"Securing Profit Stability Under Favorable Terms" Samsung Electronics and SK Hynix Expand LTAs, Cementing Global Memory Dominance

As one of the youngest members of the team, Tyler Hansbrough is a rising star in financial journalism. His fresh perspective and analytical approach bring a modern edge to business reporting. Whether he’s covering stock market trends or dissecting corporate earnings, his sharp insights resonate with the new generation of investors.

Authored On

Modified

Samsung Electronics and SK Hynix are rapidly entering into long-term agreements (LTAs) with global big tech firms Supplier-favorable terms, including increased prepayments and minimum price guarantees, are being incorporated With major countries struggling in HBM competition, Korea’s advantage is expected to persist

Samsung Electronics and SK Hynix are shifting their memory supply contracts from quarterly and annual frameworks to long-term agreement (LTA) structures. As a severe global memory supply shortage drives a surge in LTA requests from big tech firms, the companies are beginning to design stable profit structures by leveraging supplier-favorable terms. Market observers note that, given the lack of clear technological leadership in advanced memory among major countries such as the United States, China, and Japan, the competitive edge of Korean firms is likely to persist for the foreseeable future.

Expansion of LTA Adoption in the Memory Industry

According to industry sources on April 28, global big tech firms have recently been requesting LTAs from suppliers amid an unprecedented memory supply crunch. LTAs are contract structures that stipulate volume and pricing conditions over extended periods, ranging from one to five years. For customers, LTAs provide the advantage of securing stable supply during periods of shortage, while suppliers benefit from the ability to defend performance through pre-agreed pricing and volumes during downturns in demand.

From an investment efficiency perspective, LTAs are also highly effective. With transaction volumes already determined, companies can execute carefully calculated capital expenditures (CAPEX) instead of engaging in indiscriminate capacity expansion competition. This is particularly critical for high-value products such as high-bandwidth memory (HBM), where process complexity is high and customer requirements vary significantly. In such cases, securing orders prior to production enables a tailored supply system that fundamentally eliminates inventory risk and enhances mass production efficiency.

The market expects that as the proportion of LTAs increases, the average operating margins of Samsung Electronics and SK Hynix will stabilize at higher levels compared to the past. One industry expert stated, “Korean memory companies have emerged as indispensable strategic partners to big tech firms, underpinning the global artificial intelligence (AI) boom,” adding, “A strategic supply chain partnership has been established in which suppliers and customers collaborate closely from the technology development stage to ensure stable transactions.”

Contract Terms Tilted Toward Suppliers

However, if memory prices continue to rise, LTAs could also act as a constraint limiting the upside potential of memory companies’ profits. Financial markets generally expect semiconductor prices to remain on an upward trajectory for some time. Global investment bank Morgan Stanley projects that memory prices will follow an upward curve through 2027, driven by hyperscaler demand and growth in enterprise storage. UBS similarly forecasts that the DRAM supercycle could extend through the fourth quarter of 2027, citing the expansion of HBM production as a key factor structurally constraining the supply of conventional DRAM.

In response, Korean memory companies are incorporating binding conditions into LTA negotiations to maximize profitability. Notably, they have significantly increased prepayment requirements, which were previously below 5%. Under this structure, if a customer fails to purchase the agreed volume after contract signing, the prepayment is retained as a penalty. In practice, SK Hynix is structuring contracts with Microsoft (MS) and Google to include minimum price guarantees over the contract period, along with prepayment conditions amounting to approximately 10–30% of the total contract value. The agreement with MS centers on DDR5 memory supply over three years starting this year, with the total contract size expected to reach tens of billions of dollars. With Google, discussions are underway for a long-term general-purpose DRAM supply contract of up to five years, along with a potential two-year extension option contingent on next-generation HBM supply.

In some cases, LTAs are structured to fix only volumes rather than prices. This approach allows for adjustments to fixed transaction prices in line with future market conditions. In this regard, Ben Bajarin, CEO of market research firm Creative Strategies, stated, “According to multiple memory buyers, LTAs currently apply only to volumes, while prices are still negotiated quarterly,” adding, “This indicates that industry participants expect memory prices to continue rising.”

