The Hormuz Inflation Shock Is a Test of Reopening, Not Just War

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

Hormuz inflation depends on reopening speed Fast trade recovery could ease price pressure Policy should track ships before overreacting

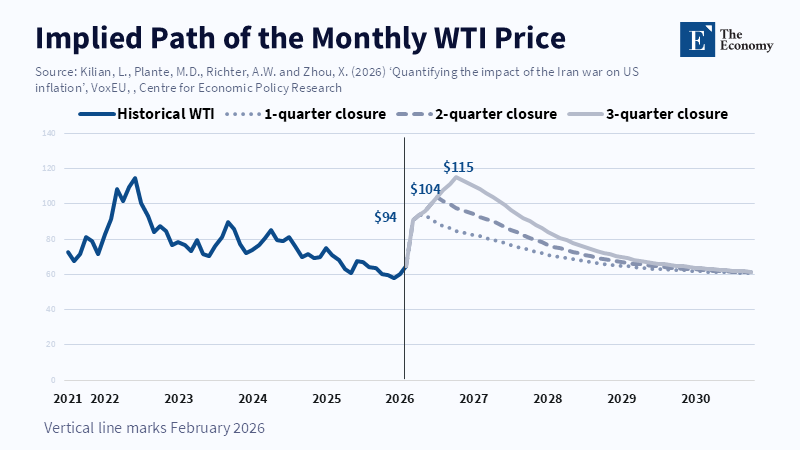

Every day, an average of 20 million barrels of oil and products pass through Hormuz. It is not an esoteric pipeline. It is a global economic pressure-relief valve. A disruption leads primarily to prices: an energy price hike, a rise in shipping costs and then food and fertilizer prices follow. But a more pertinent question than when Hormuz inflation occurs is when it recedes. The conclusion of a two-month halt in trade could be misinterpreted as the beginning of an era of entrenched inflation, if models only account for a gradual return to equilibrium, but an immediate and full reopening could have a much different outcome. Cargo will still be delayed. However, the delays, the backlog of export orders, the rerouting emergency and the restored confidence may push prices back down faster than the more cautious models allow. The policy risk, then, is simply to continue to fight yesterday’s surge when the supply is improving. The better way to read the crisis the most sensible course is to separate the crisis into two components, a physical shock and an expectations shock. The former is tangible and clear: lost barrels, lost gas, lost fertilizer, lost shipping. The latter is much more nebulous, the premium price consumers pay because they believe either that the Strait will not fully reopen, or that its reopening will not persist. The policy question ought to revolve around this second shock. The argument here is that if the Strait reopens in a matter of weeks and shipping picks up to its former scale, the market should not be treated like a damaged pipeline with slowly ongoing repairs; if the truce falters, then that will be the case and Hormuz inflation will become a test of central banks’ credibility rather than supply. The government ought to watch the ships, insurance, inventories and subsidies together, not just the price of oil.

The Hormuz inflation shock is a timing problem

Prices escalate rapidly because oil and energy are already woven into the cost of almost everything else: the fuel for the ship, truck, farm, airplane, refrigerated van and factory. In fact, A recent surge in consumer prices, for example, was driven almost entirely by the hike in gasoline prices, suggesting that the wider economy was likely still outside an era of new inflation, but a highly focused spike in a key price was quickly cascading into a wider measure of concern. However, the distinction is important; while the gasoline surge will probably reverse quickly when passage reopens, the beginnings of a self-perpetuating wage-price cycle would call for a very different response.

The same point holds true about the Hormuz market risk: it is possible that a gradual return to normality represents the logical, though not inevitable, outcome, not an intentionally crafted scenario. Once passage reopens, ships should begin to divert to Hormuz, insurance costs should decline, tankers should dock and producers should begin exporting closer to full available capacity.; the ensuing fall in prices may then occur much more quickly than in the cautious price recovery models. Although the households and firms would still have paid a premium for oil while the Strait was closed, the price dynamics are altered. Therefore, a sharp, short Hormuz inflation shock warrants a different policy response than one that persists for weeks or months.

