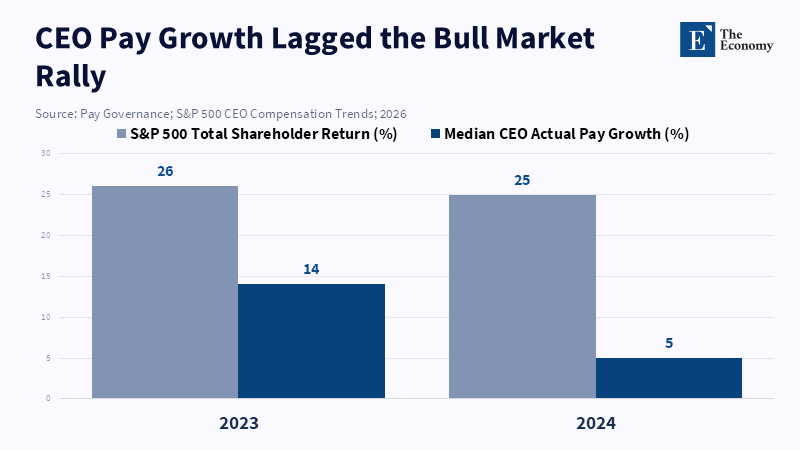

This trend is also apparent in recent years. Following a flat 2022, median S&P 500 CEO pay increased modestly by 0.9% to $14.8 million and median bonus declined by 15.5%. In 2023, by the time the equity markets recovered, median pay increased by 12.6% to $16.3 million, while in 2024, with the S&P 500 over 23% higher and index profits more than 9% higher, median CEO pay increased another 9.7% to $17.1 million. This does not provide any evidence that pay is fair, but it does provide evidence that pay is not fixed like a royal stipend, but has become saw-toothed, equity-intensive and linked to market sentiment. This is the policy challenge. Simply increasing it is the wrong solution.

The test works both ways. If, after all, CEO pay goes up less than total shareholder return during a bull market, the contract could be more limited than much of the debate would have us believe. An S&P 500 review last year actually found that median actual CEO pay rose by a modest 5 percent in 2024, while total shareholder return rose by nearly 25 percent. They also found that, since 2010, CEO pay has risen at an estimated 5 percent compound rate while total shareholder return has risen at nearly 14 percent a year. Such numbers bolster a limited argument for mega bonuses. They suggest that, in many big firms, CEO pay has not kept pace with the overall rise in the market. But even that is not the whole story. A deal can be linked to the right measure in the right direction and yet still be rewarding luck, obscuring below-par performance, or shielding a weak CEO.

CEO Compensation Is Not One Number

But CEO pay is spoken of as so much cash that cash is no longer the story. Salary is the stable element. Stock and long-term incentives are the heaviest lifts. In 2024, stock awards accounted for over 70 percent of the median S&P 500 CEO pay package. And that matters because stock awards can be booked at grant value far before the executive can turn around and sell. Some awards vest only if the market value, operating income, or another target is attained. Others fall in value if the share price drops. The same headline pay number can mean very different things. One can be a near-guaranteed transfer. The other is an uncertain claim on future firm value. Failure to distinguish them leads to bad policies and bad public commentary.

The risk side is also real, even if it should not be overglorified. The CEO is the face of the public relations disaster of layoffs, price increases, failed transactions, product catastrophes, cyber events, safety scandals and activist press campaigns. The latest personnel changes reveal how exposed the role has become. On each measure tracked by the firm, the global number of CEO departures in 2024 reached an all-time high and the level increased again across all large-cap indexes in 2025. Just in the S&P 500, 59 chief executives left that year. Security totals have also entered the compensation landscape following the murder of UnitedHealthcare boss Brian Thompson, as median security expenses for a sample of S&P 500 companies increased from $69,180 in 2023 to $94,276 in 2024. Yet this is not to provide a remuneration explanation. It is to reveal that the role encompasses public, legal and personal risk not accounted for by comparison with other wages.

