China’s Stablecoin Retreat Is a Victory for Dollar Stablecoins

Authored On

Modified

Dollar stablecoins now dominate digital money China’s retreat shows control has beaten openness The real task is to make dollar stablecoins safer

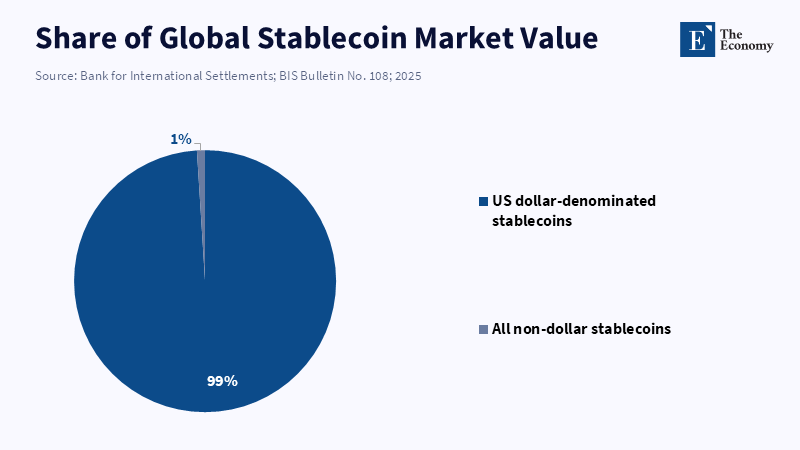

While roughly 99% of the stablecoin market cap today is USD pegged, China's newest digital currency move is less about another wave of crypto regulation and more about something entirely different. It is not the currency that matters; it is about which currency is going to be the default layer of settlement in the new digital economy of the future. It looked as though China may try to take on that layer by using an official digital Yuan coupled with an offshore pilot of a regulated currency, yet it has chosen instead to close the aperture on Renminbi, cracking down on foreign usage of currency and evicting privately backed RMB tokens. This is not a nation fighting for the open standards war-this is a nation that has surveyed the landscape, determined that being king of an existing settlement layer is a more achievable aspiration than fighting for the open one and that the dollar stablecoin currently rules that space. The tighter that China closes its borders, the clearer it becomes that, for payments in the cryptocurrency space, the dollar has already built the railroad.

Dollar Stablecoins Are the Market Standard

The simple narrative about the currency competition is too simplistic. As discussed above, in the past, there has been a narrative that China's early development of the e-CNY gave it a head start, while the US lags behind if it is too slow to develop its CBDC. This has clearly not been the case; instead, the development of private dollar-backed stablecoins led to an overwhelming dominance in the market over official digital dollars (or their lack). Dollar stablecoins succeeded first because the market already trusted the dollar's liquidity, depth and settlement role. Regulation is now turning that private lead into a formal policy advantage. A retail CBDC is not necessary for dollar stablecoins to exist in the US; transparency regulations are the critical component that allowed them to grow.

This regulation agenda is deserving of more scrutiny in the future. For China, cryptocurrency regulation is not just about the desire to control speculation. There are structural risks at play. For the renminbi to act as a leading stablecoin, it would have to cease acting as an inaccessible unit for capital control and instead become a fluid, widely redeemable asset. For the renminbi to act as an international settlement currency, it needs to be easily redeemed, settled and transferred. The dollar network exists; the renminbi does not. For the Chinese government, even an e-CNY that enables large-scale testing of cross-border wholesale settlements in this architecture will not represent a free stablecoin market; instead, it is a government-controlled digital money network.

The sheer volume and value in this market show how much this represents. Stablecoin volume is up by approximately 50% in 2025 and beginning April 2026 the total market capitalization surpassed $317 Billion. Though the fiat value seems small in comparison, it is the liquidity and usage of the assets that truly determine their significance. Stablecoins have become the lifeblood of crypto trading, decentralized finance, international remittance and global exchanges-it is a medium that allows for global settlement and in that world, the dollar has already made a lasting mark as the primary asset. As exchanges and markets price risk, settle collateral and transfer safe assets, it becomes apparent that this is the most convenient and reliable means in which to do so.

