India’s IPO Boom Will Not Mature Without Market Depth

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

India’s IPO boom is growing faster than its market depth Thin liquidity makes many new stocks volatile after listing Reform must build patient investors, wider float, and stronger post-IPO trading

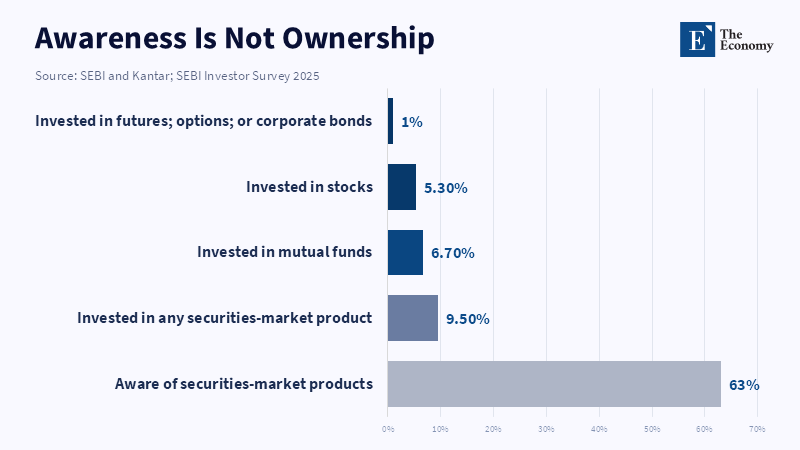

Only 9.5% of Indian households hold securities, but India is attempting to digest one of the most crowded IPO pipelines in the world. It's that gap that constitutes the true test of India's IPO market design. It's easier to tally the number of new listings, demat accounts, app downloads and oversubscriptions. It's harder to ask whether enough households have the wherewithal, faith and patience to hold shares after the opening bell. A market may appear deep on listing day only to shallow out a week later; prices shoot up, the herd moves on and the stock becomes hard to trade without accepting a poor price. India's next stage of reform, therefore, is not just about disclosure or expedited approvals. It's about making a market in which the average investor can buy, hold and sell without being penalized for thin liquidity.

India's IPO market design must rely on actual market depth

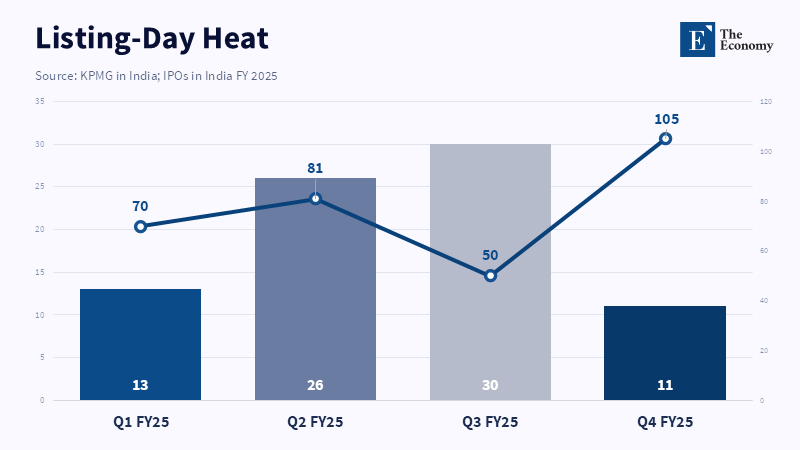

The success of the Indian IPO market is largely judged by its supply; more firms are listing, larger conglomerates are gearing up for public markets and domestic savings are pouring in through mutual funds. The exchange infrastructure looks robust, sleek and speedy. The Indian IPO market design should be assessed on its ability to move supply to ordinary demand. The IPO market is not a launch mechanism, but a system that enables private firms to become liquid public companies. This requires sufficient shares to be in public hands, a sufficient base of genuine buyers with differing investment horizons, robust analyst coverage and an adequate amount of market-making activity to maintain trading post-initial enthusiasm.

