China Property Crisis and the Price of a Smaller Capital Base

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

China’s property crisis is really a capital crisis The state can delay panic, but not restore trust by force China must shift from land-led growth to household and productivity-led growth

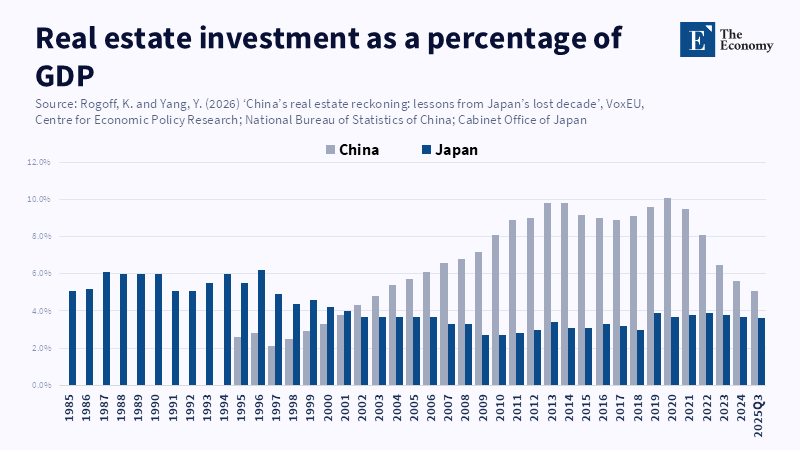

Investment in housing in China has halved in relation to its economy, dropping from 12.3 percent of GDP in 2020 to 6.1 percent in 2025. That single drop is more telling than a list of failing developers and unfinished high-rises. The China property crisis is not just about property; it is about capital. A sector that once absorbed savings, bank credit, household faith and foreign money, is now losing the fundamental support that once propped prices up. The state may be able to stave off collapse for banks; it can bolster equity markets with state funds and directed capital and it can keep bonds from morphing into an open panic. However, it cannot force households, firms and foreign capital to regard overpriced housing as a secure store of wealth indefinitely. This is why the Chinese property crisis has been so difficult to reverse. It is no longer a shock. It is a repricing of trust.

The Chinese property crisis is now a capital-base problem

The traditional explanation of China's property boom and bust suggests the state overbuilt and overleveraged and now has to deal with the aftermath. While this explanation is essentially correct, it fails to capture a crucial aspect: a real estate bubble, to survive, requires a broad base of support. This includes buyers who anticipate price increases, banks that view land as sound collateral, developers who foresee their presale revenues funding their next ventures and foreign investors who trust the political system to provide stability and not suddenly alter risks. Once this base erodes, a given volume of debt begins to feel significantly heavier and existing empty apartments become harder to ignore; the current model of local government funding becomes far less sustainable. Hence, China's property crisis is not just about excess supply, but also about the inevitable consequences when capital no longer wants to prop up that supply at the previously accepted prices.

Here, China is beginning to look alarmingly like Japan of the early 1990s. Japan's lost decade was not solely a result of a property crash. Underlying damage included a weak financial system, slow recognition of losses, insufficient demand and a long delay in clearing balance sheets. China, while maintaining more direct control over banks, land, credit and local governments and boasting stronger industrial policy and a large domestic market, is facing an increasingly narrow path in avoiding a similar trap. Between 2024 and 2025, investment in real estate development fell by 10.6 percent and 17.2 percent, respectively, while new construction starts fell by another 20.4 percent in 2025 and sales by floor area decreased by 8.7 percent. These figures are not merely weak, but rather indicate a market that is not operating in a typical business cycle, but rather a period of adjustment and fundamental rethinking.

The Chinese property crisis and the limitations of state intervention

The main policy question isn't whether Beijing has the tools; it has plenty. Instead, the issue is the strategic allocation of political and financial capital. Debt markets can be effectively managed, given that the majority of the system relies on state-backed banks, local government funding and governmental directives. Equity markets can also be shored up by state-supported firms and technology firms, but the management of a significant housing bubble offers fewer benefits. Rather than boosting the nation’s global competitiveness through high-end manufacturing and technology industries, it continues to tie capital into land and apartments, diverting it from strategic sectors while keeping households tethered to investments that no longer hold their perceived value.

