The Buffer That Moves: Why Cross-Border Capital Buffers Need a Global Rulebook

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

Cross-border capital buffers can make one country safer while shifting risk to another Multinational banks expose the limits of national financial regulation Global coordination is now the hardest test for macroprudential policy

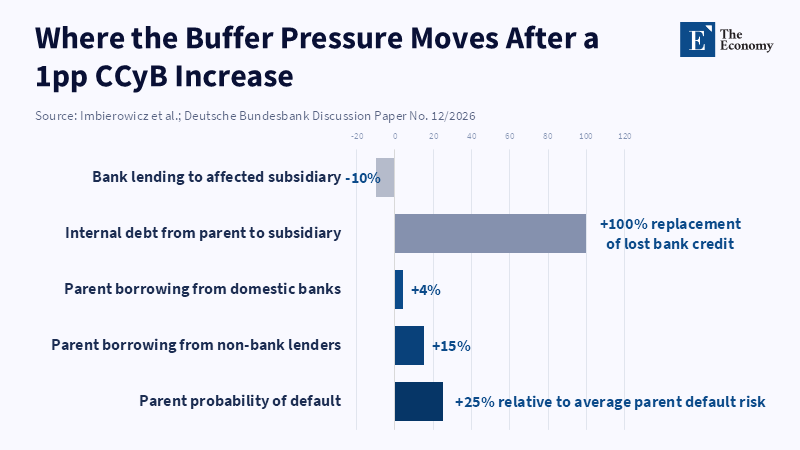

A 1-percentage-point increase in the countercyclical capital buffer of a host country can reduce bank lending to a banking subsidiary in an affected foreign country by about 10 percent. That sounds like success. It shows the buffer bites. It shows banks lend less in a booming market. It shows supervisors have internalized the lessons of 2008. Yet the same evidence also presents a harder truth. The affected subsidiary can often substitute the missing bank loan with more debt issued by its parent company. The parent can raise its borrowing in its own home market. The risk is not destroyed. It is merely displaced. This is the fundamental problem with cross-border capital buffers. They make each national balance sheet appear safer, while the multinational group provider successfully shifts the existing pressure elsewhere. After a crisis caused by global banks and paid for by local taxpayers, that is neither a minor flaw nor a new challenge for macroprudential policy.

The debate about buffers should focus not only on how much capital banks hold, but also on where the pressure moves when one country raises its guard. The classic question is whether banks are sufficiently capitalized in each country; the sharper question is, where does the pressure go when one country prudently raises its guard? Since the global financial crisis, regulators have substantially upgraded their buffers. This was necessary. Banks are safer post-2008 than they were, say, ten years ago. Yet cross-border capital buffers take place inside a global environment where multinational banks and multinational firms can, much faster than the speed at which local capital rules can follow, re-route their funding across borders. A cushion in a given market provides a safeguard to that market, but it might equally push risk into the parent bank, back into the home country, or into the next proxy legal gap. This is no deregulation by stealth. It is a safety displacement.

Why cross-border capital buffers changed the policy question

The countercyclical capital buffer was implemented for a straightforward reason. During times of relative prosperity, credit provision exceeds its natural speed. Rising asset prices obscure the embedded risks while the boom persists. The buffer engages in building capital during the expansion, and then releases it when the boom turns into a bust. Conventionally, this is a welcome policy tool. It prompts banks to prudently build capital in the upswing of the cycle, in a way that cushions the downswing. It also provides supervisors with a macroprudential policy instrument that can be targeted in a flexible and calibrated manner without having to overhaul a complex rulebook. Europe has gone further. Several countries have implemented positive, early-cycle buffers—an innovation that emerged from the early days of the pandemic. Those buffers imply that the crisis cannot be faced by simply releasing the much-needed capital until a crisis emerges, because that capital would have been set aside during a safe cycle already.

The difficulty arises when the covenanted borrower is part of a group. Suppose a host country raises its buffer. Its local banks struggle to book as much credit for the local subsidiary. The authorities see less direct bank-to-bank exposure and might therefore consider that a tightened buffer is effective in safeguarding the country. Yet the group may simply reroute funding internally from the subsidiary toward the parent, in the form of cheaper, internal debt. The parent may then step up its borrowing at home, whether through banks or non-banks. The subsidiary is being shielded, while the host country shows greater safety, and the home country shoulders greater leverage. This is why cross-country capital buffers are not only prudential tools; they are also allocation devices; they are allocation devices. They, in fact, determine which jurisdiction carries the risk of an affected group.