That argument requires sensitive handling. Risk (or stress) is not a price for any work. Nurses, warehouse workers and couriers all work under duress and generally for a lot less cash. The more important claim is specialized. The market price for CEO compensation, greedy or not, is the market price for a scarce commodity; judgment under pressure of the kind that shareholders require. The market value that their decisions affect goes into the equation, as does the credibility of their commitment and the embarrassment factor that they can offer in its absence. That explains why the better question is not whether a CEO works 200 times harder than an average employee; no one ever does. The real test is whether the CEO’s marginal influence, stress exposure and replacement cost are priced appropriately for shareholders and defensibly for staff.

Downturn Pay Tests Whether Boards Reward Skill or Luck

The strongest attack on CEO pay is not the level, but that CEOs may be rewarded for widespread market performance while being insulated from widespread market downturns, the pay-for-luck problem. This becomes apparent if a disruption alters reported results or valuations in ways that a CEO did not orchestrate. Tax windfalls, changes in interest rates, stock swings, pandemic demand, or currency fluctuations can all inflate or deflate results. If a CEO wins extra pay for a market, generates a gain while suffering no corresponding penalty for a market, generates a loss, then the contract is asymmetrical and the free rider case is strongest.

Tax windfalls are harbingers. In one research study of the 2017 U.S. corporate tax reduction, it was observed that firms with substantial one-off tax windfalls paid their weakly monitored CEOs around 8.3 percent more than the other firms with a small windfall. The extra paid in median CEO note is about a $330,000 annual salary. The authors identified no comparable penalty in the case of tax losses and no evidence that the additional pay predicted higher subsequent profits. This finding is important for measures to counteract market cycles. It indicates that some boards mistake a lucky break for CEO skill and that the additional scrutiny matters. When boards, analysts, investors and newspapers showed closer attention to the pay, the pay-for-luck correlation moderated. Effective oversight can disentangle passively earned windfalls from earned resilience.

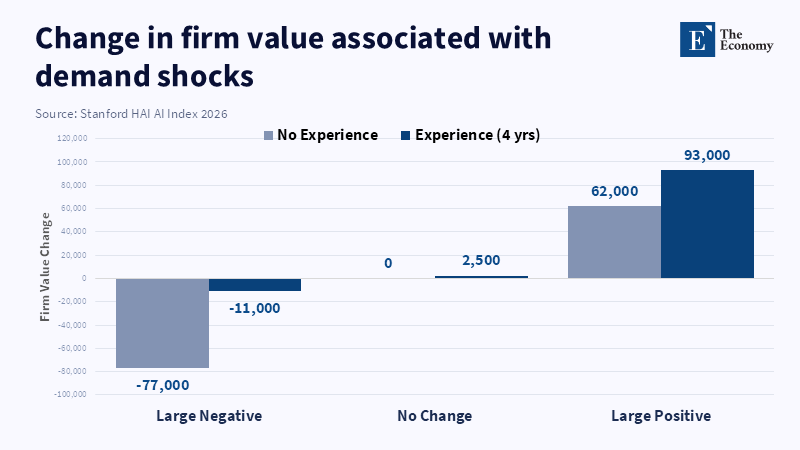

But the opposite may also be true. A pay-for-performance CEO who preserves a company through a shock deserves to be paid handsomely if the share price falls. A retailer that sheds only half the 40 percent contraction suffered by the rest of the sector has not failed; it has hedged. A manufacturer that preserves suppliers, liquidity and human capital through a demand shock creates value that does not appear immediately. (That is the space often lost in normative debate.) In downturns, CEO pay should not be assessed solely on absolute return. It should be evaluated relative to a clean counterfactual: similar firms, preset strategy, capital mix, current liquidity, customer loyalty and the firm's exposure to the shock. If the leader has minimized damage that would have been worse, then a large payout is reasonable.