It's at this point that India's market shortcomings are most obvious. While the first day of trading in a liquid market will not be calm, the shocks are normally dispersed among a wide range of market participants. These include institutional investors, long-only funds, pension assets, retail buyers and arbitrage desks that contribute to the overall price discovery process. The theatrical aspect of price discovery in a shallow market could be based on the allocation of the IPO being rationed, speculation fueled by grey-market reports on expectations and the chase for a short-term gain. As liquidity dries up thereafter, the listed company itself might be solid, but the secondary market is not sufficiently deep to price its shares reliably on a daily basis.

The policy issue isn't a lack of public enthusiasm but potentially too much of the wrong kind. A market in which listing gains are considered the ultimate reward is likely to skew attention away from the years of ownership that public equities are designed to provide toward the very first trading session. India's IPO market design, therefore, needs to narrow the gap between subscription and sustainable demand. Regulators have an opportunity to alter offer terms, but they cannot magically instill market depth. Depth is a consequence of the availability of disposable risk capital in the market, of institutions capable of counterbalancing short-term price swings and of post-listing trading volume substantial enough to keep share prices in check.

A voluminous IPO pipeline can't replace a deep shareholder base

The obvious counter-argument to the foregoing points to the millions of new accounts opened up and to the broad social reach of Indian finance today. This is indeed true and of significant import. However, an account is not synonymous with a stable, active financial base; a demat account may never hold shares and trading apps may be encouraging small, speculative transactions even as household savings remain too tight to support long-term risk. While an SIP with a mutual fund may improve liquidity in an indirect manner, it doesn't guarantee that the new listed company will have stable individual shareholders. India's IPO market design needs to take these dynamics into account rather than operate in defiance of them.

It's for this reason that the household ownership data are more important than the headline figures on account creation. When fewer than one in ten households hold any financial securities, the market's primary support comes from a narrow social base. While the metropolitan areas of India may appear to be mature markets, many other areas still remain somewhat timid, under-informed or financially stretched to shoulder equity risk. This shouldn't be attributed to a lack of interest from the household. Rather, families with weak financial safety nets don't need to be admonished to become risk takers. They need steady income streams, contingency funds, trustworthy investment advice and an investment system that doesn't resemble a casino.

A similar conundrum exists with the derivatives markets. India can sustain substantial trading volumes but may still experience weak market depth if the bulk of this activity comes from short-dated, high-leverage derivatives. Volume is a misleading metric of a healthy market because it reflects activity rather than durability. A market active with weekly options can still lack deep cash equity markets and stable post-IPO share ownership. The lesson here for India's IPO market design is stark: liquidity fueled by rapid turnover may evaporate quickly when rules change, volatility declines, or a major participant withdraws.

This observation is also what leads to the realization that the loosening of float rules for large issuers alone is insufficient. Lower initial dilution may make it easier to draw large corporations to the market and may ease the immediate burden of absorption, but a thin initial float may exacerbate post-listing liquidity if the path to wider ownership is elongated. The correct equilibrium isn't a prescribed percentage for float but a staggered strategy for increasing ownership both before and after the listing event. This would involve timelines for expanding float, continued market-making support, a greater diversity of institutional investors and increased oversight over promoter influence and related-party transactions post-listing.

The true test of the listing is what happens after the fanfare. Companies can claim to be successful upon listing with minimal float and substantial pre-IPO demand, even when liquidity is poor in the secondary market. This also affects the company founders negatively: a thin secondary market leads to higher costs for future funding needs, makes employee shareholdings harder to value and transforms share ownership into a one-day event rather than a long-term pact with investors. India's IPO market design should instead focus on rewarding companies for cultivating a broad shareholder base both pre and post-listing and highlighting illiquid shares; a stock that sees minimal trading after a few days is not merely a private investor's problem but a symptom of an undeveloped market that is yet to earn daily investor trust. Ideally, this should be disclosed to investors prior to their investment with a clearer understanding of likely post-listing tradability, potential influx of additional shares and whether the current demand originates from long-term stakeholders or from speculators.