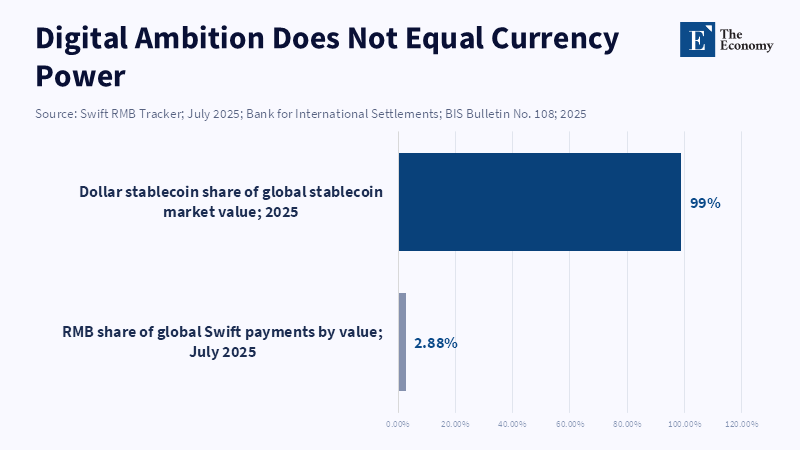

From the point of view of infrastructure, this is where the renminbi fails. As of July 2025, according to data from Swift, China's Renminbi is sixth for international payments in the world at an 2.88% market share. This isn't insignificant, but given China's tremendous trade volumes, it represents just how far behind its international presence has remained as the dominant financial infrastructure asset in comparison to the dollar; in terms of payments, reserves, debt markets, trade invoicing and safe asset flows, the dollar still reigns supreme and stablecoins are the digitized extension of that status quo. Market participants do not value a nation's public digital currency pilot more than a well-regulated, liquid and accessible asset with the most liquid backing in the world.

China Chose Control Over Stablecoin Scale

The stricter regulations for digital currencies coming from China should not just be thought of as a ban, but as a second-tier policy directive. China wants to achieve the benefits of settlement without forfeiting capital controls and desires cross-border flow without giving up full control. These objectives make sense for maintaining the internal economy but not for global leadership.

A Yuan stablecoin to rival the dollar requires foreign market adoption, large quantities of reserves backing the tokens, ease of redemption and most crucially, stability from government intervention. If private actors outside of China cannot have the confidence that their tokens will not be frozen at any given time, due to managed convertibility and strict capital controls, then foreign users will lack the confidence that the currency is viable as a freely-trading asset. This does not mean that China has failed at digital payments; its pilot project is the largest in the world and by late 2025, the e-CNY had already processed trillions of yuan in pilot transactions, showcasing state efficiency and a commitment to innovation. But transaction volumes in a regulated system and in private networks are not the same and while a state can impose adoption for services within its jurisdiction, it cannot do the same for global players without an underlying incentive.

The e-CNY Refresh dispels a common myth about China wanting to compete with the dollar directly on a token level. Since the e-CNY was modeled like a bank deposit for most of its design, it minimized its displacement from the existing banking system. This strategy makes sense for monetary policy and internal bank stability, but reduces the likelihood of the e-CNY becoming a globally disruptive currency and more of an internal system under the central bank's control.

There's also a chance China never really sought a private RMB stablecoin ecosystem to begin with. Partially, this is true. Beijing wants to keep crypto trading controlled. The difference now, however, is in the timing. After the US started regulating dollar stablecoins in order to open up the private market, China's crackdown from Hong Kong and beyond against the issuance of RMB stablecoins seems designed to ensure that it is seen by the market that only the negative consequences of privatized currency exist.

