The Strategic Peace Dividend Is Built, Not Assumed

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

Trade can support peace, but only when dependence is balanced China’s EV dominance shows why openness can become strategic risk A real peace dividend now depends on AI hardware, resilient supply chains, and allied industrial strength

Global military expenditure reached $2.887 trillion in 2025. That is the floor below any credible argument for a strategic peace dividend. The world isn't heading into a tranquil, post-war era. Instead, it's spending more on force and, simultaneously, on increasing trade, building more data centers, subsidizing more factories and testing the strain limits of open markets. The classic liberal argument-that trade makes war more expensive-still applies, but it loses some luster when the trade balance is off, when one country holds the manufacturing base and the other largely supplies capital, patents, software and the final market. A strategic peace dividend won’t appear simply by lowering barriers. It will depend on trade that is balanced enough to prevent conflict, resilient enough to survive shocks and selective enough to protect the industries that will define the next global standard.

Strategic Peace Dividend Needs Leverage

The argument for trade peace has always been fairly simple. When two states sell to one another, lend to one another and depend on one another’s ports, firms and consumers, warfare becomes costlier. That’s why the argument for a liberal peace remains useful. It is not to claim that commerce eliminates war, but that it alters war's price. More recent scholarship has provided real backing to this assertion: a doubling of bilateral trade, for instance, is shown to be correlated with a 20 percent decrease in the likelihood of militarized disputes between states. This is a significant contribution, as it transmutes moral assertion into empirically testable policy. Trade can be a peace dividend tool.

Yet, these findings are frequently taken too far. Trade interdependence does not always mean peace interdependence. Whether or not this is so depends on what one is trading, on who receives value and on whether a state could be easily replaced in times of crisis. Trade in wine, tourism or low-end consumer goods operates differently from trade in chips, batteries, rare earth minerals, power systems, ports, cloud platforms and machine tools. The first type of trade produces mutual loss. The second type can foster mutual fear. A country that relies on its rival for vital inputs will not feel more secure. It will feel cornered. In this case, de-risking is not protectionism; it is the pursuit of leverage.

The policy mistake is to view all trade barriers as equally dangerous and all openness as equally pacifying. This approach is too simplistic in the contemporary world. Trade reached about $33 trillion in 2024, but defense budgets still grew. This is not a refutation of the peace dividends trade can generate. Rather, it reveals the limits of this approach. Peace is not an inevitable outcome of substantial trade flows. Peace is a by-product of credible restraint: the conviction that both countries would be injured in war and neither has the upper hand by cutting the other off first.

Uneven Trade Weakens the Strategic Peace Dividend

The US-China connection is now a test of national competitiveness, not only trade volume. Despite their deep trade ties, the relationship is asymmetric. In 2025, US trade with China was $414.7 billion. US exports accounted for just $106.3 billion of that, while imports reached $308.4 billion. This disparity is more than just a headline number; it signifies the unevenness of the trade relationship. The US is a major importer of manufactured goods, while China exports far less to the US and is actively climbing the value chain. The result is not comfort, but an intricate network fraught with flashpoints.

Because of this asymmetry, it's possible that lower barriers could exacerbate the potential for conflict between great powers. If lowering trade barriers disproportionately benefits one state, allowing it to expand its industrial base, set new standards and undermine the other country's manufacturing sector, it could ultimately reduce overall stability. Consumers gain from cheaper imports, but weaker firms suffer. Over time this leaves countries with high levels of demand but fragile production capacity. The threat isn't in trade itself, but in a trade relationship in which one country possesses the factory floor and the other holds the credit card. This foundation will not sustain peace.