Recent firm-level evidence presents an even harder fact. When the host country increased its buffers, credit to the affected subsidiaries fell by roughly 10%. However, their overall balances, and their leverage and default risk, did not decline proportionally. Instead, the parent substituted all of that missing debt with internal debt from the parent to the subsidiary. The parent company expanded its borrowing—both from financial intermediaries and otherwise—and increased its average default risk relative to its previous level. The policy was effective at the customer-bank border, but was it truly effective across the entire group? And does it ever matter where the default risk occurs, in light of supervisory oversight, when the goal is to contain systemic risk?

Europe has attempted coordination, but it has not eliminated leakage

Europe presents the best illustration of the challenge because policy has progressed further there than in most other regions. Despite the common banking union, national authorities still regulate a significant proportion of cross-cutting buffers—because credit cycles do not coincide. And rightly so. Spain, Ireland, Germany, and the Netherlands often do not experience the real estate price booms and busts, the structure of their banking systems, or the exposures of their households and non-financial corporations in a synchronized fashion. But the European macroprudential framework also admits that national interventions cannot be purely autonomous, because a common backstop is needed, and accountability is needed. As such, authorities inform the European Systemic Risk Board of domestic measures, and the supervisor of a member state can evaluate and potentially multiply the instrument if needed. Reciprocity in the application of the countercyclical capital buffer must be maintained up to a predetermined level between countries. For example, a bank originating in one member state must apply the host country buffer when lending to that country’s borrowers. This is a vital step in preventing a foreign bank’s arbitrage and in building a common lexicon of systemic concern.

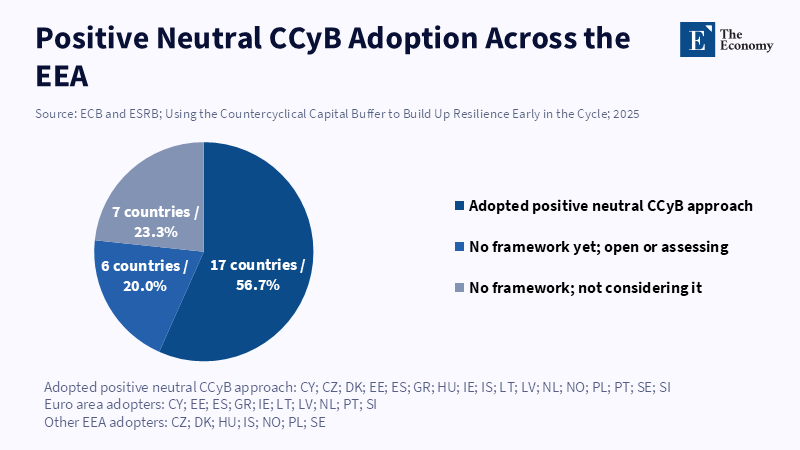

This represents invaluable progress. It addresses the broadest strawman to arbitrage: a foreign bank can keep on lending into an intensifying country, as if the local buffer did not exist. It also provides a shared understanding of systemic risk. The solutions outlined in the 2025 debate about positive, neutral buffers pointed toward pre-emptively building buffers that could be released earlier in the cycle. That strengthens the framework further. By 2025, seventeen European Economic Area countries will have adopted the positive neutral approach in their macroprudential strategies. The goal is not to make peaks higher—it is to have additional, readily available capital before the next storm commences. This is a valuable way to improve on a more passive system that only raises bank capital after risks are apparent, once markets have tightened and bank balance sheets have compressed.

However, this European model does not fully address the challenge of leakage. As it stands today, reciprocity relates only to how banks reciprocate a policy change. Reciprocity can constrain bank exposures, but it does not fully capture funding that moves through a multinational group’s internal capital market. Hence, the rebuttable presumption is that a group’s home country increases leverage and systemic risk—the home supervisor faces a seemingly elevated threat that it will have to bear operating losses when the local loan loss provision hits. The countercyclical buffer must be both a local safety device and a global risk mitigation device. As practiced, it is neither.

Why global coordination is harder than European coordination

Salient though this may be, the global challenge is, if anything, even more daunting than the European one, because there is no global fiscal backstop of the sort the European Union could facilitate through its own budget. Whereas European authorities have a very recognizable intragroup backstop at the global level, national interests tend to be more resistant to cooperation. Keenly aware of what they will inevitably face—namely, the wrath of voting constituents—national authorities want the risk to move outside their jurisdiction. Home authorities may enjoy the relative comfort of knowing that the official sector cushion in the home country can stabilize if risks emerge elsewhere. And host authorities will desire to set the buffer as high as possible, consequently penalizing the low-buffer systemic share domicile of the concerned group, and systemically encouraging risk displacement.

