“Unusual Move”: Alphabet Turns to Samurai Bonds to Offset AI-Driven Financial Burden, With Low-Rate Lock-In Effect Expected to Stand Out If Japan Raises Rates

Authored On

Modified

Google Parent Alphabet Moves to Issue Samurai Bonds Amid Expanding Capital Spending Samurai Bonds, Long a Secondary Option for U.S. Firms, Previously Used Mainly by Financial and Investment Companies Such as Berkshire Similar “Yen Carry Trade” Effect Expected If Japan Raises Benchmark Rates

Google’s parent company Alphabet is preparing to issue yen-denominated corporate bonds, known as Samurai bonds, for the first time since its founding. With investment outlays expanding sharply amid an overheated global race in artificial intelligence (AI), the company is seeking to improve financial efficiency by tapping Japan’s yen market, which continues to operate under a low-rate environment. Market analysts say that as pressure mounts on Japan to raise its benchmark interest rate, Alphabet’s move could mark the beginning of a rapid shift in the standing of Samurai bonds across U.S. industry.

Alphabet’s Samurai Bond Plan

According to a report by the Nihon Keizai Shimbun on the 11th, Alphabet plans to issue “global yen bonds” targeting investors inside and outside Japan. The offering will be managed by Bank of America Securities, Mizuho Securities USA, and Morgan Stanley. The exact size of the public offering has yet to be disclosed, but it is expected to reach several billion dollars, with detailed terms, including the coupon rate, likely to be finalized within this month.

Nikkei analyzed that Alphabet’s move to issue Samurai bonds reflects increased funding needs stemming from rising AI investment. Alphabet’s capital expenditures this year, including data centers, are expected to expand 2.1 times from the previous year to $190 billion, with investment projected to rise further next year. Alphabet and other U.S. Big Tech companies have long financed such spending with cash generated from their core businesses, but as the AI investment race has intensified, their reliance on debt financing has steadily increased.

Indeed, Alphabet’s corporate bond issuance has grown from $10 billion in 2020 to nearly $40 billion last year. On the 5th, the company also disclosed that it had raised $17 billion through bond offerings worth about $10.5 billion and about $6.2 billion, respectively. The planned Samurai bond issuance is viewed as Alphabet’s strategy to optimize its financial structure by tapping the yen market, where interest rates remain low relative to the dollar market. The company appears to be seeking to lower its overall cost of capital and enhance financial efficiency by using low-cost debt capital.

Rare Use of Samurai Bonds in U.S. Industry

Markets regard Alphabet’s move as highly unusual. At present, the Samurai bond market is largely composed of international organizations, financial institutions, and Asian companies. There have been relatively few precedents of U.S.-based companies issuing Samurai bonds. Most U.S. firms can raise sufficient funding in the domestic dollar bond market, the world’s largest and most liquid market. Currency risk, Japanese financial regulations, and complex issuance procedures are also cited as factors limiting U.S. corporate participation in Samurai bonds.

The few U.S. companies that have issued Samurai bonds have been limited mostly to financial and investment firms such as Berkshire Hathaway. Berkshire Hathaway, led by Warren Buffett, issued about $1.8 billion in Samurai bonds in 2024. At the time, Reuters and other foreign media reported that Berkshire would use the proceeds for “general corporate purposes,” but the prevailing interpretation in the financial investment industry was that the move was aimed at securing funds to expand its stakes in Japan’s five major trading houses and pursue additional investments in Japan.

Since beginning investments in Japan’s five major trading houses—Itochu, Mitsubishi Corp., Mitsui & Co., Sumitomo Corp., and Marubeni—in 2020, Berkshire has aggressively bet on the Japanese stock market, raising its holdings in each to about 9% at the time of the Samurai bond issuance. The bond issuance effectively served as a foundation for raising low-cost funds in the yen market and making additional local asset investments. After the issuance, Berkshire increased its stakes in Mitsubishi Corp. and Mitsui & Co. to more than 10%. This year, it also announced the purchase of a 2.5% stake in Tokio Marine Holdings, Japan’s largest nonlife insurer, for $1.8 billion.

