Europe’s Auto Market Tilts Toward Electrification as Chinese Brands Surge and Tesla’s Foothold Weakens

Authored On

Modified

European EV market expands despite infrastructure constraints

Stricter subsidy conditions steer production toward local sourcing

Tesla slump deepens, prompting pressure for strategic recalibration

As reliance on internal combustion engines declines rapidly across Europe’s automotive market, the shift toward electrification has gathered pace. Amid this transition, Chinese brands have strengthened their presence through price competitiveness and broader vehicle lineups, while European authorities have begun redesigning industrial subsidy frameworks to incentivize local production. As the market expands and regulatory rules are reshaped in tandem, the influence of Tesla—once seen as a symbol of the electric vehicle revolution—has instead shown signs of erosion, drawing attention to the underlying causes.

Chinese Brands Post Triple-Digit Growth

According to the European Automobile Manufacturers’ Association (ACEA) on the 3rd (local time), battery electric vehicle (BEV) registrations in the European Union (EU), the European Free Trade Association (EFTA), and the United Kingdom totaled 189,062 units in January, up 13.9% from 165,930 units a year earlier. Denmark, France, and Germany drove the increase, posting gains of 52.7%, 52.1%, and 23.8%, respectively. By contrast, gasoline vehicle registrations fell 28.2% year over year, including declines of 48.9% in France and 29.9% in Germany. Diesel registrations dropped 22.3%. As a result, the combined market share of gasoline and diesel vehicles fell to 30.1%, down sharply from 39.5% a year earlier.

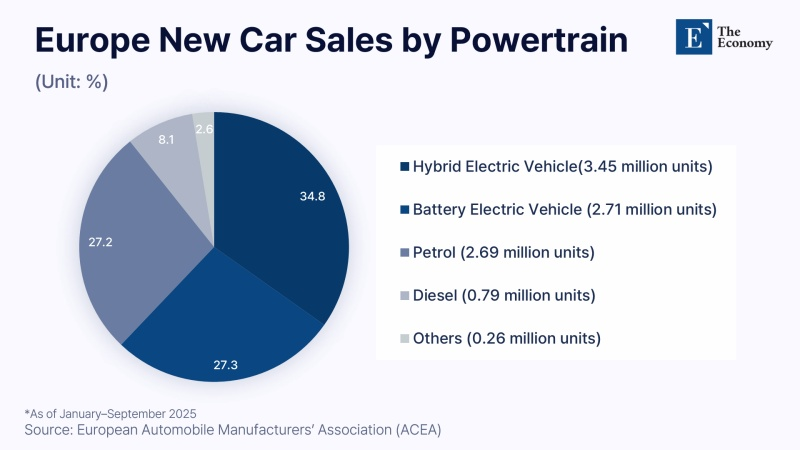

Electrification is not confined to a single vehicle category. ACEA’s analysis of new car registrations from January through September last year shows that hybrid electric vehicles (HEVs) led the market with 3.45 million units sold, accounting for a 34.8% share. This figure approaches the combined 35.2% share of gasoline and diesel vehicles. Over the same period, BEVs reached 2.72 million units, representing 27.3% of the market. Germany and the United Kingdom registered 382,202 and 349,414 BEVs, respectively. In Northern Europe, electric vehicles have surpassed internal combustion models in most countries, including Norway (96.8%), Denmark (68.7%), Sweden (62.0%), and Finland (56.6%).

A notable development is the rapid ascent of Chinese brands. Data from market research firm Dataforce show that Chinese automakers captured a 7.4% share of the EU, EFTA, and UK markets in January, nearly doubling from 4.0% a year earlier. BYD sold 17,630 units, a 173% increase year over year, while Chery recorded 17,106 units, up 354%. Other brands including Geely (384%) and Lynk & Co (183.2%) also posted triple-digit growth. Industry observers attribute much of this momentum to aggressive pricing strategies. In the United Kingdom, for example, Chery’s Tiggo 7 and BYD’s Sealion 5 are priced around $38,000, roughly $13,000 less than a comparable Volkswagen Tiguan hybrid.