The US wins by enabling the private market

Yet, a weak response could have put the US years behind countries with different regulations in the space. America's stance on stablecoins is more explicit: it intends to regulate private dollar-backed assets rather than eliminate them with a retail CBDC. The GENIUS Act defines payment stablecoins as financial instruments subject to reserve, oversight, anti-money laundering and sanctions rules, meaning there are rules of engagement for public blockchain assets.

There is also the issue that there will be stablecoins runs. With multiple issuers of different qualities of reserves, a collapse of one stablecoin could impact all systems through complex and opaquely chained systems, cascading from crypto markets to short-term funding markets. It's why regulation is essential, but it is also clear that any public digital currency backed by private assets cannot be a completely risk-free proposal, but rather a less risky alternative to non-regulated products.

Compared to China, the US solution has a massive advantage: it accommodates the market. Consumers are demanding dollar stablecoins, private companies are building them and exchanges are listing them. Payment providers are already equipped with the tools they need to integrate stablecoins without having to wait for a central bank wallet to become widely adopted. It is less about building new infrastructure and more about strengthening the existing framework of the dollar with clear rules to avoid risks and manipulation. This is a far more appealing proposition than convincing the world to use a state-mandated token they have no prior demand for.

One area where China and the US diverge more clearly is regarding interest in stablecoins. In the US, regulators have suggested preventing stablecoin issuers from paying out interest to users in order to avoid blurring the lines between bank deposits and payment tokens, thereby preventing coin runs and avoiding an increase in financial risk. Regulators are pushing for stablecoins to maintain their characteristics as payment instruments; if they become investments, they risk distorting the market. China is currently allowing interest payments on stablecoins, yet in so doing, it is blurring those lines further and inviting an increasing amount of financial risk to its stablecoin network.

Dollar stablecoins help to enhance the value of the dollar without putting a burden on the global financial system. With the proper regulation in place, dollar stablecoins can stimulate demand for Treasury bonds, direct more dollar settlement into new digital applications and improve the reach of dollars into countries with failing monetary policies. Most importantly, this is a way for US regulations, sanctions and global financial policies to be enforced worldwide. This is what worries China: dollar stablecoins, despite being private infrastructure, can become direct mechanisms for propagating public policy across the globe and escape Chinese control.

An open system punishes closed ones

The stablecoin market rewards transparency, liquidity and trustworthy governance. Dollar stablecoins currently dominate because only dollars have demonstrated these qualities within a free and open global market. The dollar has not captured the stablecoin market; the market has simply identified that only the dollar is suitable to exist within this sphere of global payment rails. The renminbi will see growth as a currency in trade settlement, in swap markets, in commodity trading, in international payment systems and in wholesale CBDC, but it will not capture the lead for global stablecoin currencies without market participants who want it and an administrative apparatus to support its rise, an ambition that is clearly limited by Beijing’s stance. European authorities will also have difficulty. They may have an open and liquid currency, but it is far from achieving market adoption in the stablecoin realm. They may not be able to beat dollar stablecoins at their own game since a competitive product will require market liquidity, low prices, developers who will code and integrate the asset and a broader global reach. They will need a compelling reason for the public to want the token. The case of China reveals the fundamental truth: public digital currencies alone will not capture the private network competition.

The repercussions of this may be even worse for emerging economies, which can benefit from the use of dollars through stablecoins but can also undermine monetary policy and capital controls. Citizen demand for stablecoins will drive capital substitution, leading citizens away from their domestic currencies toward dollar-backed digital dollars, potentially undermining the economy. Those who view the stablecoin market as too small today may be in for a nasty surprise when the market continues its trajectory toward significant systemic importance.

Beijing represents one path and China, with its crackdown, is confirming a limited policy approach based on restrictions, regulations and a centrally controlled national digital currency to ensure internal stability, while hindering the renminbi’s global ambitions. On the other hand, the US's proactive approach to regulating private dollar-backed entities enables the market to build upon a foundation of established rules and provides the benefits of scale and network effects without sacrificing stability. This pathway of regulated private market dominance has allowed for the currency to build momentum as citizens and businesses choose dollars for liquidity, simplicity, collateralization and settlement capacity. Government policies will only serve to try to catch up with the public’s choice.

