R&D Tax Credits Are Not Innovation Cash

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

R&D tax credits and direct subsidies are not the same tool Tax credits help profitable firms; subsidies help projects start Innovation policy must match support to cash needs, not labels

In 2024, China passed the milestone of 3.613 trillion yuan in national R&D spending, equivalent to 2.68 percent of GDP. That is a fine national boast to have, but it should be a warning. Governments now buy innovation through the back door, too. A budget can be huge, a tax code can be generous, but the outcome can be starkly inconsistent if the tool ends up reaching the wrong firm at the wrong moment. The most common form of support, R&D tax credits, is held out as a clean, neutral form of support, when in fact they are not; they are a firm-level discount that works best when a firm is already spending on R&D, has a clean set of books and enough tax capacity to use up the relief. A direct subsidy is very different; it is project-related cash that hits the firm before the payoff is known. That distinction alone determines whether policy helps only those firms already inside the innovation system, or also those trying to get inside.

Why R&D tax credits and subsidies are not interchangeable

The most common flaw is to imagine that R&D tax credits and direct subsidies are merely different pathways to the same end. Both are aimed at reducing the private cost of innovation, but they do so through two different gates. R&D tax credits are usually de facto rule-based: a firm chooses to spend, deducts the cost and applies through the tax system for relief, while direct subsidies are more often de facto project-based: a firm applies, the government approves and the payment is made against a specific project. One drops the effective price of R&D borne by the firm; the other places cash on the table for a specific project. The one affects the firm's average R&D expenditure, the other makes a choice of an innovation project. This is not trivial. It is the difference between who applies, who benefits and what kind of innovation gets done.

Suppose that a tax credit and a subsidy had the same effect over a narrowly defined case: that a firm has a single product line of one consistent kind, a long-term stable R&D plan, huge profits, enough tax capacity to claim and no cash-binding constraints. The tax credit could then be a deferred grant and if the taxpayer is not cash-constrained, the impact on behavior would be almost identical between the two. But most real firms do not look like that. Large multi-product conglomerates move money across product lines. Young or strained firms burn cash early and before revenues can be forecast. Smaller manufacturers may have useful process innovations but not enough taxable income to claim against, or huge cash constraints. A tax incentive mainly affects what is already open in the books and a subsidy can open up what otherwise would not be. This is not just a matter of logistics. It has implications for policy choices: whether to promote breadth or to steer entry.

It is only in the narrowest of cases that the two tools would have an equal effect: when a single profitable locus can be assumed; a project can have an assured payoff flow and revenues can be foreseen one year ahead; when one can write a credible R&D roadmap without the deep improvisation the modern business needs. Even then, the same logic applies: an incentive to make an already-unstable activity cheaper, another to make a new activity easier. The first affects the remaining price of R&D, the second affects whether risk is ever taken at all. That, once again, is the deciding factor between policy that merely accelerates current activity and policy that forges new paths on innovation.

R&D tax credits exclude firms with no tax base

The key fissure is not between small and large firms. It is between firms with usable tax capacity and firms without. A small firm with solid profits and careful accounts may benefit from an R&D tax credit, while a young or cash-strapped company may view it as a future promise and a collateral-free one at that. This is why lean start-ups with little cash, a good idea and no tax base often prefer direct support. The problem is not that they do not like tax benefits: it is that the tax tool cannot help if the cash does not come in. The relief must be refundable, quick and easy to claim. If it is not, then the policy is set up to appear generous on paper but to generate weak effects in practice.

There is strong evidence that this taxonomy applies: that firms with a tax capacity are more eager to take advantage of R&D incentives, while those smaller, newer, or cash-squeezed are better off with direct grants. Firms experienced in R&D are more likely to claim tax incentives; subsidies work better when seeking to induce the very first experiments. Firms that already have R&D labs and scientists know what to document, how to portray it and how to claim. It is young or new entrants that face the fixed costs of trying something new, finding the right equipment, personnel and laboratory space and figuring out who to bill and how to account for it. An incentive applied at the end of the process cannot provide the initial injection of cash needed to get the first project off the ground.