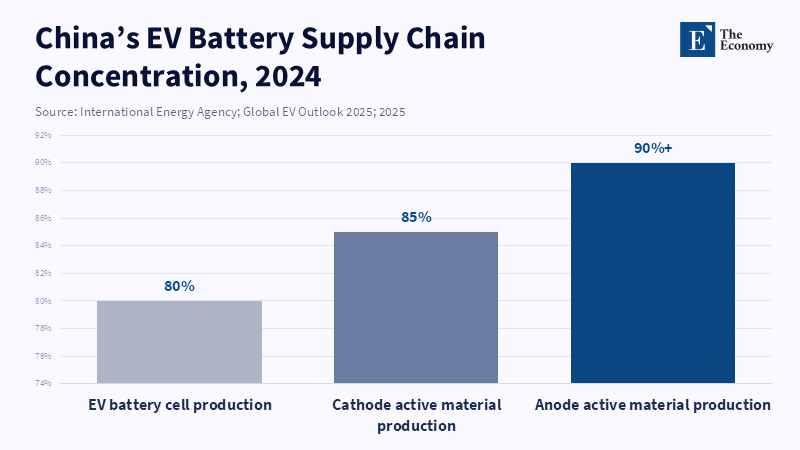

The market for electric cars is illustrative of the problems at hand. Global sales exceeded 17 million units in 2024, with over 11 million being sold in China. By 2024, nearly 50 percent of cars sold in China were electric. China produces around 80 percent of global EV battery cells, almost 85 percent of cathode active material and more than 90 percent of anode active material. This is not just an environmental development but also an opportunity for setting global standards. If electric vehicles are to become the standard global car, then battery technology, software and charging infrastructure will shape the auto industry for years to come. European, Japanese, Korean and US policymakers are not concerned about whether the Chinese make good products, but about whether China dictates the entire world of product development.

The recent surge in tariffs is a response to this concern. In 2024, the US increased tariffs on Chinese EVs to 100 percent. Meanwhile, the EU slapped countervailing duties on Chinese EVs with rates that range from 35.3 percent, in addition to standard duties. Such measures are often labeled protectionism, some more so than others, but they signal the advanced economies' perception of clean technology no longer as a commodity, but a platform war. The question is not if there will be trade, but if trade has enough substance to maintain peace.

AI Hardware: The New Peace Dividend Sector

The realm of EVs demonstrates where China has built considerable scale. The US, however, still enjoys a relative edge in AI Hardware, a sector that forms the nexus of the strategic peace dividend. Semiconductors, cloud systems, electricity grids and computing infrastructure are all vital in this domain. US-headquartered semiconductor firms commanded slightly more than half of global chip sales in 2024. NVIDIA's revenue in 2025 was $130.5 billion, fueled by data center demand. These numbers reflect shifts in bargaining power.

The AI boom fundamentally alters our understanding of security. By 2030, data center electricity consumption is expected to rise by over 100% to approximately 945 TWh, driven largely by AI workloads. That’s nearly as much power as Japan consumes in a year. A nation that leads in AI chips, cloud services, electrical grids and applications does more than export products; it establishes dominance over the underlying logic of intelligence. That’s far more potent than tariffs. It determines who has access to the resources for model training, automation, design, modeling, operational management and next-generation services.

Peace through strength today requires more than just military force, which can be costly and fragile. Strength today signifies a sufficient measure of control over critical technologies, preventing adversaries from acting rashly. It also enables allies to find a dependable partner beyond a single dominant manufacturing structure. To achieve a US-aligned strategic peace dividend, the United States must build on its existing advantages and invest in areas like AI hardware. Advanced semiconductors, grid technology, defense electronics, quantum devices and high-level industrial software are all candidates for such investment.

The most obvious geopolitical risk is that such a strategy could partition the world into competing blocs and make war more likely. That is a real risk; a crudely implemented decoupling strategy is more likely to increase mistrust, increase costs and decrease the same linkages that reduce conflict. However, the alternatives-unchecked openness and separation- are not viable. The correct path involves selective interdependencies, by keeping trade open where risk is low, developing redundancy where coercion is a likelihood, sharing critical production with trusted friends and using tariffs only in those instances where subsidy and strategic dependence are already creating long-term damage. Such a strategy is not isolationism; it is insurance.

Resilience Without Retreat

The test of the policy should be the following: can we achieve security without retreat? The goal should not be free trade or separation, but rather security without sacrifice; the government should ask before it reduces or increases trade barriers, whether it would still appear secure after such a change in a crisis. If the answer is no, then the policy needs reformulation.