The next reform should be patient liquidity, not more access

India's upcoming reform cycle should make patient liquidity a public good by transcending the argument that mere access alone would rectify a nascent market. Access draws people into the market but liquidity retention keeps them from departing after a negative experience. The regulator needs to turn its attention to post-listing liquidity rather than simply focusing on IPO approvals. Issuers will need to meet stricter benchmarks related to float expansion, shareholder distribution, communication with analysts and ongoing disclosures. Exchanges will be required to produce simpler post-listing liquidity dashboards that provide investors with an overview not just of price performance but also turnover quality, bid-ask spreads and share ownership concentration.

For exchange/brokerage house and market institution operators the job is practical. It’s to map out the market trajectory once the stock is listed. This must include investor education on not chasing day one gains; improved warnings on illiquid stocks and clear segmentation of investment product versus speculative product. If nothing else has been learned from India's weekly options saga it’s that access without suitability just creates an illusion of inclusion by pushing losses onto the most vulnerable households. Financial educators need to speak of liquidity in simple terms – it's not just that the price can drop, but also that you may have no takers later on at any price.

The difficult part for policymakers, however, lies outside the exchange. A deep IPO market in India cannot be built just through securities law. It must also be built through rising real incomes, wider formal employment, enhanced pensions, better insurance coverage and trustworthy financial advice. The wider household base simply provides space for public markets to develop without each boom depending too heavily on a handful of institutions, affluent investors and short-term retail players. This is precisely why the design of India's IPO market is, in part, a development question. Markets cannot be much deeper than the household balance sheets from which people who sustain them are supposed to come.

The criticism that waiting for wealthier households would slow down India’s capital market ascent is, therefore, an incorrect reading of what needs to happen. It is not a question of waiting; it’s a question of sequencing reforms honestly. The government must continue to improve listing rules, attract significant issuers and expand digital access. However, it must cease touting the results as proof of existing market depth. The surer, slower path involves gradually building broader and larger domestic institutional participation, widening pathways for good public float, strengthening market supervision, simplifying disclosures and implementing financial education that acknowledges household capacity constraints. A market only truly matures when it acknowledges its areas of remaining thinness.

The headline number of 9.5% should remain at the center of the debate. If only a fraction of India's households are invested in securities, then the current IPO boom is not a mass capital market. It is merely a rapidly expanding one with a relatively shallow risk-bearing base, which may ultimately prove to be a historically successful venture if only subsequent reforms are judged by the market’s life after listing, rather than the first-day noise. IPO market design in India needs to facilitate fewer abandoned stocks, more stable pricing and more ordinary Indians who can sit through markets without fearing they are trapped. The mandate is simple: build the investor base, expand the float, police the pipes and make liquidity stick.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Agarwal, A. (2025) ‘Less than 10% of Indian households invested in securities markets, regulator’s survey shows’, Reuters, 30 September.

Hyde, K. (2024) ‘Explainer: The meteoric rise in India’s equity derivatives volume’, Futures Industry Association, 16 August.

Kapoor, A. and Senthil, P. (2025) ‘Neither solid nor liquid: The volatile state of Indian financial markets’, Institute for Competitiveness, 1 September.

KPMG in India, Tuteja, A., Mathur, S. and Sharma, M. (2025) IPOs in India – FY 2025. Mumbai: KPMG in India.

Navin, N. and Upadhyay, J.P. (2025) ‘India’s market regulator proposes allowing large firms to launch IPOs with smaller issue size’, Reuters, 18 August.

Reddit user (2025) ‘Indian F&O markets are super shallow’, Reddit: r/IndianStreetBets.

Securities and Exchange Board of India and Kantar (2026) Investor Survey 2025. Mumbai: Securities and Exchange Board of India.

Seth, R. (2026) ‘Market design is key to India’s IPO success’, East Asia Forum, 9 May.

Sinha, A. (2025) ‘India’s new trade strategy: From shallow agreements to deep value chain integration’, The Economic Times, 27 December.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.