The End of the Peace Dividend

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

Europe’s peace dividend is ending Defence independence is becoming a political necessity Europe must now build its own security capacity

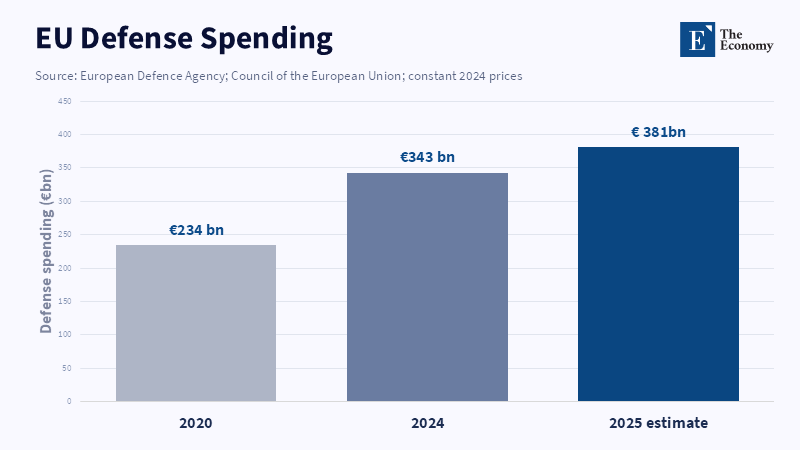

Europe's peace dividend can be reduced to one sharp turnaround. EU's defense spending is set to rise to 381 billion in 2025, from 343 billion in 2024 and more than 60% higher than in 2020. That is not the normal pattern of a budget cycle. It is a political Rubicon. For 30 years, Europe treated defense as a bill it could discount with the U.S., picking up the hard-edge cost of security. That age is over. The truth is not that Europe is drifting away from Washington in pique but that it is being forced back to act as a first-tier power. The peace dividend made room for building welfare states, economies and a rules-based union. Now the tab for that comfort is being called. European defense independence is no longer a dream; it is the price of strategic maturity.

The Peace Dividend Is Over

The previous peace dividend was premised on a simple trade. The U.S. supplied the main security umbrella while Europe made money in its shadow. They both called it an alliance. The terms suited their Cold War context. Soviet hegemony menaced Western Europe; the U.S. enjoyed unrivalled financial and military reach; European states had not yet overcome the trauma of two wars and were willing to cede authority to the U.S. After 1945, to avoid older power politics re-emerging. Even more so after 1989, defense budgets could decline, supply chains expand and security could become background noise. That is how the peace dividend became less a budgetary advantage and more a mental framework, teaching Europe to treat security as someone else's eternal burden.

This framework is now a danger. While Russia's invasion of Ukraine has not invented the problem, it has removed any excuse for neglecting it. Complaints about European free-riding are not new: Barack Obama already nudged allies toward higher spending, warning that special ties would fray if Europe continued to underspend. Donald Trump intensified the tone and added a transactionality that was missing in Obama's time, but the argument has been building for a decade. The difference is now that Europe is not merely being rebuked-it is being exposed. If U.S. Troops may be withdrawn from Germany, if weapons systems delivery is subject to political constraints and if access to U.S. Military equipment is tied to U.S. Political interests, the peace dividend is hardly cheap-it is an invisible dependence.

The statistics reveal the speed of the change. All NATO members met the old 2% defense spending threshold in 2025, with European NATO countries plus Canada boosting expenditure by 20% in the last year. The alliance has also increased its target to 5% by 2035, with funds allocated to both hard and broader security issues. EU statistics corroborate this shift in trend. Defense spending increased to 1.9% of GDP in 2024, with projections indicating 2.1% by 2025. Investment in defense, too, continues to rise dramatically, from 106 billion in 2024 to a predicted 130 billion the following year. Such figures may be attributed partly to a reaction to immediate events, yet they fundamentally indicate a transition of the peace dividend from an asset into a vulnerability.

