The Monetary Policy Signal Is Now an Interpretation Problem

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

Monetary policy shocks often begin as interpretation failures, not true surprises Newspaper coverage, market reports and investors can distort the central bank’s original signal LLMs may help expose where human bias enters the policy communication chain

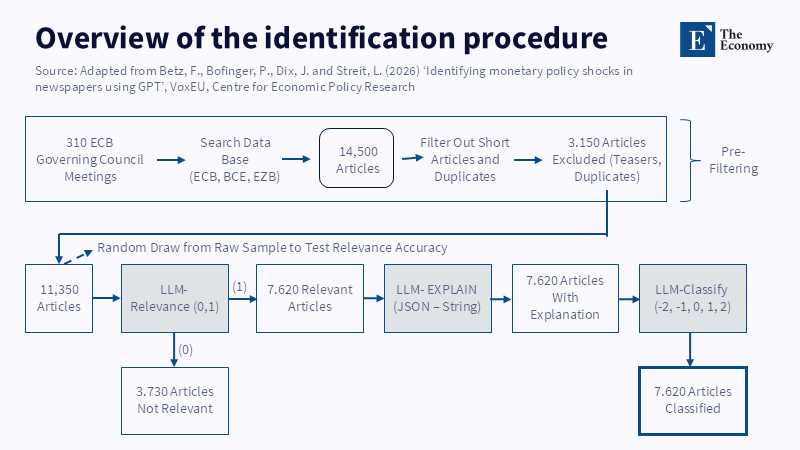

There once was a test wherein a large language model read through 11,350 news articles about decisions made by the ECB and identified only 7,620 articles deemed relevant to read. When a signal for monetary policy pings from a central bank to a market price, it does not go through the markets unchanged. It has to go through the draft of a speech, a press room, a headline, f a research note, the trading desk and the eyes of a borrower or saver who's on the other end of the line might already be biased toward one or the other. By the time the signal hits the eyes of a market participant, the policy might be hawkish, dovish, or remain unchanged, depending on when along the pathway it was modified. The point is pertinent in learning because courses are still teaching that monetary shocks are largely a function of surprises to the central bank. It stands to reason that by now, many shocks are in fact reading failures.

The monetary policy signal does not equal the shock

An easy way to show the problem is to give quantitative values to the piece of news. A tight surprise can be 2. A mild restrictive surprise can be 1. An expected policy can be 0. A bit of loose money can be -1. And a strongly expansionary surprise can be -2. Taking the article would not require guessing, but rather the disciplined practice of analyzing whether the article implies a policy more or less tight than an average expectation with meaning. What will be created is a newspaper monetary policy signal versus trade reaction, rather than a change in dollar price action or a change in 10-year bond yields. The difference is the heart of the problem. If a newspaper's monetary policy signal can foretell in advance a change in policy, then it was probably no "shock" when the policy change actually occurred. The newspaper has foreseen the event. The analyst who called the event a "shock" has read the signal wrongly.

If the newspaper-based signal does not forecast the policy change, two explanations are possible. Perhaps the central bank did not send statistically useful information, or perhaps the market interpreted the signal incorrectly. The initial results also indicate that monetary policy shocks, at least in the eyes of the press, are not nearly as widespread as is popularly believed. Roughly 1% of the newspaper articles examined predicted a significant policy shock, whereas about 2/3rds did not take a stance on the change (i.e., they can be classified as neutral indicators about the policy shift). Remember that the market considers central bank meetings to be high-profile. Even so, that is not what the data indicates; rather, meetings tend to reinforce (or slightly alter or delay) existing signals about the central bank's intentions. The pressing question is whether readers can tell the difference between true paradigm shifts and a gradual shift in the tone of communication.

There is a second way to approach the same question. A textual analysis tool designed to analyze ECB press releases in this period identified a boosting of forecast accuracy about interest rate decisions from 70% to 80% when the text was added to traditional economic variables. Not a huge jump, but a meaningful one—it demonstrated that there was information in the monetary policy signal that could be used before the decision was made. It also demonstrates that in the modern economics era, text should not be seen as just an adjunct to "real" data.

When monetary policy transmission takes a detour

The first possible cause of bias lies within the central bank. Unlike directive orders, language words used by central bankers are not explicit; they layer language as a means of steering markets without tying themselves down to a certain policy in the future when the data changes. Words such as dependent on data, persistent inflation, or sufficiently restrictive can be considered policy tools rather than neutral lexicon. Previous research proved that central bank communications could influence long-term yields more than interest rate changes. New text-based research shows that language is also a measure of central bankers' perception of the economy as a whole, risk and uncertainty. The second cause of bias is in journalism. Even when quoting directly, the meaning of the quote can change with its context. A quote is a snippet of intention, surrounded by a headline, a market reaction and a summary of market expectations.