This does not mean R&D tax incentives are bad policy. It means policymakers often oversell them as a universal help to R&D; that they are better off promoting it where they want to widen a broad base of firms, rather than steering project choice; that they can, used at scale, cut the political costs of selecting winners; and that they can, when the spillovers are right, generate positive flow-on effects to neighboring firms and supply chains. But they are never neutral; a tax system carries its own bias; it favors firms that have lawyers, taxable income and have the patience to wait. Ignoring this leaves support systems that seem outward-facing but act like an exclusive club.

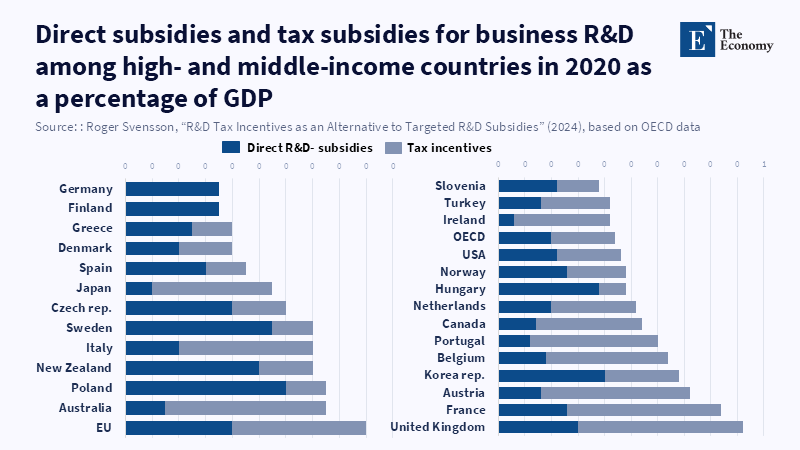

This shortcoming becomes apparent in current OECD analyses: OECD estimates show that close to 55 percent of total support for business R&D in the OECD area is now provided through tax incentives and the average SME R&D tax subsidy rate was higher than for large firms in that same year, yet the medium-sized and small firms received both higher and lower subsidies in different countries. Governments are unwilling to abandon the tax side of the equation: they want it for its large scale and political simplicity. Yet profits still matter and some firms will still have no tax infrastructure at all.

China exemplifies the promise and the pitfalls of scale

If there is one nation that shows how scale can distort the question, then it is China. Total R&D in the most recent year represented well over 3.612 trillion yuan, while basic research hit a new record of 249.7 billion yuan. But the emphasis in support has shifted heavily in the direction of a tax-driven system. OECD estimates suggest that tax incentives accounted for about 85 percent of China’s total public support for business R&D, showing how far the country’s support model has shifted toward the tax system. That is a hefty example of the power of scale, but also the risk of neglecting those firms that are not profitable, who burn cash when creating new processes, importing new machinery and fitting out laboratories for the first time.

This is proven at an industry level: Chinese manufacturing-based studies from 2009 to 2015 reveal that R&D became more efficient over the timeframe, rising to above-average levels in the electronics, machinery and chemical sectors studied; that tax-driven incentives maintained a strong, stable link to R&D efficiency; that direct payments became less relevant that same period, lagging behind the tax effects; and, lest we think that public money replaces private expenditure, at least one study raises concern that some firms may be spending exactly that much (hence crowding out). When these things happen, subsidies need rules; they require co-finance; they demand milestones.

Once again: what good is scale? In small amounts, tax incentives can make the difference for firms that are already cruising along, already organized for R&D and already hiring chemists; they can turn R&D projects into positive numbers on the income statement; they also have the potential to induce the firms that will create the next yield of patents, exports and new export markets; they do not, however, tend to promote firms without profits or without tax capacity into R&D. The problem begins when mass pushes the tax instrument too far and the less-appreciated firms with no profits, no history, no taxing experience and no benefit from scale get left behind. Without a bridge, the gap between current innovators and 21st-century rivals grows ever wider.

This is a place where utopians see efficiency; a subsidy appears uneven, because it takes time to apply, to choose and to settle; a tax credit appears to be given on demand, for free. Both are wrong. Efficiency should be judged against the problem it is meant to fix. If the problem is cost within a profitable employer, then an R&D tax incentive can be mighty; if the problem is, instead, cash, uncertainty, or entry, then a subsidy may be cheaper in the end. Innovation policies should be built around fit, not necessarily related to ideological preference.