For EVs, supply chain resilience means domestic battery capacity, processing, recycling industries and standards. For AI, this requires domestic manufacturing of silicon, packaging, power generation, transformers and cooling systems, as well as skilled workers, along with export controls that would limit the export of critical technologies that could be used for military purposes without hampering civilian use.

For allies, this suggests that purchase rules should prioritize trade with trusted suppliers over mere low prices. Industrial policy is not a dirty word; all major governments currently practice it, so the task is to do it intelligently. Good industrial policy supports rather than stifles all industries. It ensures the existence of a sufficient number of firms so that a nation can negotiate, adapt and recover. It provides incentives for private investors to construct industries with high social value even if immediate returns are not guaranteed. The market has no mechanism to capture the loss of a battery, chip, tool, or power grid supply chain until it is already lost.

There is, therefore, a careful trade-off required in developing a strategic peace dividend. The global community should remain open to trade in order to impose costs on aggression, but it should protect itself from dependence being used as a weapon. Commerce still cools politics, as the conventional wisdom would have it, but that statement is now incomplete. Commerce cools politics when it is based on trust, diversification and credible power. When the flow of trade is used to achieve dominance over others, commerce hardens politics. In a world that already spends about 2.9 trillion dollars annually on defense, peace will not spontaneously be generated by markets; it must be manufactured with domestic industrial power, allied cooperation, and careful trade policy. Peace in the coming decade will go to the nations that understand that openness is not antithetical to power; it is safest when backed by power.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

European Commission (2024) ‘EU imposes duties on unfairly subsidised electric vehicles from China while discussions on price undertakings continue’, European Commission Press Release, 29 October.

Feng, L., Huang, Q., Li, Z. and Meissner, C.M. (2026) ‘Why “de-risking” may not deliver a large peace dividend’, VoxEU, 8 May.

Innes, S. (2026) ‘Markets trade a peace dividend while AI builds a debt-fueled empire’, Investing.com, 7 May.

International Energy Agency (2025a) Energy and AI. Paris: International Energy Agency.

International Energy Agency (2025b) Global EV Outlook 2025. Paris: International Energy Agency.

Kant, I. (1795) Perpetual Peace: A Philosophical Sketch. Königsberg: Friedrich Nicolovius.

Liang, X., Tian, N., Lopes da Silva, D., Scarazzato, L., Karim, Z.A. and Guiberteau Ricard, J. (2026) Trends in World Military Expenditure, 2025. Stockholm: Stockholm International Peace Research Institute.

Martin, P., Mayer, T. and Thoenig, M. (2008) ‘Make trade not war?’, Review of Economic Studies, 75(3), pp. 865–900.

Mayer, T., Méjean, I. and Thoenig, M. (2025) ‘The fragmentation paradox: de-risking trade and global safety’, CEPR Discussion Paper No. 20564. London: Centre for Economic Policy Research.

NVIDIA Corporation (2025) ‘NVIDIA announces financial results for fourth quarter and fiscal 2025’, NVIDIA Newsroom, 26 February.

Oneal, J.R. and Russett, B. (1999) ‘Assessing the liberal peace with alternative specifications: trade still reduces conflict’, Journal of Peace Research, 36(4), pp. 423–442.

Polachek, S.W. (1980) ‘Conflict and trade’, Journal of Conflict Resolution, 24(1), pp. 55–78.

Semiconductor Industry Association (2025) 2025 SIA Factbook. Washington, DC: Semiconductor Industry Association.

Thorne, J. (2026) ‘If Trump’s strategy of peace through strength works, the result could be a new peace dividend’, Wellington-Altus Private Wealth, 5 May.

UNCTAD (2025) Global Trade Update: The Role of Tariffs in Global Trade. Geneva: United Nations Trade and Development.

United States Trade Representative (2024) ‘U.S. Trade Representative Katherine Tai to take further action on China tariffs after releasing statutory four-year review’, Office of the United States Trade Representative Press Release, 14 May.

United States Trade Representative (2026) The People’s Republic of China: Trade Profile. Washington, DC: Office of the United States Trade Representative.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.