Local and macro-scale risks are balanced only in principle. In practice, a widened, openly disclosed buffer would be followed by a dissonant capital release announcement and the potential subsequent relocation of systemic risk. The political forces are too strong in every jurisdiction not to take this eventuality into account. To limit risk displacement, a concerted, explicit commitment to the timing, content, and communication around buffer releases is needed. For example, the country experiencing the buffer increase should proactively specify whether it will release it if it makes a subsequent decision to protect its banking system, and it should partner with other jurisdictions in releasing the buffer.

What a credible macroprudential reserve regime should do

A robust approach needs the following three steps. First, identify all relevant risks. For highly systemic banks and large-sized multinational borrowers operating inside complex regulatory frameworks, supervisors should cross-check country-specific stress tests with their own internal capital adequacy tests at the multinational group level. Impact scales should be extended to funding effects and cross-border funding choices. The relevant question is where the group would turn to find the next capital support: at the national bank, at the interstate parent, or another jurisdiction? Responses should factor into capital planning and crisis simulations, not only the planned drilling exercise. Second, require conditional reciprocity. In addition to guaranteed application of the host country buffer on direct exposures, practitioners should expect the home regulator to examine the leverage, default risk, and off-platform funding response provided by the internal capital market of an affected multinational group when the affected bank’s home country raises its buffer. This exercise should inform the subsequent assessment by supervisors and trigger capital countermeasures if needed. Third, create a better protocol for international buffer releases. Banks and markets need to believe that the buffers can be prudently deployed when necessary. The pandemic demonstrated that some banks chose not to utilize their buffers because the risk of market repricing was too high—markets would have reacted, and supervisors would have penalized them. While positive neutral buffers are intended to facilitate the predictable early building of capital for when the next crisis hits, international protocols should be set forth in a transparent way that discloses policies and anticipates potential effects, so as to make stakeholders less apprehensive and less dispirited as well.

A final test is the identification of a political compromise. Cross-border buffers are a half-solution, not an answer to the inherently fragile tension between the sovereign mandates that govern each nation and the reality of global financial groups. The task for more effective rules is nothing less than acknowledging that a buffer’s function is not to prevent a crisis, but to fluidly and predictably open or close the appropriate valve. When a buffer tightens, pressure crowding through the pipelines is inevitable. Regulators’ duty is to know where that pressure goes, who absorbs it, and who pays when it breaks. If a one percentage point buffer routinely reduces bank credit into affected subsidiaries by about 10 percent while leaving their structures and risks unchanged, then policymakers need to know explicitly—that is the lesson for the next crisis rulebook.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Agénor, P.-R., Jackson, T.P. and Pereira da Silva, L.A. (2022) ‘Cross-border regulatory spillovers and macroprudential policy coordination’, BIS Working Papers, No. 1007. Bank for International Settlements.

Basel Committee on Banking Supervision (2010) Guidance for National Authorities Operating the Countercyclical Capital Buffer. Basel: Bank for International Settlements.

Basel Committee on Banking Supervision (2024) Range of Practices in Implementing a Positive Neutral Countercyclical Capital Buffer. Basel: Bank for International Settlements.

European Central Bank and European Systemic Risk Board (2025) Using the Countercyclical Capital Buffer to Build Up Resilience Early in the Cycle. Frankfurt am Main: European Central Bank and European Systemic Risk Board.

European Commission (2008) State Aid NN 49/2008 — Belgium, NN 50/2008 — France, NN 45/2008 — Luxembourg: Emergency Aid to Dexia in the Form of a Guarantee for Bonds and Liquidity. Brussels: European Commission.

European Commission (2024) Report from the Commission to the European Parliament and the Council on the Macroprudential Review for Credit Institutions, the Systemic Risks Relating to Non-Bank Financial Intermediaries and Their Interconnectedness with Credit Institutions. Brussels: European Commission.

European Systemic Risk Board (2024) Annual Report 2024. Frankfurt am Main: European Systemic Risk Board.

Imbierowicz, B., Loeffler, A., Ongena, S. and Vogel, U. (2026) ‘How CCyBs travel — Internal capital markets and domestic borrowing’, Deutsche Bundesbank Discussion Paper, No. 12/2026. Frankfurt am Main: Deutsche Bundesbank.

Imbierowicz, B., Loeffler, A., Ongena, S. and Vogel, U. (2026) ‘How countercyclical capital buffers travel: Internal capital markets and domestic borrowing’, VoxEU/CEPR.

Nocciola, L. and Żochowski, D. (2016) ‘Cross-border spillovers from macroprudential policy in the euro area’, in Bank for International Settlements (ed.) Macroprudential Policy. BIS Papers, No. 86, pp. 45–48. Basel: Bank for International Settlements.

Tuominen, A. (2025) ‘Towards a more consistent EU macroprudential framework’, The Supervision Blog. Frankfurt am Main: European Central Bank Banking Supervision.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.