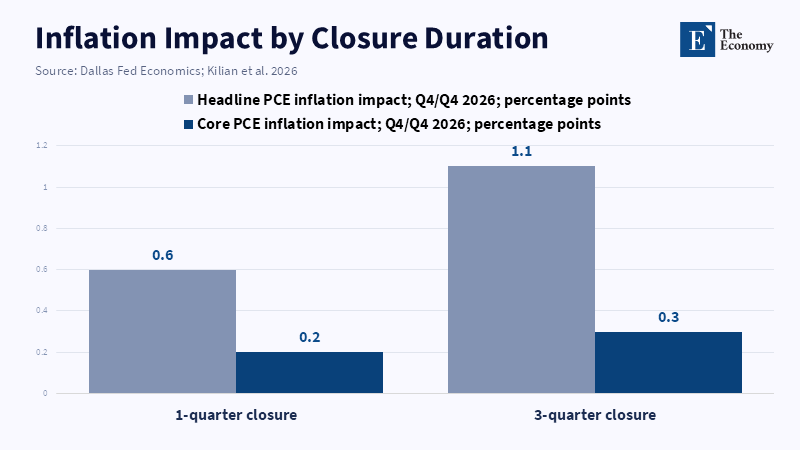

The timing of events also matters to inflation data; one month of surging prices is not automatically synonymous with an inflation regime shift for the whole economy. An increase in inflation above trend for the second and third consecutive months begins to carry significant policy implications if prices, wages and expectations are shown to be reinforcing each other and pushing higher. The key task, then, is to determine which prices have been affected-whether the surge is still largely contained within goods and services directly tied to oil and transit costs and has not yet fully cascaded into rents, services, contract agreements and wages. This distinction should guide policy decisions. In its absence, any price shock receives the same policy prescription.

Reopening can reverse panic, but only if capacity returns fast

The biggest argument in favor of price moderating inflation is the trade bounce effect. Most of the cargoes should eventually re-enter the supply system after the shock; oil stuck in storage can be re-released to market demand when conditions improve; and deferred orders will pick up once Hormuz fully reopens. This may create temporary congestion, but it should ease panic pricing if cargo flows return at scale. So, when the Strait reopens, the market price should be a few points lower than at the peak of the crisis.

The immediate weeks after a possible settlement will, therefore, be far more important than is currently suggested; a formal opening will not mean much. A limited number of successful passage attempts will be no more than a token gesture. Meaningful daily transit volumes, reduced insurance rates, a rapid increase in the number of docked ships and the return to normalcy will signal that the emergency has passed. Absent that, a partly open strait looks much like an embargo with the added risk of persisting price uncertainty: importers will continue to struggle to secure oil at reasonable levels, while producers will be unable to commit to full output volumes. For families, each hike in gas prices will serve as confirmation of the looming risk. Scale matters. Confidence itself constitutes a form of supply.

However, there are limitations to the trade bounce logic. The bypass capacity available to Saudi Arabia and the UAE can offset only part of the missing daily transit volumes. Reopening passage is the difference between a supply-clearing and supply-rationing market and it will not only affect Asian nations, but all price dynamics will shift. Barrels delayed on one route still affect the global price, because buyers compete across the same energy market. Consequently, the Hormuz inflation shock presents both a geographically confined and a globally impactful price shock.

Subsidies offer relief, not the underlying supply solution

Many governments will continue to provide temporary relief through subsidies, tax cuts, or price controls. These are not surprising. A rapid increase in fuel prices can impose heavy burdens on households that lack wage and welfare flexibility or company capacity to pass costs on immediately before internal mechanisms adapt. Particularly for certain segments of the developing world, price effects on food could be almost as direct: diesel prices feed into food transit costs and gas prices into fertilizer inputs. Every imported item will face the higher cost of transit insurance and shipping over time. For poor households already spending a high proportion of income on food, any price increase is significant – a foregone meal, missed bus trip, postponed doctor’s appointment.

Subsidies, however, may mask the reality during an energy shock. If they prop up reported prices for several weeks while a government budget absorbs costs, inflation figures could understate the real impact initially. If the Strait is reopened quickly, subsidies might help stabilize the economy, keeping consumers calm. If not, the intervention would become unsustainable- governments would be faced with the choice of either allowing prices to rise rapidly, or piling up debt at high interest rates. Unlike barriers, the core of subsidies must be a bridge; they can shield essentials, but can't mask the basic reality of a fuel shortage.

Port operators, shipping companies, hospitals, municipalities and other local governments must also realize that this isn't just about managing the shortfall-it's about managing the ensuing recovery wave. A rapid opening of trade routes would likely clog ports and transportation networks with ships and vehicles carrying urgent deliveries, suddenly pressuring authorities to handle a large influx of demand, customs clearance and delivery capacity at a high cost. If government offices are not properly prepared, their management of the recovery process could itself become a bottleneck. This is precisely where strong state capacity comes into play. Information about fuel stocks, shipping schedules, shipping costs and food purchasing needs will all contribute to preventing a supply shock from devolving into a management crisis. The shock to inflation at Hormuz will clearly not be only a monetary policy issue-it is fundamentally a logistics challenge.

The policy response must focus on pricing the recovery, not the rupture

Governments should not take the energy-driven inflation as a benign one; it is not. Since oil prices will affect people directly (via prices at the pump), expectations are bound to adjust upward and it is clear that transport and related goods would become much more expensive. This second round effect may eventually force wage demands. This is indeed a second-round effect that should be mitigated; however, this does not mean that any surge in oil prices should automatically imply demand beyond what an economy can afford. A higher interest rate may indeed reduce demand, but it will not open the Strait. An oil-led inflation shock that affects inflation, or wages and salaries, would surely be well-suited for rate hikes. In other instances, with a temporary price shock that is about to be resolved, there might not be much benefit in raising interest rates.