It would be more sensible to focus on creating realistic safeguards instead of striving for national digital sovereignty. Stablecoin issuers should prove the quality of their reserves, disclose timely information about them, grant explicit redemption rights, uphold custody rules and maintain AML and Sanctions compliance. Regulators must pay attention to all parts of the system that transmit risk to prevent system collapse and to safeguard the financial system during any coin run or Treasury market downturn. Governments should decide whether to pursue currency competition and strengthen domestic monetary systems or double down on existing financial mechanisms.

In conclusion, China’s tighter regulation of digital currency is not just a step toward controlling its financial system but also an acknowledgment of a loss in the race to dominate the stablecoin market. Beijing may continue to develop a sophisticated system of state payment instruments, launch its e-CNY in controlled markets, or further establish the RMB as a global payment unit for international trade partners. However, the independent, globally distributed stablecoin ecosystem has taken the other route, further entrenching the dollar as the dominant currency of the digital-asset world. The rise of the dollar stablecoin, in large part a consequence of the limited freedom Beijing refused to grant the currency, will leave it far behind. The goal is no longer multipolarity in stablecoin dominance but responsible management of the system, regardless of other nations’ potential desire for independent systems.

The initial statistics are stark and foreboding for all who are not in the US; 99% of the market capitalization of stablecoins is dominated by the USD. This is not a fleeting advantage but rather a fundamental network effect, one that is now a vital part of the broader global financial infrastructure. The increasing stringency of China’s control only reinforces this growing dynamic. The renminbi can become a digital currency, but without the openness that China refuses to offer, it cannot become the globally dominant stablecoin. Today's focus shouldn't be on the abstract ideal of a world of multiple stablecoins, but on developing practical safeguards for a regulated US dollar stablecoin system that can withstand global scrutiny, while other countries explore the option of challenging it or adapting. Digital currency did not democratize the world's monetary hierarchy; it made that hierarchy faster, more programmable and harder to reverse.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Aldasoro, I., Aquilina, M., Lewrick, U. and Lim, S.H. (2025) ‘Stablecoin growth – policy challenges and approaches’, BIS Bulletin, No. 108. Basel: Bank for International Settlements.

Blockhead (2026) ‘China draws a red line under tokenization, stablecoins’, MEXC News, 13 February.

Carapella, F., Lubis, A. and Vardoulakis, A. (2026) ‘Stablecoins in 2025: Developments and Financial Stability Implications’, FEDS Notes, 8 April. Washington, DC: Board of Governors of the Federal Reserve System.

Chorzempa, M. (2026) ‘China gives up on state-backed digital cash: The US and Europe should take note—for different reasons’, RealTime Economics, Peterson Institute for International Economics, 10 February.

Illes, A., Kosse, A. and Wierts, P. (2025) Advancing in Tandem: Results of the 2024 BIS Survey on Central Bank Digital Currencies and Crypto. BIS Papers No. 159. Basel: Bank for International Settlements.

Liang, N. and Dudley, W.C. (2026) ‘Next steps for GENIUS payment stablecoins’, Brookings Institution, 3 March.

Ma, B. and Xiao, C. (2026) ‘Beijing draws the line on digital dollars’, East Asia Forum, 14 May.

Society for Worldwide Interbank Financial Telecommunication (Swift) (2025) RMB Tracker: Monthly Reporting and Statistics on Renminbi Progress Towards Becoming an International Currency. August 2025. La Hulpe: Swift.

United States Department of the Treasury (2026) ‘Treasury proposes rule to implement the GENIUS Act’s requirements to counter illicit finance’, press release, 8 April. Washington, DC: United States Department of the Treasury.