It also addresses the oft-heard street-level logic. Why pay so much when I could get someone cheaper to do that job?' For a small shop, that certainly may be true. For a large publicly traded entity, it depends on how much it costs to make the wrong hire. A bad CEO can wipe out more value in a single quarter than an entire year's worth of pay at market levels. The Search pool is small, publicly available and benchmarked. Boards are not simply buying labor. They are buying a probability distribution of results. That does not equate to the market not pricing the market, determined role well. It does mean a low-salary alternative is not necessarily cheaper, including the chance of failure. The optimal reform is not a cap; it is a better way to demonstrate that enormous pay correlates with firm-specific value.

Better CEO Compensation Rules Should Price Risk, Not Defend Excess

Policy must therefore shift its focus from anger to design. While pressure on boards should continue if CEO pay vastly outpaces that of workers, the social signal is counterproductive and worker morale is crucial.1 Yet a more meaningful reform isn't to dial down total CEO pay; it's to demand more explicit evidence of its justification. A pay plan should indicate the share of a CEO's upside attributable to general market, sector, or firm performance. It should clarify how a target date and magnitude are set in absolute and relative terms. It should address what will happen in a bear market before the bear market hits. It should use extended holding periods, clawbacks and post-exit stock ownership so the CEO can't take profits while the risks are obscure. It's a standard that a public report can comply with and that substantial boards can rely on. It does not ban pay; it urges the firm to demonstrate need, to justify the premium now and to win worker and investor confidence.

That'd make it easier for boards, investors and policymakers to interpret CEO pay with a little less heat and a little more discipline. Even in a recession, boards could still hand out a payday, just not too one-sided a payday. They'd need to make a good business case: did we have sector leadership? Did we protect cash flow? Did we survive the bear? Did we avoid a solvency shock? Did the CEO lose money while our other shareholders did? Such questions are more illuminating than working out if it looks outrageously high. They also shield genuine CEOs from being labeled free riders when they have, in fact, been riding us through a tough patch. They also reveal deals that subsidize the bull and pardon the bear.

The opening ratio still counts. A 192-to-1 difference is not noise. It is a stress test for trust within capitalism. But that ratio ought to start a debate, not end one. Executive pay can only be justified if it is unequivocally linked to risk, cycle-adjusted returns and value that the company could not have created without that individual. During bull markets, boards need to stop crediting all rising share prices to leadership. During bear markets, opponents need to stop accusing all high payouts of theft. The bar should be higher for everyone. Reward the chief executive officer only when he or she makes a difference in the outcome. Deny him or her the reward when the market was responsible. That strategy, the simplest, departs clearest from the premise that high pay is a mark of privilege.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Andreani, M., Ellahie, A. and Shivakumar, L. (2025) ‘Are CEOs Rewarded for Luck? Evidence from Corporate Tax Windfalls’, The Journal of Finance, 80(4), pp. 2255–2302. DOI: 10.1111/jofi.13448.

Anderson, M. and Harloff, P. (2025) ‘CEO Pay Rose Nearly 10% in 2024 as Stock Prices and Profits Soared’, Associated Press, 1 June.

Batish, A. (2025) ‘2025 Equilar | Associated Press CEO Pay Study’, Equilar, 29 May.

Binnie, I. (2025) ‘Global CEO Departures Hit Record High in 2024 amid Investor Pressure’, Reuters, 29 January.

Bout, A., Cuevas, P. and Lawani, J. (2026) ‘S&P 500 CEO Compensation Trends’, Harvard Law School Forum on Corporate Governance, 4 February.

Donatiello, N.E., Larcker, D.F. and Tayan, B. (2016) ‘CEO Pay, Performance, and Value Sharing’, Stanford Closer Look Series, Corporate Governance Research Initiative, Stanford Graduate School of Business, 3 March.

Hummels, D., Munch, J.R. and Zhang, H. (2026) ‘Using Global Shocks as a Laboratory to Study Executive Pay’, VoxEU/CEPR, 26 April.

Russell Reynolds Associates (2026) ‘Shorter Runways, Higher Stakes: What Today’s CEO Turnover Means for Boards and Succession’, Global CEO Turnover Index.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.