The Oil Shock Is Not Overshooting

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

Oil shocks are real supply shocks They spread through transport, food and industry Policy must reduce forced oil dependence

The most relevant number in the oil debate today is not the day-to-day price of Brent but rather 20.9 million barrels a day. This was the amount of oil that flowed through the Strait of Hormuz in the first half of 2025, about a fifth of the world's daily consumption of petroleum liquids. A market can overreact when traders panic about a good that buyers can defer, substitute, or do without. Oil cannot: it is the fuel, feedstock and transport base of the modern economy. A geopolitical oil price shock is not a temporary mood swing in financial markets, but rather an attempt by prices to reckon with the degree to which the world's supply chains might be threatened with blockade, delay, or attack. And when the threatened good is oil, the price shock is not an argument about value but value itself.

Why a Geopolitical Oil Price Shock Is Not Overshooting

There is a grain of truth in the overshooting thesis. Market mechanisms are fast but often overshoot. They price in risk before the pipes are shut, before the tankers stop and before the refineries are in short supply. But this misses what a geopolitical oil price shock actually does to prices and the economy. It not only removes a tranche of today's barrels but also abruptly raises the probability of losing future barrels. This makes sense because oil undergirds much of the productive economy, providing mobility for people, for goods and for machinery, as well as serving as the feedstock for plastics, pharmaceuticals, fertilizers, solvents, asphalt, packaging and a myriad of other products consumed every day. So price is not only accounting for supply and demand, it is factoring in time, fear, storage, transit risk and a premium to keep assets online.

This is where the analogy with wine helps and fails. If war breaks out in an important wine-producing region, wine prices rise. Consumers have alternatives, such as beer, whiskey, water, or just saying no to drink. Restaurants adjust menus and shops can adjust inventory allocations. The damage might be real, but the market is narrow. In oil, the story is different: a shipping firm cannot find substitutes for diesel within the week, a plane can't suddenly switch from jet fuel to battery on a scheduled flight and a chemical plant can't operate without specific inputs. Farmers cannot easily avoid higher fuel and fertilizer costs simply because markets are pricing future risk. It's not that there are no substitutes for oil in the long term; it's just that there are too few for short-term, shock-related disruptions.

This timing is the critical policy challenge. In the long run, oil demand may decrease. In a crisis week, it is inelastic. Ships have cargo to deliver, routes to maintain and schedules to keep; trucks need to travel specific routes to customers and airlines need to refuel for departure. This means that while each party can try to cut usage slightly, the economy as a whole is inflexible. This is why a geopolitical oil price shock can feel much larger than a reduction in current supply: it highlights the economy's rigidity and signals how costly it is to maintain so many daily activities that run on oil.

The Supply Shock Hidden in the Price Spike

A geopolitical oil price shock should thus be understood in the first instance as a fundamental supply shock. Demand shocks are different. When oil demand grows sharply, higher prices can ration use, entice additional supply and signal economic dynamism. This higher price might even come with the bonus of higher income and production. An oil supply shock, in contrast, suggests a more ominous state: a necessity operating under much greater physical constraint. It also means prices are paid for essentials that must continue to be procured, imposing a direct burden on consumers. What looks like a speculative premium is better understood as a scarcity and security premium, paid because a critical input may be pushed beyond reach.

