The Energy Shock Has Turned Renewable Energy Competition Into Asia’s Real Security Policy

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

The Iran war has made fossil fuel dependence a direct economic risk for Asia Renewable energy competition is now central to growth, inflation control and energy security China will gain, but India can compete too

The world added 585 GW of renewable power capacity in 2024; the majority, over 90%, of new power capacity is renewable. This was before the latest oil and gas shock turned the Strait of Hormuz into a balance-sheet liability for Asian economies rather than a trade route. Why this figure matters is that it indicates that the energy transition is not a matter of future potential, but the cheapest insurance policy that many economies have available. The shock has become even clearer since the latest Iran-related energy shock intensified. The premium on imported fuel is now reflected in higher inflation, weaker growth, fiscal distress and lower household demand. In reality, the problem facing Asia is no longer whether or not to move away from fossils fuels, but who will dominate the newly emerged clean technology race and how states would be able to transform increased demand into lasting industrial capacity in response to the shock.

Economic Security through Competition in Renewables

In the past, the old economic security model was based on the secure provision of supply: States were determined to win oil cargo and gas contracts; they secured shipping lines and tank facilities and stable relations with fuel producers. While all these still apply in some way today, the model can no longer explain why certain fuel-importing economies still find themselves in trouble even if they have all the contracts and stocks in hand, when faced with strategically important choke-points and premiums during wartime, tanker delays and sudden depreciation of their currency. It asks what portion of the final energy demand could be converted from molecules to electrons. Solar panels, wind turbines, batteries, grids, heating pumps and electric vehicles can no longer be seen solely as ways to combat global warming but as instruments to escape foreign exchange losses, price volatility and foreign political pressure. That is the reason why renewable energy competition has become an instrument of national security, just as it has become an instrument of industrial policy.

The data presented on the latest crisis is strong enough to shift the focus completely. Growth in developing Asia was revised downwards from 5.1% in 2026 to 4.7%, on the back of the current shocks from the Middle East, with a worst case of 4.2% if fuel prices don't fall. That's a region-wide loss of growth between 0.4-0.9% within the first crisis; it directly corresponds to the social cost faced by many fuel-importing economies. The shock is not only faced by households at the gas pump, but it also impacts power costs, the prices of foodstuffs and farming inputs, the costs of transportation, the cost of borrowing funds and a widening variety of other prices. While the governments have tried to reduce costs to households through subsidies in an effort to avoid unrest and higher inflation rates, this comes with the cost of a growing burden of public debt. Public finance for many economies is not capable of maintaining peace and affordability in times of crisis, given the two years of the COVID pandemic and conflict, the escalating cost of debt servicing and the cheap fuel to compensate.

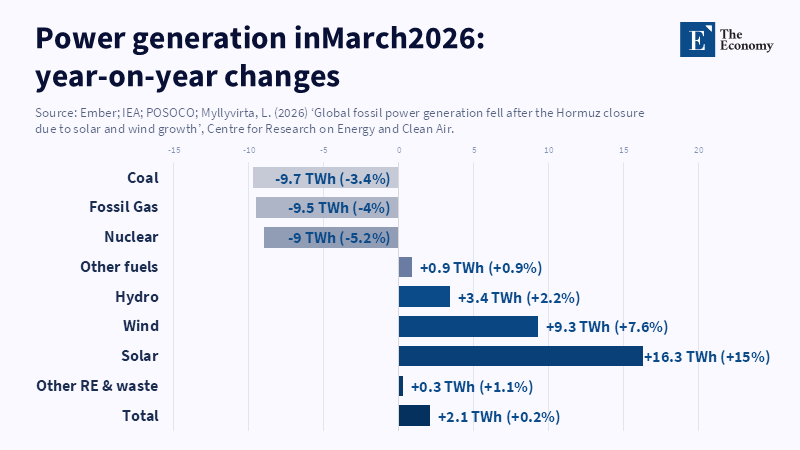

This explains the debate of whether coal might be making a comeback; a crisis is seen as providing a compelling rationale for the usage of a familiar fuel source, which can justify reliance upon an existing system. Nevertheless, there is little evidence of a global resurgence of coal in the first month after the shutdown of Hormuz; in the first month after its closure, countries that are providing reliable data showed that fossil-fueled power generation dropped by 1% year-on-year and by 3% for gas-fired power generation, while solar generation increased by 7% and wind generation by 12%. In all states apart from China, fossil-fueled power generation, both from coal- and gas-fired power plants, dropped while the generation from renewables increased strongly. While China may have increased its coal-fueled generation in some coastal areas, the takeaway is that fossil fuels are not indestructible; states with existing built-up capacity from renewables are clearly better off.