Encourage innovation support built on liquidity, not labels

A more rational set of outcomes would instead begin with the liquidity of the firm: keep cash-flow-constrained, pre-profit startups outside the tax-only zone; provide direct support, vouchers, advance credits, or cash grants for rapid repayment; base the support on the same actual costs and allocations within the books, but aim to deliver the cash when the activity is computed into a cost; embed that in everyday support for established firms with the capacity to claim a tax credit, otherwise incentivize large firms with more power over their needs to claim in a manner commensurate with their low marginal cost, large number of lines of business and tendency to schedule projects over internal time horizons; sustain long-term projects with heavy spillovers in the grant of their choice, while addressing the pressures for over-spending that can arise when a project is not co-funded with private parties, staged in installments and subject to clawbacks if the costs end up mounting further.

Doing this can also help practitioners hit two targets they often set aside: first, by acknowledging the financial dimension of the battle to claim R&D support; and second, by recognizing that not every policy tool is the same. Any incentive that appears in the form of a tax discount is not without cost; it simply appears to be free of charge and is therefore easier than a grant to spread on a broad foundation. Any subsidy that appears simply to be an industrial planning instrument can be suspect at first sight; but if not, then the flexible correction for market failure remains necessary, because sometimes the industry needs help that the tax code cannot supply. The solution is not to abandon one or the other. It is to ensure every tool is put to its best use and that every claim is earned.

Innovation agencies, business incubators and policy advisers should start here. Innovation needs to be cast as timing: the credit is not cash, the grant is not waste; the tax credit is not the same as an R&D project. And for policymakers, the simple principle is this: which tool reaches the remaining firm before the idea is dead?

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Appelt, S., Bajgar, M., Criscuolo, C. and Galindo-Rueda, F. (2023) The impact of R&D tax incentives: Results from the OECD microBeRD+ project. OECD Science, Technology and Industry Policy Papers, No. 159. Paris: OECD Publishing.

Bloom, N., Van Reenen, J. and Williams, H. (2019) ‘A toolkit of policies to promote innovation’, Journal of Economic Perspectives, 33(3), pp. 163–184.

Busom, I., Corchuelo, B. and Martínez-Ros, E. (2012) ‘Tax incentives and direct support for R&D: What do firms use and why?’, Working Papers, wpdea1212. Barcelona: Department of Applied Economics, Universitat Autònoma de Barcelona.

Dechezleprêtre, A., Einiö, E., Martin, R., Nguyen, K.-T. and Van Reenen, J. (2023) ‘Do tax incentives increase firm innovation? An RD design for R&D, patents, and spillovers’, American Economic Journal: Economic Policy, 15(4), pp. 486–521.

Liu, Z. and Zhou, X. (2023) ‘Can direct subsidies or tax incentives improve the R&D efficiency of the manufacturing industry in China?’, Processes, 11(1), 181.

National Bureau of Statistics of China (2025) ‘China’s expenditure on research and experimental development (R&D) exceeded 3.6 trillion yuan in 2024’, National Bureau of Statistics of China, 7 February.

OECD (2023) OECD R&D tax incentives database, 2022 edition. Paris: OECD Publishing.

OECD (2025) ‘R&D tax incentives continue to outpace other forms of government support for R&D in most countries’, OECD Statistical Release, 22 April.

Svensson, R. (2024) ‘R&D tax incentives as an alternative to targeted R&D subsidies’, in Henrekson, M., Sandström, C. and Stenkula, M. (eds.) Moonshots and the New Industrial Policy. Cham: Springer, pp. 289–307.

Takalo, T., Tanayama, T. and Toivanen, O. (2024) ‘Welfare effects of R&D support policies’, Helsinki GSE Discussion Papers, No. 21. Helsinki: Helsinki Graduate School of Economics.

Toivanen, O. and Takalo, T. (2026) ‘The use and misuse of R&D subsidies and tax credits’, VoxEU / CEPR, 5 May.

Xie, Z., Xie, L. and Li, J. (2021) ‘Direct subsidies or tax credits? The effects of different R&D policy tools’, International Journal of Technology Management, 86(1), pp. 25–43.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.