Japan Under Mounting Pressure to Raise Rates

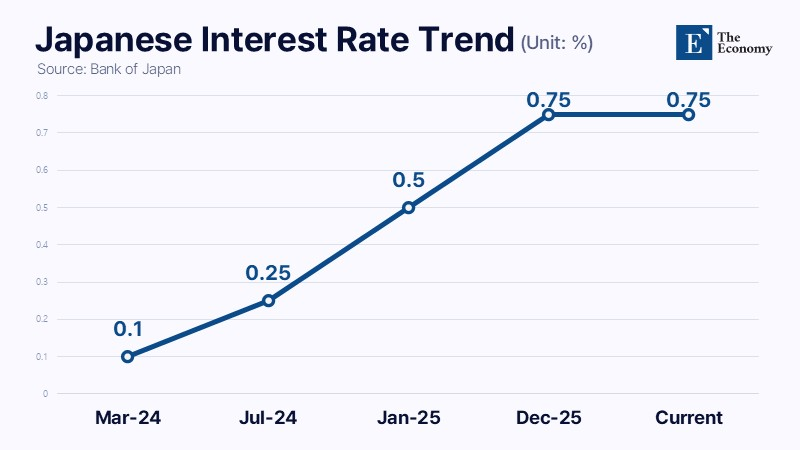

Some analysts, however, say the status of Samurai bonds, long treated as an exceptional option among U.S. companies, could change rapidly in the near future. This is because Japan may move to raise its benchmark interest rate. The yen is currently showing pronounced weakness, while Japan’s benchmark rate has remained low for an extended period. Under these conditions, companies that raise long-term funds in the yen market could expect an effect close to foreign-exchange gains if rates rise and the yen appreciates. The structure resembles the “yen carry trade” long used by global investors. The yen carry trade refers to a strategy of borrowing in yen, where interest rates are extremely low, and investing the funds in overseas assets with higher interest rates or higher yields to capture the spread.

Recently, the pressure on Japan to raise rates has become increasingly visible. The United States is a key factor. The U.S. Treasury has criticized Japan’s monetary and fiscal policies as excessively accommodative. U.S. Treasury Secretary Scott Bessent recently issued a direct criticism after the Japanese government intervened in the foreign-exchange market to stabilize the yen, saying that Japan needs “fundamental monetary policy, such as rate hikes.” In financial circles, expectations are growing that Bessent will urge Japan to raise rates during his ongoing visit to the country. Bessent arrived in Tokyo on the 11th and had dinner with Finance Minister Satsuki Katayama. On the 12th, he is scheduled to hold official meetings with Prime Minister Sanae Takaichi and Katayama.

The prolonged conflict in the Middle East is also an element of instability. Amid a high-exchange-rate environment triggered by the war with Iran, the Japanese yen has shown greater vulnerability than other major currencies. The dollar-yen exchange rate, which moved around 145 to the dollar early this year, has surged to around 160. This is viewed as a result of the Bank of Japan’s relatively passive monetary policy stance compared with major economies such as the European Union, the United Kingdom, and Australia, where central banks have shown moves toward rate hikes to contain inflationary pressure stemming from the Middle East. In addition, the structural characteristic of Japanese industry, which depends on the Middle East for 90% of its crude oil supply, is also cited as a factor deepening yen weakness.

- Previous “Amazon Embraces Even an Arizona Abandoned Mine” Copper Supremacy Reshaped by the AI War, Copper Rush Moves Into Full Swing

- Next "Chinese Shipbuilders Absorb Middle East-Driven VLCC Demand" — China Dominates General-Purpose Shipbuilding Market as South Korea Responds With High-Value Vessels and U.S. Cooperation

Similar Post