Fed Independence Is Now a Dollar Policy

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

Fed independence is now central to the dollar’s credibility Political pressure on the Fed can weaken trust, raise risk, and hurt currency value For a reserve-currency country, protecting the central bank is also protecting national financial power

The single most consequential figure in the 2025 dollar story is 10.7 percent. That was the decline in the dollar in the first half of 2025, the worst first-half retreat of the dollar in more than half a century. It was not merely market volatility. It was an institutional warning shot over the bow of Fed independence. A reserve currency does not trade only on interest-rate differentials, growth prognostications and safe-haven preferences. It also trades on faith in the rules governing the money. When the foreign investors' assessment calculus begins to shift towards the possibilities that the FX market is questioning whether the central bank can simply tell the White House no, the exchange rate is broadcasting a live institutional doubt indicator. The United States can still borrow in its own currency, still has deep markets in which to do so and still has no available rival. But reserve status is not a permanent title, only a daily evidence-based vote by foreign investors, central banks, banks and fund managers that this remains the case. That vote works like a market signal.

Too often today, we treat incursions against central bank independence solely as an inflation issue. Not wrong, but too limited. The undercurrent case is that if the central bank is in effect under political duress, it may ease out of sync by cutting sooner, holding out longer, or tolerating higher inflation for more time. But this may not be the most immediate consequence for a reserve-currency nation. The most immediate consequence may be read through the exchange rate. It is true that a depreciating dollar makes for more expensive imports and even higher U.S. yields and accordingly lowers foreign confidence in U.S. assets and can directly and immediately raise yields on that basis, even when policymakers want cheaper money. Here is the paradox at the center of Fed independence: the more a president tries to browbeat the central bank into delivering easier policy, the more the FX market will price the dollar as a risky asset. That is not to say that the central banker should never speak to politics. They must be in a crisis. The point is that only when the market believes that the Fed is still able to say no even to a bad order, can the central bank coordination gains be meaningful.

Fed independence is a dollar problem

The obvious fact is that the US president who seeks to manipulate the Fed is not the first. The Nixon-Burns episode remains the classic warning. What is different today is the combination of the forced public appeal coupled with legal confusion, a trade shock, fiscal limits and the dollar's position at the center of global finance. In 2025, the dollar slid sharply in April, even as the changes in UST yields created a characteristic relationship that, beyond doubt, should have lent stability to the currency. Instead, the dollar's depreciation came at a time when, again, UST yields in the US should have risen according to the classic risk-on scenario. Instead, the risk that was gnawing away at the dollar had turned out to have come from Washington itself after all. Tariff frights scarred the growth outlook, but the blowback on market trust in the Fed was even sharper when vocal suggestions about replacing Powell appeared at the same time. Now they moved the conversation to separately minded Fed independence and dollar moves.

Hence, the reason the exchange-rate channel merits more focus. Expectations of inflation are sluggish; there is a slow read of short-term inflation expectations, growth responses can be confounded by stimulus, tariffs, commodity prices, or global growth, but the dollar moves faster. It may not be a clear, one-for-one antidote to just one event, but it does communicate a stress indicator. So in April 2025, the dollar was communicating a simple message: the market was not only beginning to prepare for a slower United States, but was also beginning to prep against a fundamental change in the rules of macro policy. For a mid-size country, it may be only a credibility problem at home. For the US, it's a much bigger one. The dollar is the currency in which much of the world saves, trades, borrows, hedges and clears the risk. Hence, a dented confidence can ripple across countless balance sheets.