There is also a need for caution with regard to fiscal policy; blanket fuel subsidies are a clumsy tool. Not only do the poor and the needy benefit from it, but also the rich drivers will have the chance to drive and demand will not be reduced, even with supply scarcity. Better alternatives would include temporary transportation vouchers, targeted food subsidies for the poor, support for small transport companies and lines of credit for otherwise viable energy-intensive businesses. The port authorities and customs officials will have to manage not only shortages, but a potential overflow of goods once the bottlenecks begin to open. Energy ministries must make information on arriving shipments, current inventories and alternative routes accessible. Possibly, one of the most powerful anti-inflationary tools post-truce would be the tangible, indisputable evidence. That cargo is moving again may reassure consumers and prevent demand from overshooting due to fear. This might indeed not be such an optimistic view: the opening of a war-prone area cannot automatically guarantee the restoration of normal operations. Threats of mines, damage to infrastructure, militias, high insurance premiums and lack of trust between stakeholders can deter trade from recovering easily. The point is not to underestimate the challenge, but to underline that the recovery strategy must not be naive and must be contingent on how the Hormuz Strait is reopened. An opening of narrow trade channels and high insurance rates would result in higher inflation pressure than a fully restored and monitored channel. The latter will impact monetary policy, budgets, food security and public perception of the crisis.

One could perhaps criticize that a short-term shock may cause a longer-term backlash. Price adjustments may be slow from the business side once prices fall; demand expectations from households may be affected and businesses may start buying in larger inventories and Governments might even be compelled to allocate more public funds to security measures. Such effects are real, but they do not detract from the main argument; this is a post-shock event and not a regime shift. The policy must try to prevent a short-term crisis turning into a long-term one by stabilizing long-term expectations, by targeting temporary and timely subsidies and by communicating accurate information through public data and avoiding speculation. Of course, the authorities would have to accept that a catch-up will happen if trade fully re-establishes its operations. If not, the policy will be too tight and focus on worst-case scenarios only.

The above statement is founded on a general logic: a trade route that transports about 20 million barrels a day would cause export inflation during a shutdown, but a relief to imports during re-opening. Any later policy mistake would be to regard Hormuz's inflation shock as a constant; it would rather appear to be a varying parameter based on the dynamics of ships, trust, insurance premiums, inventories and opening time and speed. A fast opening of the Hormuz Strait, if a truce occurs swiftly, will imply that authorities must focus on managing the recovery instead of the crisis itself. If not, they must brace for substantial cost-of-living increases. It is essential that the speed of reopening is accurately measured, assistance be provided to those who bear the most brunt of the blow and the Hormuz chokepoint must not lead to sustained inflationary pressure.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Bureau of Labor Statistics (2026) ‘Consumer Price Index — March 2026’, U.S. Department of Labor, 10 April.

Dunn, C. and Barden, J. (2025) ‘About One-Fifth of Global Liquefied Natural Gas Trade Flows Through the Strait of Hormuz’, U.S. Energy Information Administration, 24 June.

Dunn, C. and Barden, J. (2025) ‘Amid Regional Conflict, the Strait of Hormuz Remains Critical Oil Chokepoint’, U.S. Energy Information Administration, 16 June.

International Energy Agency (2026) ‘Strait of Hormuz: About’, International Energy Agency.

Kilian, L., Plante, M.D., Richter, A.W. and Zhou, X. (2026) ‘Quantifying the Impact of the Iran War on US Inflation’, VoxEU, Centre for Economic Policy Research, 4 May.

Kilian, L., Plante, M.D., Richter, A.W. and Zhou, X. (2026) ‘Implications of the Iran War for U.S. Inflation’, Dallas Fed Economics, Federal Reserve Bank of Dallas, 17 April.

Kilian, L., Plante, M.D., Richter, A.W. and Zhou, X. (2026) ‘The Impact of the 2026 Iran War on U.S. Inflation: A Scenario Analysis’, Federal Reserve Bank of Dallas Research Department Working Paper No. 2609, 6 April.

Lippuner, M., Petrocchi, M. and Vermot, R. (2026) ‘How the Blockade of the Strait of Hormuz is Emptying Plates’, Helvetas, 23 April.

UN Trade and Development (2026) ‘Hormuz Disruption Deepens Global Economic Strain Across Trade, Prices and Finance’, UNCTAD, 1 April.

UN Trade and Development (2026) ‘Strait of Hormuz Disruptions: Implications for Global Trade and Development’, UNCTAD, 10 March.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.