As such, it appears Beijing may allow the Chinese property crisis to grind on rather than fully resolve it. While the state is actively involved in ensuring the completion of pre-sold homes, relaxing some regulations and attempting to absorb surplus inventory in select cities, the sheer scale of the problem dwarfs these interventions. By 2025, the surplus inventory remained equal to approximately 30 months of sales. Construction completion levels stood at almost 40 percent below the 2021 peak. Funding available to developers also continued its downward trajectory. In 2025, developers’ available funds fell by 13.4 percent. Deposits and advances receipts dropped by 16.2 percent, while individual mortgage loans fell by 17.8 percent. Foreign funding of developers fell drastically to just 2.5 billion yuan, an annual decline of 20.8 percent. A market can weather price declines; it cannot indefinitely absorb a crisis of confidence across all funding points.

The foreign capital story is critical to the speed of adjustment in the Chinese property market. China's current property slump is occurring in an environment of increasing trade tensions, global supply chain anxieties and geopolitical uncertainty. Inward FDI in China fell from 163.3 billion dollars in 2023 to 116.2 billion dollars in 2024, a 28.8 percent drop according to UN figures. Actual Chinese government figures recorded used FDI falling an additional 9.5 percent in 2025 to 747.7 billion yuan. Despite the rise in the number of new foreign-invested enterprises, the amount of capital invested in them has shrunk considerably. This disparity is significant. While foreign investors still seek access to the market, they are far more hesitant to commit large sums of long-term capital in an environment where political risks and declining demand are difficult to quantify.

The Chinese property crisis should provide a new curriculum for academic study

For universities and policy schools, the Chinese property crisis represents an valuable case study illustrating the interplay between capital markets and political systems. It should not be examined as a simple tale of moral hazard, nor as evidence that state-controlled systems invariably fail. A more constructive lesson is practical: the state can postpone a crisis, but it cannot eliminate the need for accurate pricing. It can keep a bank operational, but it cannot make illiquid assets sound. It can direct credit flow, but it cannot force households to purchase assets that they no longer trust. Business schools, economics departments and public policy programs should use this case to offer courses on balance sheet management, capital flight, local public finance and industrial policy as integrated topics, rather than as distinct subjects. The real value of this crisis to academics lies in these integrated lessons.

University administrators should also recognize the implications for global education. For generations, Chinese families have relied on housing wealth to finance schooling fees, education overseas and supplementary private tutoring. Falling housing prices, coupled with declining job prospects for young people, will lead to more cautious spending on education. Universities reliant on Chinese students must temper expectations by examining figures beyond headline GDP growth and considering the household capacity to spend. Despite China's 5 percent GDP growth in 2025, private domestic demand remained tepid, headline inflation averaged near zero and youth unemployment remained stubbornly high. This combination of factors is increasing student risk assessment and may reduce the demand for expensive degrees without strong job outcomes. Conversely, it may increase interest in programs related to data analysis, engineering, finance, public policy and risk management. The education market will not collapse, but its pricing and outcome-based approach will become much more pronounced.

The second lesson for policymakers should be clear. Future economics education must be less abstract. Students need to learn why a housing collapse hurts local budgets, bank lending, household spending, graduate job prospects and research grants simultaneously. Students need to know the difference between paths. In 1997, Korea, in 2008, the United States and in 2010, Greece all went through painful transitions in capital conditions. Japan chose a slower path involving a protracted bank cleanup and very low inflation. China is pursuing a third strategy, which supports the banking system, directs capital toward strategically important industries and allows housing to cease being its primary focus. It will likely be more successful than Japan's route, but only if the losses are not hidden so long that they infect new growth.