Global HBM Market Lacks Momentum

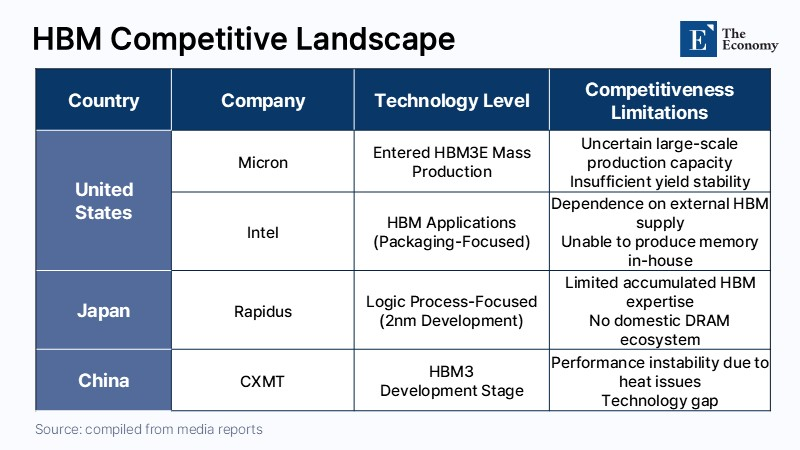

Industry observers believe that the current market dominance of Korean memory companies is unlikely to be overturned in the near term, as other major countries have yet to demonstrate competitiveness in advanced memory technologies. A representative example is China’s ChangXin Memory Technologies (CXMT). On April 21 (local time), IT outlet ComputerBase reported that CXMT has postponed its mass production target for fourth-generation HBM (HBM3) from the first half of this year to sometime after next year. The HBM3 chips currently produced by CXMT reportedly fail to maintain stable operating speeds due to excessive heat generation. This issue extends beyond initial defects and directly impacts long-term durability, bearing similarities to the challenges Samsung Electronics faced during the early stages of HBM adoption. At the time, Samsung spent more than a year and a half resolving thermal control issues.

Micron, a direct competitor to SK Hynix and Samsung Electronics, has entered production of fifth-generation HBM (HBM3E), but questions remain regarding its large-scale manufacturing capabilities. As process complexity increases further in the transition to sixth-generation HBM (HBM4), narrowing the gap with leading firms in the short term appears increasingly difficult. In the case of Intel, while the company has secured capabilities to integrate HBM into chips through advanced packaging technologies such as EMIB and Foveros, it still relies on external procurement for HBM itself. Notably, its flagship AI accelerator Gaudi 3 currently utilizes third-generation HBM (HBM2E) rather than HBM3E. This reflects not merely a product selection issue but a fundamental limitation stemming from the absence of in-house memory manufacturing capabilities.

Japan’s state-backed foundry Rapidus, established in 2022, is focusing on securing 2nm logic process technology and is developing next-generation transistor and packaging technologies in collaboration with IBM. However, it has yet to accumulate meaningful experience in core HBM technologies such as DRAM stacking, through-silicon via (TSV), bonding processes, and thermal management. To date, it has not disclosed any roadmap or generational strategy for HBM development. This is viewed as a fundamental weakness of Japan’s semiconductor industry. Following its exit from the DRAM sector in the past, the country’s related ecosystem has effectively collapsed, making the establishment of a competitive HBM mass production system in the short term highly unlikely. While Japan may participate as a partner in logic chips or packaging for HBM applications, catching up with Korean firms as a memory supplier remains a formidable challenge.

As one of the youngest members of the team, Tyler Hansbrough is a rising star in financial journalism. His fresh perspective and analytical approach bring a modern edge to business reporting. Whether he’s covering stock market trends or dissecting corporate earnings, his sharp insights resonate with the new generation of investors.

Similar Post