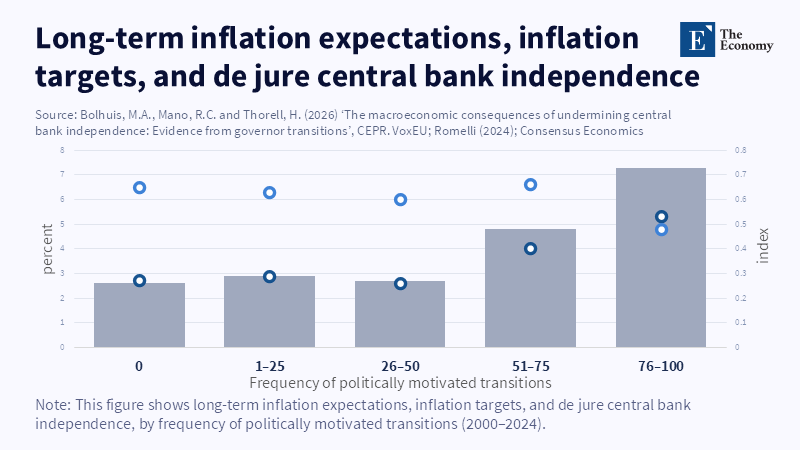

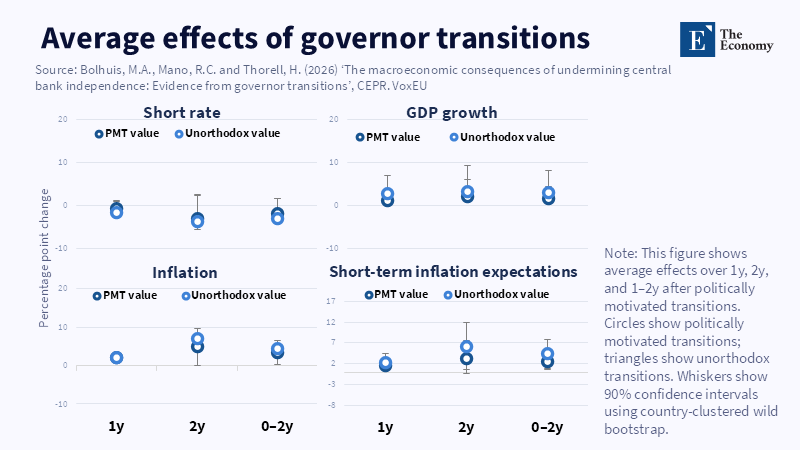

Exactly how important systemic politicizing of central banker leadership is may be forewarned by research that shows that when governors in effect plan to be picked through politicking, then short-term interest rates tend to fall and growth can temporarily accelerate. But if you get the temptation, then inflation and inflation expectations tend to shoot up and the long-run credibility of the system can come under greater stress if the system's pack of orthodoxy is subsequently eroded. This is not an account of technocratic superiority over populism. It is a market analogy to trust-based promises. When central bankers at the top promise to keep inflation low, then their credibility is only worth as much as the market's belief in the promise's durability over the looming election, recession, or debt crisis, whenever more favorable easy money is on offer. It is the institution of Fed independence that delivers that credibility. If it looks weak, then the market reflexively begins to reprice the currency.

The reserve currency premium is not free

The dollar functionally enjoys a great privilege, but it is not automatic. The data shows that global FX reserves hit roughly USD 13.14 trillion as of the end of 2025Q4. The composition is one step further removed from the physical: the dollar represented nearly 57 percent of the world's most elaborate FX reserves, well above the euro. A similar effect is observed in global FX trade: as of April 2025, an outstanding 89.2 percent of FX trades are carried out on one side by the dollar and in total, an average daily FX turnover amounts to USD 9.6 trillion. These data might be the reason that the credibility threshold of the Fed still carries global implications. While a normal central bank determines local liquidity conditions, the Fed is casually buoying the terms of funding to the single largest global reserve asset. That is not a local public good: it is a functioning, global fiscal asset. Institutional credibility has become a national competitiveness signal.

That is also why the dollar may depreciate before the reverse managers test it by large deviations. Official reserves move slowly, but private credit portfolios move far more quickly. The fact that foreign investors held some USD 35.35 trillion worth of value in U.S. securities by the end of 2025Q2 (even as the parallel number of total US holdings in long-term securities amounted to USD 35.35 trillion) means that the slightest hedge by a global portfolio can move the needle. This effect may not seem obvious, whether it comes from foreign investors selling treasuries or speculators bidding the currency forward, pension funds raising their hedge ratios, or multigenerational families exporting some part of their dollar-interest in U.S. equities to the euro or to bits of Japanese yen. But they will translate into a sudden effect on the margins, a seemingly slow-motion collapse in the market, because the decision is realized across a thousand private balance sheets.

The respect effect is that a kind of silent discount on the cost of borrowing and the support of the dollar goes into the national accounting. It does not show up as any line item in the budget. Yet the discount translates into lower risk premiums, the higher demand for Treasuries, the more affordable financing conditions for U.S. firms and the greater purchasing power of imports for U.S. households. As the IMF's 2026 study on central bank independence and sovereign local-currency yields showed, stronger independence is associated with lower five-year local-currency yields in emerging and developing market countries. Though the United States is not an issuer of emergent market currencies, the principle is clear: greater depth in the market can contribute to greater repricing. If investors treat the policy as diminished in its stability, then the effects will not be a few basis points higher. Instead, a slow, systemic, new tax will accrue to all those who borrow in the dollar currency to fund their operations.

The potential point of capture is not the same as a healthy state of policy separation

Today's honest critique may be that central bank independence can be oversold. Monetary policy should not be a template that makes a religion of dictum to keep eccentric politicians outside of. In times of war, banking crises, a pandemic and energy crunches, governments and central banks have to coordinate. Fiscal policy is the hand that controls the vote. Monetary policy is the hand that controls the dose. When the two hands behave as if the other does not exist, then the people pay. This fact is likely to be more important for a mid-size economy such as South Korea, Italy, or Spain that has less scope to buffer a large external shock domestically than a G7 economy. But even a country like South Korea, which is similarly subject to external disturbances, has to distinguish coordination from capture. The central bank has to have the freedom to keep a veto over inflationary pressure. A finance ministry can provide fresh data, solutions and financial choices on debt and spending, but it cannot set the rate. A president can argue the economy needs credit, but he cannot threaten to demote the fed chair if a rate is kept high. A central banker can stress the importance of price stability and even of employment stability, but cannot speak otherwise. Otherwise, the market prices the boundary. If they do not believe the boundary is real, then every rate cut looks suspect, even if the case is correct.