European Defense Independence Becomes Industrial Policy

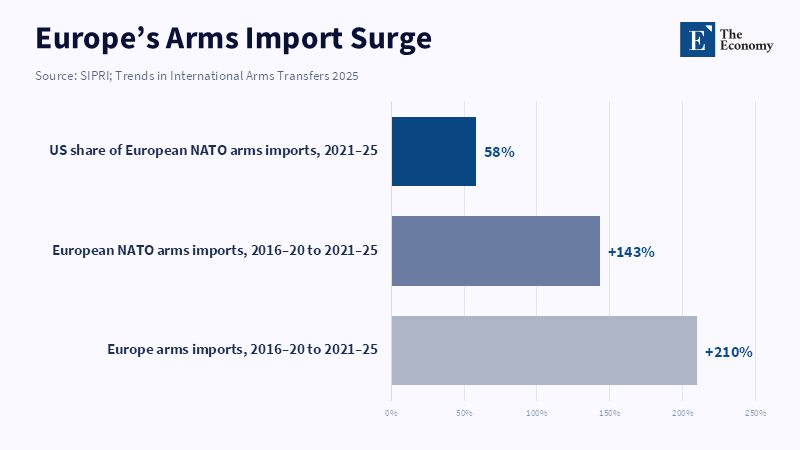

But raising money is not the same as achieving autonomy in defense. States that increase defense budgets may simply buy more equipment from abroad and Europe must avoid such an outcome. According to SIPRI's latest data on arms transfers, imports more than tripled from 2016–20 to 2021–25, nearly half of which came from the U.S. The new reality has thus become paradoxical: the more Europe spends on security, the more its imports could compound the dependencies it seeks to overcome. A Patriot battery, an F-35 fighter jet, or a missile system based on a U.S.-linked platform, while addressing immediate defensive shortcomings, provides another capital with a lever: a supply line, a queue for arms and a veto over military actions.

Hence, if the goal is European defense independence, the outcome cannot merely be rhetorical; it must involve genuine capabilities and production. Europe needs more factories, a more skilled workforce, greater stockpiles of matériel, secured software, a robust component supply chain and the capacity to repair weapons systems within its own borders. It requires air defense systems that can be deployed rapidly, drones that can be mass-produced, shells that last longer than a few months and command systems that function independently of foreign political will. The EU's Readiness 2030 initiative and the SAFE funding instrument, which aim to promote joint procurement, missile defense, drones, cybersecurity and stronger defense production capacity in Europe, have set the right priorities. However, the success of such initiatives hinges not on the funding levels announced but on their ability to translate spending into tangible results before the next crisis hits.

Skeptics might dismiss the notion of pan-European defense production as costly redundancy. There is some truth to this, though it cannot be the whole story. NATO standards are still important; U.S. Military capabilities remain essential; Europe should not construct a protectionist defense market that isolates it from reliable foreign technologies. Yet, the reverse is a far greater danger. A continent unable to produce sufficient ammunition, air defense systems, drones, or secure cloud technology cannot claim to have genuine freedom of action. European autonomy need not be a rejection of America; it must be the ability to weather a crisis in Washington. It also necessitates a transformation in defense budgeting culture, not blank cheques to national champions but investments in speed, common standards, joint orders and open European competition with the ultimate aim of usable power.

Germany and the Return of European Power

Germany serves as the primary indicator of this transformation, for it is a country that fully embraced the peace dividend. Its post-war development model relied on export dominance, a policy of fiscal prudence and strategic reticence. While the U.S. provided the security umbrella, Russia offered cheap energy and China absorbed German manufacturing goods, this framework was workable. Now all three elements have weakened. Germany's deviation from its previous debt limitations on defense and infrastructure expenditure, therefore, represents more than a budget revision; it signifies the leading economy of Europe accepting that power comes with a price. Germany will not emerge as a military behemoth, but it can no longer abdicate responsibility for the hard aspects of its own security, nor for carrying Europe's strategic burden out of sheer abundance.

The symbolic significance is profound. Since 1945, German military might has been viewed with suspicion; today, the weakness of the German military also represents a problem. Eastern Europe has reason to urge greater German urgency, as any delay incurs high costs. France, meanwhile, seeks greater European control over weapons systems whose deployment may depend on the approval of Washington. Lesser states would prefer an autonomous Europe, capable of action independently of any foreign election. Herein, a comparison to the old Concert of Europe might be relevant, but not in the sense of a return to exclusive great power clubs where smaller states are bartered over maps. Instead, the ideal would be a concert of capacity where dominant states assume greater responsibility, but within an agreed framework of common rules and standards.