Renewable Energy Competition Is Not Just China vs. the United States

Despite all the shocks, China is currently leading the early renewable energy competition. The advantages are its economies of scale, affordable price point, developed supply chains, strong network of suppliers, government incentives and its significant export market. It's still a dominant manufacturer of solar panels, much more than in terms of global solar demand. China has also taken a large lead in producing and selling electric cars, with sales exceeding 11 million in 2024, half of them being new car sales. And again, it's the main supplier in developing markets. In light of the fuel crisis, Asia and its countries are turning more and more to electric vehicles, including the emerging markets of electric bikes, three-wheelers, buses and delivery vehicles, rather than high-priced luxury cars.

Though a substantial competitive advantage does not assure a long-term dominance. As demand for renewable energy sources is surging, integrated supply chains for manufacturing solar panels, wind turbines, batteries, deployment and after-sales support are critical. The global demand for renewable energy means that numerous nations will attempt to build localized manufacturing capacities rather than depending on a pure import-dependent model and that a comprehensive renewable energy supply chain, not only assembly parts, will dominate the next stage. China might remain the number one exporter of clean technologies for the foreseeable future, but the crisis will also stimulate countries like India, the US, Europe, Japan, Korea and ASEAN to seize market opportunities and utilize clean technology manufacturing and development as part of economic policies.

The success of the clean energy industry cannot be summed up as merely a race between the US and China and this is what India proves as an example. Its planned increase in solar generation capacity by the mid-2030s, accompanied by the country's goals on wind power and storage capacity is just an indication; India has been trying to scale up solar panel manufacturing through policies on building fully integrated supply chains not just assembly lines, it still imports a substantial amount of upstream components, however it is switching from being a pure importer of clean technologies and services to an exporter, standard setter and counterforce to China in the competition sphere.

What does it mean for Asia? Replacing a dependency on single oil suppliers with dependence on a single clean technology exporter carries the risk of the problem moving from one location to another. To limit these potential risks, states should encourage rather than restrict imports of clean technology and leverage the competitive advantages China offers while developing their own local capacities where strategically important. Although integrated supply chains are the best outcome possible, focusing policy support on individual clean technologies, whether it's solar panels, wind turbines, batteries, power grids, or charging equipment, individually can bring reasonable success even if not all segments become fully localized manufacturing and states can define for themselves what the most strategic elements to produce are. Broad-brush policy recommendations to all actors on the field might simply prove inefficient and costly.

The Missing Links in Renewable Energy Competition

The main danger is that governments misread the transition, believing that by acquiring renewable technologies, the energy transition has already been done. You can install a solar panel or a wind turbine without an adequate power system or energy security. To fully harness renewable energy, particularly with the increased grid load from transportation and heating electrification, states will require reliable power grids, sufficient storage, effective demand response programs, adequate feed-in-tariffs, effective interconnections between the place where electricity is generated and end-users, reasonable permitting and comprehensive distribution reform. The success of competition in the renewable energy domain in the future will be less dependent on visible equipment, but on critical invisible infrastructure.

Here lies a difficulty, or not too glamorous side, which reveals weakness in most Asian energy systems. A lot of Asian markets still use highly distorted tariffs, suffer from inefficient distribution companies and cumbersome approvals of land clearance. Utilities still sell electricity at negative prices and thus, there are incentives not to bring forward renewable energy. Several utilities still subsidize fossil fuels so much that the cost advantage of cleaner alternatives is hardly visible. Policy outcome: governments used to shield consumers from global prices through subsidies, then those subsidies strain the national economy and slow down infrastructure investments necessary to obviate the need for subsidies.

The state-level problems of India are insightful. The security of the energy sector cannot be built at the national ministry level only, but is driven by state-level regulators, distributors, land registries, your local bus stations, building codes and the public sector organizations’ purchasing patterns. A national goal of 500 GW cannot bring much change if your local distributor cannot or delays, underpays, or discourages you from installing rooftop solar. The same applies to Southeast Asia; inviting investment for renewable energy will lead to the slowing down of capital due to delays in grid connection, unclear tariffs and long waiting lines. Countries that enact swift and thorough reforms will actually profit in the cleanest terms, not based on rhetoric.

EVs show the same pattern. Asia will get more benefits in small vehicles, buses and fleet rather than copying the luxury EV market for developed countries. Besides savings of fuel costs, reduction of air pollution, reducing dependence on imported oil and diesel, EV charging will use clean electricity but needs effective infrastructure for charging, which should be based on a certain standard, especially battery swap and public charging network. It needs support from governments to provide incentives to develop public transport and help apartment and fleet owners install charging facilities. Otherwise, the agenda will remain in concept and in the showroom rather than as policy for security.