Use of technical language also weakens as it moves into general news. "Pause" may not mean an indefinite pause on tightening, but may be interpreted as "wait now, but not forever." Similarly, "pivot" may not even be a line-in-the-sand moment for a rate cut, but be interpretable as "possibility of cuts in the near future, but is not a certainty." Those simplifications and distortions will broaden the reach of the monetary policy message but weaken it as well. The third bias is on the part of the reader. An investor who expects cuts might internalize the softer message, whereas an investor who is more worried about inflation might tout the more hawkish message. While it might be the opposite for a journalist and he or she might call it "cautious," the LLM might classify it as "restrictive." Indeed, that is what the new LLM evidence reveals. The relevance filter was implemented with 91% accuracy and the classification accuracy was 84%. Those are not tremendous scores, but they are fairly high and lead to questions about whether some human surprises are merely a series of personal biases.

The least obvious is the one that masquerades as expertise. Some market professionals are right that he can read between the lines and some are merely reading his old forecasts. This is an obvious problem in central bank communication, but it takes a new form over time. Central banks talk the same language to both the economy and policy. A rate hike could sound restrictive, while also reflecting the bank's view that the economy is doing well, but a cut could sound benign and represent the central bank having concerns about the economy. After all, surprises are usually both policy and economic surprises.

Teaching the monetary policy signal as a skill for general literacy

The policy lesson for teachers is clear: not only tell students what a cut in interest rates implies but also how the market for monetary policy signals evolves. A good economics course should prepare students to look at the text of the original central bank's statement and compare with the press conference, the newspaper articles of the next day, the reports of analysts and the market price of assets. Instead of simply asking "what happened", the exercise should ask where and how interpretations changed and whether this increased understanding or simply added further noise. Ironically, today's AI complicates (rather than alleviates) the urgency. Administrators should therefore treat this as a curriculum design issue. Separate departments for macro, journalism, finance and data science, widespread in business and economics schools, miss the point that the monetary policy signal connects all those disciplines.

Similarly, the same student who is asked to compile a central bank speech, to evaluate an LLM prompt, to forecast and to communicate to laypeople what has been learned might learn more from a class that enables him or her to complete the whole process than from a course in interest rate rules alone. On top of that, the class would probably do more to prepare students for a world in which LLMs are digesting news before the last headline reader has finished digesting it. Policymakers might take a more obvious lesson from these findings than the overall market and learn that they must subject their speech to machine evaluation, too, to prove it in the same way that they proofread it. This does not mean sacrificing voice to the machine; it means piggy-backing the speech through a set of algorithms that can serve as reader-analogies—economist, journalist, retail trader and tone-analogies; hawkish versus dovish.

When a wide dispersion of readings is tied to one message, it is not merely a market problem; it is a message problem. Clarity of central bank communications is not a public relations afterthought. It is a component of monetary policy transmission. Education leaders can also respond to this challenge by developing public modules on inflation, rate decisions and central bank terminology. They should be short, freely available and practical, not with the goal of turning citizens into bond traders but with the goal of narrowing the gap that exists between what policy is saying and what people think policy is saying.

The effect of the monetary policy signal issued by the LLMs will be tested on the markets in real time.

The most obvious criticism of an LLM is that it may make errors in text generation, have poor interpretation, or make crudeness of abbreviated thought. These are valid criticisms, but they are comparing the wrong; a faulty system cannot be evaluated by the perfection of human response, but rather be assessed against the realities of present information flows—rushed journalists, congested desks, predetermined views and ingrained incentives. Special-purpose LLMs show that whether reports from central banks require a language and knowledge base in a form seen before in general AI, but that their training on the latter can reveal departures from the true meaning perceived by a human. Another criticism relates to markets requiring price rather than newspapers. But price is not equivalent to dispassionate fact; it is rather a summation of traders' assumptions about the perceptions of other traders.