The bigger change is psychological. For the last century, many European leaders took the fact that the ultimate strategic authority lay across the Atlantic as a given. They could resent its tone, resist war, or complain about US pressure, but they ultimately assumed the center in America would hold. That assumption no longer holds. The peace dividend evaporated first in the budget. It is now evaporating in the mind. This is why the issue should not be framed as Europe moving away from America, but rather Europe moving out of strategic depedence on America. Mature allies can cooperate and deter together without one being ever more the protector and the other ever more the protected client.

Capital is a part of this same story. It remains true that the U.S. spends more on its military than anyone else on Earth, but this expenditure no longer seems like a settled public good; rather, it seems like a market product that can be priced, delayed, or abandoned. Europe has learned that fact in the realm of energy, chips, cloud services, geopolitical risk and defense. That fact does not mean America is powerless. It means that American power is much more subject to its domestic politics, its industrial contractors and its shorter election cycles and it is on that premise that Europe must plan its defenses to be European. The old peace dividend enabled Europe to divorce itself from force and turn to wealth. The new one brings them back together. To gain political voice, Europe must gain a capital base, a supply base and a command base.

The worst outcome is not simply that Europe spends more on defense. It is that Europe spends too late, too narrowly, and too nationally. Overspending on rearmament without coordination, industrial policy without urgency, will result in conferences rather than weapons and it will fall once its inhabitants understand the tradeoffs that strategic autonomy requires. This requires an honest calculation by leaders. The demise of the peace dividend cannot lead to easily-made promises. Defense, energy, technology and fiscal policy are intertwined again and they all must fit in the same debate. Schools, hospitals and housing will not disappear, but it is naive to assume that defense will automatically safeguard them without investment.

Europe should use this moment for a clear bargain: Additional money for defense must generate additional capacity in Europe, additional capacity in Europe will strengthen NATO and additional strength for NATO depends on a Europe that will hold the line when Washington goes inward. That is the true demise of the peace dividend: no exit from America, no precipitous leap to militarism, but the assumption of a different responsibility. Europe spent three decades enjoying the fruits of peace. It must now invest in the structures of peace. If Europe seeks a power status, it will do so when it pays for, builds and plans as if it does. The peace dividend has run out, but the peace dividend predicated on it will endure if Europe decides that defense is not an American service, but a European duty.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Barrot, J.-N. (2026) ‘Europe will shape the 21st century’, speech at Columbia University, New York, 27 April. Paris: Ministry for Europe and Foreign Affairs.

Clapp, S. (2025) ‘EU defence funding’. Brussels: European Parliamentary Research Service.

Council of the European Union (2026) ‘EU defence in numbers’. Brussels: Council of the European Union.

Council of the European Union (2026) ‘What is Security Action for Europe (SAFE)?’. Brussels: Council of the European Union.

European Commission (2025) White Paper for European Defence – Readiness 2030. Brussels: European Commission.

European Defence Agency (2025) Defence Data 2024–2025. Brussels: European Defence Agency.

George, M., Djokic, K., Hussain, Z., Wezeman, P.D. and Wezeman, S.T. (2026) Trends in International Arms Transfers, 2025. Stockholm: Stockholm International Peace Research Institute.

Goldberg, J. (2016) ‘The Obama Doctrine’, The Atlantic, April.

Liang, X., Tian, N., Lopes da Silva, D., Scarazzato, L., Karim, Z.A. and Guiberteau Ricard, J. (2026) Trends in World Military Expenditure, 2025. Stockholm: Stockholm International Peace Research Institute.

Momtaz, R. (2026) ‘Europeans Are Quiet Quitting the United States’, Strategic Europe, Carnegie Europe, 5 May.

Murray, S. (2025) ‘French EU minister: Europe needs its own weapons to truly control its security’, Euronews, 13 March.

NATO (2025) ‘The Hague Summit Declaration’, 25 June. Brussels: North Atlantic Treaty Organization.

Psaropoulos, J.T. (2026) ‘Europe becoming arms powerhouse despite increased imports, says SIPRI’, Al Jazeera, 9 March.

Schneid, R. (2026) ‘The U.S. Military Drawdown in Europe Has Only Just Begun’, Time, 3 May.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.