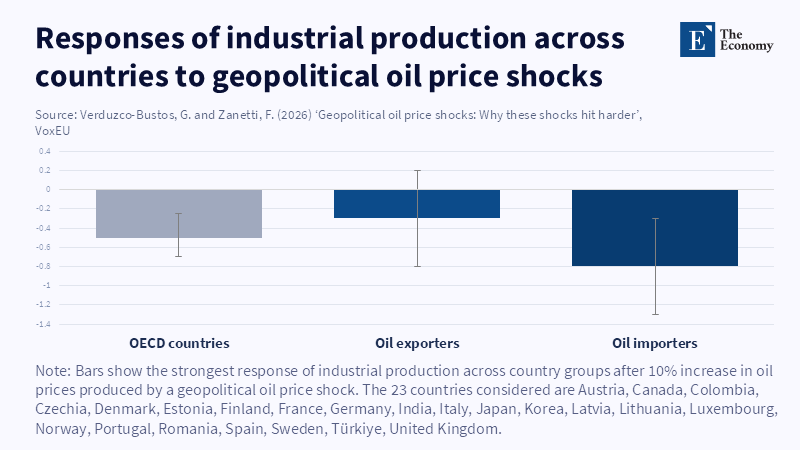

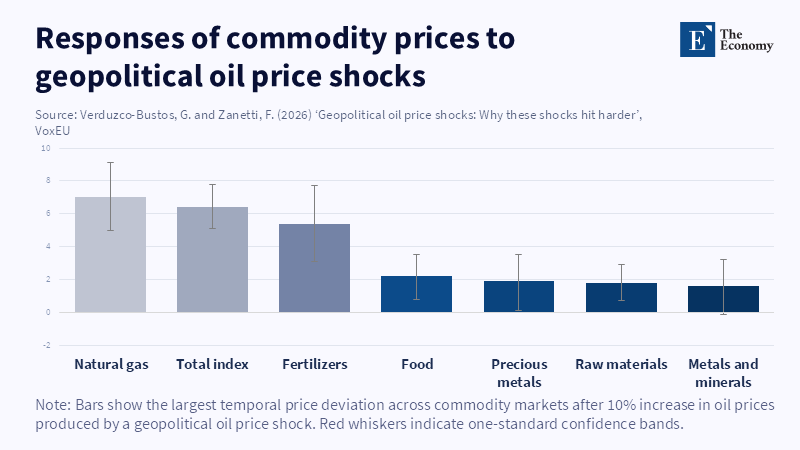

Recent data backs this up. Studies on geopolitical oil price shocks show that a 1% drop in oil output is associated with about a 11.5% increase in oil prices. That's much larger than one would normally expect of so small a change in supply. This market is sending an alarm that it believes the lost barrel represents an early sign of a broader supply threat. The same research shows that, for OECD countries, a 10% rise in oil prices triggered by a geopolitical shock led to about a 0.5% decline in industrial output and a 0.3% rise in consumer prices. Individually, not enormous, but directional. In a supply shock, output falls and prices rise.

The inventory response again shows why overshooting is not quite the right word. In an ordinary shock, inventory drawdowns can temporarily cushion the blow before the market returns to equilibrium. After a geopolitical oil price shock, however, there can be significant drawdowns followed by stock building. This might seem like an overreaction, but it does not look so when oil is treated as a security rather than a commodity. It is then that firms and countries build up oil stocks against future supply threats, keeping demand relatively strong even after the initial shock has passed. This may flatten price momentum, but the fundamental dynamics have changed. The market has learned that just-in-time energy is only truly cheap if the sea lanes, pipelines and political alliances supporting that transit are trustworthy.

Oil Is the Foundation, Not a Discretionary Commodity

Oil shocks are deeply destabilizing for a second reason: oil is not consumed in isolation. It supports much of the world's productive base. It fuels agriculture, health care, manufacturing, construction, logistics and defense. Petrochemicals show the issue. Oil demand in rich economies is now growing more slowly as a substitute for gasoline and more quickly as a feedstock for plastics and other goods. The IEA projects that global oil demand could rise by about 2.5 million barrels per day between 2024 and 2030, reaching roughly 105.5 million barrels per day by the end of the decade. This does not represent a burgeoning world of gasoline-consuming vehicles. It is a global dependence on oil-based materials.

Dependence on oil for transportation is just as crucial: in the EU, transportation accounted for 32.0 percent of the economy's final energy consumption in 2023, with road transportation accounting for 73.4 percent of total transport energy, petrol and diesel 88.7 percent and electricity only 0.5 percent. This is the sobering edge of green transition, and while electric cars are a breakthrough, the world's existing transport systems, in all their diverse configurations-long-haul trucks, utility vehicles, ports, construction machinery, ambulances, farm tractors, and aircraft-can not instantly shift gears. In consequence, the price impact of oil cannot be restricted solely to drivers of gasoline-powered vehicles. It propagates as it drives up the cost of moving goods everywhere, thereby affecting the price of almost everything we buy.

It’s not a failure of the transition. It’s a failure to break oil’s short-run power. Lower oil consumption by cars in some places has already reduced some of the risk, while growth in aviation, chemicals, freight and developing-world transport is keeping demand strong in other places. As a result, we are left with a divided system: while some oil demand is shrinking, much of what remains is becoming more essential and could make shocks worse, not better. A family can skip a car journey when fuel is expensive, a hospital can't avoid plastic supplies, a food transporter can't suspend the cold chain and a defense ministry can't ignore fueling requirements during a security crisis. While the marginal barrel looks smaller in long-term climate plans, it is vital in a real geopolitical crisis.