The new test is inflation, austerity and industrial choice

Another barrier now appears: the present context of inflation and its effects on debates on industrial policy and austerity. A simple argument against accelerating the switch to renewables is that consumers already suffer from rising prices in everything (food, housing, fuels, cost of credit, etc) and governments should not impose more costs on the public to pursue a greener world. This is true; poor climate policies can be regressive (reduction of subsidies would hurt low-income groups and the cost of purchasing equipment would lead to public riots). However, this doesn't mean that competition in the renewable energy market can never happen; it just means that it has to be structured in a way to protect households’ cost of living, generate jobs and secure energy, instead of sloganeering. Fossil-fuel dependence would also regress as poor people allocate a large portion of their income to fuels for transportation and cooking. They are also the first victims of budget cuts to finance universal fuel subsidies.

Targeted subsidies and quick replacement solutions: low-income groups will get direct relief and support, but fossil fuels shouldn't be an automatic benefit. Instead, the governments should incentivize electric buses, two-wheelers, public buildings with rooftop solar, intelligent cooling devices, storage for weak grids and locally made goods when and where they are competitive. Industrial policies also must make sense, don't make impossible claims that all nations would manufacture all necessary components and only invest in domestic products if they fulfill price, quantity and quality standards. While China and India might strengthen their positions as manufacturers of solar panels and batteries, Vietnam and Thailand are in a good position to produce EVs and the like. The governments in Korea and Japan are already taking the lead in advanced manufacturing, such as complex components and technologies, grids and high-end vehicles. Developing nations, small as they might be, could profit the most from wide distribution, service sectors and regional power trade instead of subsidies.

Discussions on austerity and the energy transition can no longer be segregated. By spending trillions on artificial manipulation of fossil fuel prices, governments forgo opportunities to invest in grid infrastructure, battery storage, public transportation, or industrial upgrading. The high inflation rates and interest rate hikes implemented by central banks are already dampening private investments. The finance ministry’s already tight budget is always strained by the cost of fuel subsidies, which inevitably entails cuts in healthcare, education, or general infrastructure. Those costs are the true social costs of fossil fuels and have always been hidden in the global assessment of their costs, till the war in Iran revealed the real cost of fuels when we add up the insurance premiums needed to keep supplies constant.

The opening statistic is essential since it points out the trajectory. The fact that the world has generated 585GW of renewable energy in a year means the world has already begun the phase-out of the oil market. The war in Iran only reminded us of how much time it had lost so far. For Asia, the challenge now is how to change necessity-driven demand to sustainable long-term capacity, not through blanket subsidies but direct relief for low-income consumers, accelerating grid development, clean transportation, strategic industrial policies, encouraging cross-border investments and diversifying sources. China would tremendously benefit, just like other Asian states, including India. Losers will be states that still adhere to the old, outdated regime of security derived from fossil fuels and states will succeed in this field based on performance.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Asian Development Bank (2026) Asian Development Outlook April 2026: The Middle East Conflict Challenges Resilience in Asia and the Pacific. Manila: Asian Development Bank.

Downs, E. (2026) ‘Hormuz closure opens doors for China’s energy leadership’, East Asia Forum, 3 May.

EAF editors (2026) ‘The energy pinch is an economic omnicrisis for Asia’, East Asia Forum, 4 May.

Garg, V., Sharma, P., Tewani, C.H., Gupta, A. and Tiwari, S. (2025) Assessing the Effectiveness of India’s Solar Production Linked Incentive Scheme. Institute for Energy Economics and Financial Analysis and JMK Research & Analytics.

International Energy Agency (2022) Special Report on Solar PV Global Supply Chains. Paris: International Energy Agency.

International Energy Agency (2024) Renewables 2024: Analysis and Forecast to 2030. Paris: International Energy Agency.

International Energy Agency (2025) Global EV Outlook 2025. Paris: International Energy Agency.

International Renewable Energy Agency (2025) Renewable Capacity Statistics 2025. Abu Dhabi: International Renewable Energy Agency.

Kennedy, C. (2026) ‘India Unveils Ambitious Plan to Quadruple Solar Power by 2035’, Oilprice.com, 19 March.

Myllyvirta, L. (2026) ‘Global fossil power generation fell after the Hormuz closure due to solar and wind growth’, Centre for Research on Energy and Clean Air, 15 April.

Reuters (2026) ‘Asian Development Bank cuts regional growth forecasts on impact of war in Middle East’, Reuters, 29 April.

Roy, A. (2026) ‘Beyond Hormuz: Why India’s Energy Security Must Be Built by Its States’, Observer Research Foundation, 30 April.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.