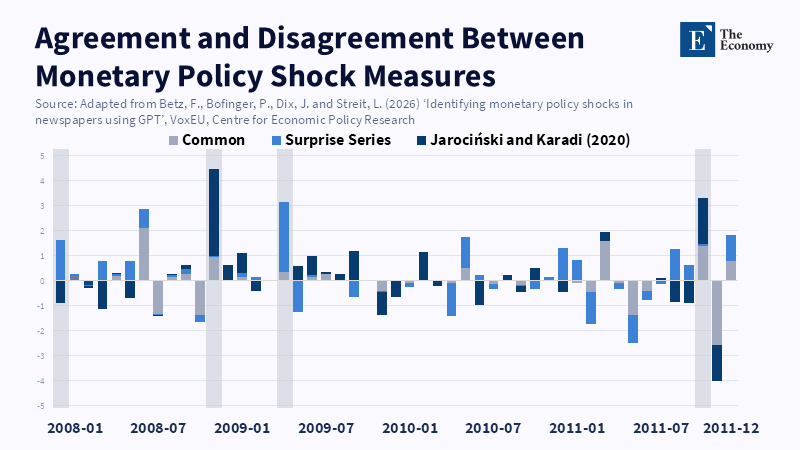

High-frequency data remains enormously useful, but methodological differences and sparse data points mean the picture of shock impact will vary. Text forms a valuable adjunct, providing the other side of the same incident. Agreement between market prices and a newspaper-based monetary policy message enhances confidence: divergence does not indicate one or the other must be wrong, simply that the divergence provides prudent information to be incorporated into the subsequent policy action. For the first time in years, the hedge fund industry will undergo the most rigorous test of all, where the value added of the management was based on subjective judgment, the ability to decode the deeper meaning of a central banker's speech and body language. In the out-years, the market may witness the imminent challenge of LLM systems to this theory and quicker, more common interpretations of signals resulting. If herding is encouraged, fragility may increase, or alternatively, a seminal insight will unfold: information is no longer enough; interpretation is what matters. The alarming statistic of more than 3,700 articles retrieved that could not meet a large-scale relevance screening underscores the enormous noise that encapsulates the financial industry.

Tens of thousands of found articles were discarded by relevance filtering. That's more than an insignificant detail. It reveals the sheer amount of static accompanying the money policy signal until it's consumed by investors, the media, students and the public. The takeaway. Any shock that could not be read is not a shock at all. It's a failure of communication. We should, thus, be teaching economics students the path from central bank announcement to news report to analyst note to market movement. Administrations should integrate macro, journalism, finance, and AI as skills rather than siloed subjects. Policymakers should pilot their wording through this entire chain before markets try out their experiments. Next-round monetary communication will hinge on clarity just as much as policy action.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Altavilla, C., Brugnolini, L., Gürkaynak, R.S., Motto, R. and Ragusa, G. (2019) ‘Measuring euro area monetary policy’, Journal of Monetary Economics, 108, pp. 162–179.

Bernoth, K. (2025) ‘Analyzing ECB communications improves forecasting of interest rate decisions’, DIW Weekly Report, 15(16/17), pp. 99–105.

Betz, F., Bofinger, P., Dix, J. and Streit, L. (2026) Identifying Monetary Policy Shocks in Newspapers Using GPT. CEPR Discussion Paper No. 21390. London: Centre for Economic Policy Research.

Betz, F., Bofinger, P., Dix, J. and Streit, L. (2026) ‘Identifying monetary policy shocks in newspapers using GPT’, VoxEU, Centre for Economic Policy Research.

Brennan, C.M., Jacobson, M.M., Matthes, C. and Walker, T.B. (2024) Monetary Policy Shocks: Data or Methods? Finance and Economics Discussion Series 2024-011r1. Washington, DC: Board of Governors of the Federal Reserve System.

Gambacorta, L., Kwon, B., Park, T., Patelli, P. and Zhu, S. (2024) CB-LMs: Language Models for Central Banking. BIS Working Paper No. 1215. Basel: Bank for International Settlements.

Gürkaynak, R.S., Sack, B. and Swanson, E.T. (2005) ‘Do actions speak louder than words? The response of asset prices to monetary policy actions and statements’, International Journal of Central Banking, 1(1), pp. 55–93.

Haldane, A., Macaulay, A. and McMahon, M. (2020) The 3 E’s of Central Bank Communication with the Public. Bank of England Staff Working Paper No. 847. London: Bank of England.

Hansen, S., McMahon, M. and Tong, M. (2019) ‘The long-run information effect of central bank communication’, Journal of Monetary Economics, 108, pp. 185–202.

Jarociński, M. and Karadi, P. (2020) ‘Deconstructing monetary policy surprises: the role of information shocks’, American Economic Journal: Macroeconomics, 12(2), pp. 1–43.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.