The Chinese property crisis leaves a narrowing path

The biggest objection to this argument is that the Chinese system is too highly regulated for a similar drag to occur as in Japan. The state can order banks to lend and local governments can be refinanced. Households do save an enormous amount and the state can construct, purchase, merge and absorb companies. This argument is valid, but incomplete. Regulation can cushion a fall and slow a cure. By keeping weak loans afloat, cheap credit continues to be available, although not well-directed. The continuation of local government services without a new revenue model can reduce private sector confidence by allowing for continued cuts to services and fees. A delayed reckoning for housing would keep buyers waiting and a regulated market is still capable of becoming a stagnant one.

China does have a way out of the lost-decade pattern, but the way forward is narrower than it was five years ago. First, the government has to stop seeing property solely as an issue of confidence. It is also a matter of price, income and trust. Properties will have to be re-priced and some developers must exit the market; some local debt needs to become explicit; banks need capital in order to absorb losses, not conceal them. Second, support needs to be shifted from assets to households. Households will not continue to consume if they fear for their employment and fear spending on education, healthcare and retirement. Third, foreign and domestic private capital should be encouraged, rather than treated as a temporary guest. If capital is only directed to the state industry, then growth will remain timid.

The opening number is still the warning. The shift from 12.3% of GDP spent on real estate investment to 6.1% is not a slowdown in an old engine of growth. It is a divorce of the Chinese capital markets from an overinflated asset class. China's real estate crisis is now the question of whether a government can burst a bubble without collapsing confidence. This is a policy lesson for instructors to teach, planners to plan on and officials to plan for. While inaction might preclude immediate panic, it will not provide a path forward. China has a strategy to avoid the Japanese lost decade but the state must recognize it will need a smaller capital pool, more truthful pricing of risk, greater support for families and greater growth coming from productivity rather than land. The decision is not solely on housing. It is whether a property retreat is capable of delivering a cleaner economic transition.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Bank for International Settlements (2025) BIS Data Portal: Debt Securities Statistics. Basel: Bank for International Settlements.

Board of Governors of the Federal Reserve System (2025) FRED Economic Data: Deposits, Debt Securities and Financial Market Indicators. St Louis: Federal Reserve Bank of St Louis.

Cabinet Office of Japan (2025) National Accounts of Japan. Tokyo: Cabinet Office, Government of Japan.

International Monetary Fund staff (2026) People’s Republic of China: 2025 Article IV Consultation—Press Release; Staff Report; and Statement by the Executive Director for the People’s Republic of China. IMF Country Report No. 26/044. Washington, DC: International Monetary Fund.

Kanaya, A. and Woo, D. (2000) ‘The Japanese banking crisis of the 1990’s: sources and lessons’, IMF Working Paper, WP/00/7. Washington, DC: International Monetary Fund.

National Bureau of Statistics of China (2025) Investment in Real Estate Development in 2024. Beijing: National Bureau of Statistics of China.

National Bureau of Statistics of China (2026) Investment in Real Estate Development for 2025. Beijing: National Bureau of Statistics of China.

National Bureau of Statistics of China (2026) Statistical Communiqué of the People’s Republic of China on the 2025 National Economic and Social Development. Beijing: National Bureau of Statistics of China.

Rogoff, K. and Yang, Y. (2020) Peak China Housing. NBER Working Paper No. 27697. Cambridge, MA: National Bureau of Economic Research.

Rogoff, K. and Yang, Y. (2026) ‘China’s real estate reckoning: lessons from Japan’s lost decade’, VoxEU, 11 May. London: Centre for Economic Policy Research.

Rogoff, K. and Yang, Y. (2026) A Tale of Two Countries: The Real Estate Crises in 1990s Japan and Present-Day China. Washington, DC: Brookings Papers on Economic Activity.

Shiratsuka, S. (2005) ‘The asset price bubble in Japan in the 1980s: lessons for financial and macroeconomic stability’, BIS Papers, 21, pp. 42–62. Basel: Bank for International Settlements.

UN Trade and Development (2025) World Investment Report 2025: International Investment in the Digital Economy. Geneva: United Nations.

World Bank (2025) World Development Indicators. Washington, DC: World Bank.

Zillow Research (2017) United States Housing Market Value Estimates. Seattle: Zillow Group.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.