The inflation channel stems from oil's key role. Ordinary price rises can often be avoided or absorbed, but a price surge for oil is passed through many times, at the pump, in transport costs, then in product packaging, food and public services. A commonly accepted IMF estimate is that a sustained 10% increase in oil prices adds roughly 0.4 points to headline inflation, cutting growth by 0.1-0.2%. This modest estimate suggests the danger is less a single spectacular event than a broad squeeze.

Policy Must View Oil Security as Economic Infrastructure

The implications for policy are clear. Oil security can no longer be considered a 20th-century concept; during the energy transition, it must be treated as critical economic infrastructure. This doesn't mean stalling the transition. Instead, it calls for accelerating it in specific areas and reinforcing the existing system. Strategic reserves can play a role, but are insufficient: 20 million barrels a day flow through the Strait of Hormuz, far more than the alternative export capacity. Rerouting can partially alleviate this problem, but it can’t completely replace the existing system. A sensible policy response needs reserves, diverse routes, refinery flexibility, demand management and clear rules for stock release.

The language of prices needs refinement. Describing every geopolitical oil price spike as an "overshoot" can lead to inaction until the crisis has passed, even as the real economy feels its impact. A better rule of thumb is to assess what kind of demand is being priced: discretionary uses can absorb some fluctuation, while critical ones require an earlier response. Targeted fuel support can help. Critical transport routes and public transit can be prioritized and energy-intensive small businesses could be assisted with liquidity rather than blanket subsidies. Bottlenecks in chemical, fertilizer and medical supply chains need to be monitored. Central banks should clearly distinguish first-round energy inflation from wage-price spirals, acknowledging the impact of the former.

Of course, such a pragmatic policy view may be criticized as encouraging panic, with governments hoarding oil, offering subsidies and delaying climate action. This is a real danger, but the solution is not to deny the shock’s reality by deeming it an overshoot. The key is to foster resilience in a sustainable manner: make reserve rules-based, subsidies time-limited and targeted and efficiency policy a security measure, not just a climate one. Public transport, heat pumps, grid enhancements, recycling and resource efficiency can all cushion against future oil price shocks and the goal should be to reduce forced oil use rather than increase consumption.

Returning to the first point, with roughly a fifth of global petroleum liquids passing through a single chokepoint, oil prices are more than a trader’s mood indicator; they signal potential physical supply disruption. A geopolitical oil price shock represents a failure of expectations about a vital production input and policy should aim to mitigate future price spikes rather than simply validate market overreactions after the fact. Strategic planning must be bolstered by greater buffer capacity, accelerated, practical substitution efforts and a clear understanding of what sectors critically depend on oil. The oil-dependence system needs redesign; an overshoot is a temporary symptom of the problem.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Aastveit, K. A., Bjørnland, H. C. and Cross, J. L. (2023) ‘Inflation expectations and the pass-through of oil prices’, Review of Economics and Statistics, 105(3), pp. 733–743.

Baumeister, C. and Hamilton, J. D. (2019) ‘Structural interpretation of vector autoregressions with incomplete identification: Revisiting the role of oil supply and demand shocks’, American Economic Review, 109(5), pp. 1873–1910.

Caldara, D., Cavallo, M. and Iacoviello, M. (2019) ‘Oil price elasticities and oil price fluctuations’, Journal of Monetary Economics, 103, pp. 1–20.

Caldara, D. and Iacoviello, M. (2022) ‘Measuring geopolitical risk’, American Economic Review, 112(4), pp. 1194–1225.

Eurostat (2026) ‘Final energy consumption in transport – detailed statistics’, Statistics Explained. Luxembourg: European Commission.

Georgieva, K. (2026) ‘Coping and thriving in a fluid world’, International Monetary Fund, 9 March.

International Energy Agency (2025) Oil 2025: Analysis and Forecast to 2030. Paris: IEA.

International Energy Agency (2025) Strait of Hormuz. Paris: IEA.

Känzig, D. R. (2021) ‘The macroeconomic effects of oil supply news: Evidence from OPEC announcements’, American Economic Review, 111(4), pp. 1092–1125.

U.S. Energy Information Administration (2026) World Oil Transit Chokepoints. Washington, DC: EIA.

Verduzco-Bustos, G. and Zanetti, F. (2026a) ‘Geopolitical oil price shocks: Why these shocks hit harder’, VoxEU, 28 April.

Verduzco-Bustos, G. and Zanetti, F. (2026b) The Effects of Geopolitical Oil Price Shocks. CFM Discussion Paper CFM-DP2026-08. London: Centre for Macroeconomics, London School of Economics and Political Science.

World Bank Group (2024) Commodity Markets Outlook, April 2024. Washington, DC: World Bank.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.