This is for the United States the key to independence. It does not need strict deference. It does need transparent separation of powers. The Treasury must provide the fiscal housekeeping. Congress must specify the budget procedure and borrowing limits. The Fed must buy its labor with prosaic disclosures and barebones transparency. If politics is over here and policy over yonder, then the market will instead adjust the exchange rate. Cheap dollars might look like a win in international value and international trade, but the United States is not a small open economy like other G7 members. It is the world largest issuer of the reserve currency and a disorderly dollar depreciation could turn into a permanent increase in U.S. prices and a durable inflation acceleration, sending the policy rate higher, not lower.

The final solution is not to provide the Fed with unappealable immunity. It is to settle its guardians along the lines of accountability. The best way is to be ready with a concise statement of how to turn the facility off again, a period of explaining itself in one sentence and a readiness to be tempered by Congressional channels when necessary. The best answer is disciplined transparency. The Fed should explain its rate decisions clearly, accept public scrutiny, and stay inside its mandate. But it must also be protected from removal threats based on policy disagreement. That is the line markets need to see.

To conclude, a 10.7 percent decline in the dollar in half a year does not prove that the Fed's independence therefrom is lacking. There were plenty of other influences: tariffs, growth worries, fiscal limits and dollar dominance in global finance. But the key for the time being is that a loss of belief in the rule-based integrity of the currency is a loss in FX market confidence in the Fed's ability to refuse to cooperate with unwise or unhelpful reasons to loosen. Without that dominance, a country's entire finance, debt and trading system can suffer. Otherwise, even the US debt ceiling can become a catalyst for a rising interest rate.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Abrams, B.A. (2006) ‘How Richard Nixon pressured Arthur Burns: Evidence from the Nixon tapes’, Journal of Economic Perspectives, 20(4), pp. 177–188.

Alter, A., Bersch, J., Touna Mama, A. and Quaye, B. (2026) ‘The credibility premium: Central bank independence and local-currency sovereign yields’, IMF Working Paper No. 2026/058. Washington, DC: International Monetary Fund.

Bank for International Settlements (2025) OTC foreign exchange turnover in April 2025. Basel: Bank for International Settlements.

Bertaut, C., von Beschwitz, B. and Curcuru, S. (2025) ‘The international role of the U.S. dollar – 2025 edition’, FEDS Notes. Washington, DC: Board of Governors of the Federal Reserve System.

Bolhuis, M.A., Mano, R.C. and Thorell, H. (2026) ‘The macroeconomic consequences of undermining central bank independence: Evidence from governor transitions’, IMF Working Paper No.., Bersch, J., Touna Mama, A. and Quaye, B. (2026) ‘The credibility premium: Central bank independence and local-currency sovereign yields’, IMF Working Paper No. 2026/058. Washington, DC: International Monetary Fund.

Bank for International Settlements (2025) OTC foreign exchange turnover in April 2025. Basel: Bank for International Settlements.

Bertaut, C., von Beschwitz, B. and Curcuru, S. (2025) ‘The international role of the U.S. dollar – 2025 edition’, 2026/040. Washington, DC: International Monetary Fund.

Bolhuis, M.A., Mano, R.C. and Thorell, H. (2026) ‘The macroeconomic consequences of undermining central bank independence: Evidence from governor transitions’, VoxEU Column, Centre for Economic Policy Research, 2 May.

Dixon, P. (2026) ‘Why does central bank independence matter?’, NIESR Blog, 19 January.

J.P. Morgan Asset Management (2025) ‘Where is the U.S. dollar headed in 2025?’, On the Minds of Investors.

Jones, K. (2025) ‘Why is the U.S. dollar declining?’, Charles Schwab Market Commentary, 28 April.

Nephew, E., Vu, H.L. and Wei, H. (2026) ‘Modest growth in world official foreign currency reserves’, IMF Data Brief, 27 March.

Romelli, D. (2024) ‘Trends in central bank independen

e: A de-jure perspective’, BAFFI CAREFIN Centre Research Paper No. 217. Milan: Bocconi University.

Shukla, S. (2026) ‘The hidden cost of central bank independence’, The Interpreter, Lowy Institute, 3 February.

U.S. Department of the Treasury, Federal Reserve Bank of New York and Board of Governors of the Federal Reserve System (2026) Report on foreign portfolio holdings of U.S. securities at end-June 2025. Washington, DC: U.S. Department of the Treasury.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.