Charging infrastructure remains a constraint on the pace of electrification. Across Europe, there is roughly one public charging point for every 13 electric vehicles, far below the industry’s recommended ratio of one charger per two to three vehicles. Waiting times, long-distance accessibility, and regional disparities inevitably shape consumer choices. The pronounced gap in EV adoption rates between infrastructure-dense countries such as Norway and Sweden and parts of Southern and Eastern Europe underscores this imbalance. Many in the industry view the pace of infrastructure deployment as effectively setting an upper bound on EV demand growth.

Subsidy Framework Recast Under a “European IRA” Model

Despite bottlenecks, electrification has become an irreversible trajectory, prompting Europe to recalibrate policies to encourage domestic production. A draft of the Industrial Accelerator Act (IAA) announced by the European Commission incorporates a “Made in Europe” principle. The proposal designates energy-intensive industries, carbon-neutral technologies, and electric vehicles as strategic sectors and would require a specified share of European-made components for eligibility in subsidies or public procurement. In the case of EVs, at least 70% of components—excluding batteries—would need to be produced within Europe to qualify for subsidies.

The policy shift reflects growing concern over the market penetration of Chinese EVs. Although the EU imposed tariffs of up to 45.3% on Chinese electric vehicles beginning in October 2024, their market share has continued to rise. The European Association of Automotive Suppliers (CLEPA) warned that up to 350,000 jobs could disappear from Europe’s auto parts industry by 2030. That projection has begun to materialize: in 2024 and 2025 alone, 104,000 workers left the European automotive sector. Germany’s ZF Group cut 7,000 jobs, Bosch reduced 13,000 positions in its mobility division, and Continental eliminated more than 10,000 roles. Employment pressures have strengthened the political rationale for tighter local production requirements.

These policy changes present new variables for global automakers that count Europe as a core market. Hyundai Motor and Kia, which together sell roughly 1.1 million vehicles annually in Europe, operate production facilities in the Czech Republic and Slovakia. However, many models in Hyundai’s Ioniq lineup and Kia’s EV series are manufactured in Korea and exported. If the 70% local production requirement takes effect, supply chain restructuring and production adjustments would become unavoidable. The IAA was initially scheduled for announcement on the 25th of last month but has been delayed amid internal EU debate over feasibility and potential cost increases.

Tesla’s Brand Premium Erodes

Meanwhile, the competitive landscape once shaped largely by Tesla has been rapidly reconfigured. In Germany, Tesla’s sales fell from 3,152 units in January 2024 to 1,301 units this January, a 59% decline. In Norway, registrations plunged 93%, from 1,108 units to 83 units. Similar declines were recorded in the Netherlands (1,619 to 303), Switzerland (749 to 68), Spain (749 to 512), and the United Kingdom (1,591 to 714). Although some markets such as Ireland and Austria posted rebounds, steep drops in larger markets including Germany, the United Kingdom, and the Netherlands outweighed gains elsewhere.

Industry analysts attribute Tesla’s decline to strategic misalignment. Europe’s market is expanding not only in BEVs but also in HEVs and plug-in hybrid vehicles (PHEVs). By maintaining a portfolio centered exclusively on pure BEVs, Tesla has struggled to adapt to the broader shift in demand. In an increasingly competitive environment, a narrow product lineup limits flexibility in adjusting specifications or diversifying drivetrain options. During the downturn in European sales, Tesla lacked a mid-range model capable of defending volume under evolving pricing structures, local subsidy conditions, and corporate procurement standards, resulting in a pronounced contraction in deliveries.

Another factor lies in the dilution of brand advantage amid intensifying competition. Traditional European automakers have rapidly expanded electrified lineups, diversifying models, price tiers, and distribution networks. Since the early 2020s, Chinese brands have further broadened consumer choice through varied segments and assertive marketing. As Europe’s market evolves from one dominated by a handful of brands to a multipolar arena with fragmented market shares, the dynamic in which a single brand’s leadership image automatically drove sales has effectively dissipated. The symbolic status of Tesla as the “leader in electric vehicles” is no longer sufficient to sustain its premium positioning.

Similar Post