Partial Relief From Deflationary Pressures Amid Iran War, Yet Export Reliance and Defense Spending Risks Persist

Authored On

Modified

Long-Entrenched Deflation Gives Way to Price Rebound Triggered by Iran Conflict Beijing’s Advanced Manufacturing Push Shows Limited Effect on Domestic Consumption Defense Spending Continues to Climb as Consumption Recovery Measures Lose Momentum

The Chinese government is intensifying its drive to foster advanced manufacturing industries. As prolonged deflation deepens economic strains, Beijing has moved to secure new growth engines through massive investment in strategic sectors. Market observers, however, largely argue that the impact of these policies remains confined to export markets and has failed to generate meaningful spillover effects across the broader domestic economy. China’s vast military expenditures are also increasingly viewed as a structural impediment to domestic demand recovery.

Shifting Dynamics in China’s Inflation Trend

According to financial industry sources on the 13th, China’s economy has endured severe domestic demand weakness and persistent deflationary pressures for several years. Data from the National Bureau of Statistics (NBS) show that China’s Producer Price Index (PPI) remained in negative territory for 40 consecutive months from October 2022 through February of this year. China’s Consumer Price Index (CPI) likewise remained trapped in a near-zero inflation environment, posting annual growth of just 0.2% in 2023 and failing to stage any meaningful rebound through last year.

The situation began to shift in March this year, when the conflict involving the United States, Israel, and Iran escalated into open warfare. In March, China’s CPI rose 1% year-on-year while PPI increased 0.5%, signaling the possibility of a turning point. The trend became far more pronounced last month. China’s PPI surged 2.8% from a year earlier, sharply exceeding market forecasts of 1.53%, while CPI climbed 1.2%, also surpassing expectations of 0.95%. The escalation of Middle East tensions has pushed global energy prices sharply higher, fueling visible inflationary pressure. International crude oil prices have hovered around $100 per barrel since the outbreak of the Iran conflict.

Some analysts believe the inflation rebound could provide a favorable tailwind for China’s economy. Bloomberg reported last month that rising energy prices stemming from the Iran war were easing China’s deflation burden. Others, however, argue that the current price movements will provide little meaningful support to the broader economy. The South China Morning Post (SCMP) warned that inflation driven by wartime cost increases could prove more damaging to corporations than inflation fueled by rising demand. While headline inflation indicators may improve, analysts caution that stress across the real economy could intensify further.

Structural Weaknesses in China’s State-Led Growth Model

Amid such uncertainty, the Chinese government has selected advanced manufacturing expansion as its primary tool for overcoming the economic downturn. According to the OECD’s Main Science and Technology Indicators (MSTI) released in March, China’s research and development (R&D) spending reached approximately $1.03 trillion in purchasing power parity (PPP) terms in 2024, surpassing the United States’ $1.01 trillion for the first time. The surge reflects a rapid expansion of state-led investment across strategic industries including semiconductors, artificial intelligence (AI), electric vehicles, and batteries.

Government investment trends across industries clearly underscore this policy direction. In semiconductors, Beijing established the third phase of the National Integrated Circuit Industry Investment Fund, commonly known as “Big Fund III,” with a scale of roughly $47 billion in 2024. Massive capital is also flowing into AI infrastructure. Citing a Bank of America report, SCMP estimated China’s AI-related equipment investment last year at between approximately $82 billion and $96 billion, including around $56 billion in direct government funding. Support for the electric vehicle sector has been even more substantial. According to analysis by the Center for Strategic and International Studies (CSIS), the Chinese government injected at least approximately $231 billion into the EV industry between 2009 and 2023.

The problem is that Beijing’s state-led growth strategy has failed to translate into meaningful domestic demand expansion. China’s domestic market has struggled to absorb the rapidly growing supply generated through government-backed industrial expansion, forcing corporations to divert excess inventory into overseas markets. Even advanced industries are increasingly demonstrating stronger competitiveness in exports than in domestic consumption. This explains why Beijing’s aggressive investment campaign has failed to generate a sustainable cycle of job creation and consumer spending growth.

The “excessive competition” triggered by aggressive government support has also emerged as a major side effect. Chinese firms, backed by subsidies and policy financing, have continued flooding markets with supply far beyond underlying demand. Intensifying competition has fueled relentless price cuts, creating a vicious cycle in which shipment volumes and exports expand while corporate profitability remains stagnant. Without sustainable profit generation, meaningful trickle-down effects remain severely constrained. China’s economy has consequently become increasingly dependent on what analysts describe as “growth without domestic demand,” where production and exports continue rising even as consumption recovery remains weak.

Defense Spending Adds Further Pressure on Domestic Demand

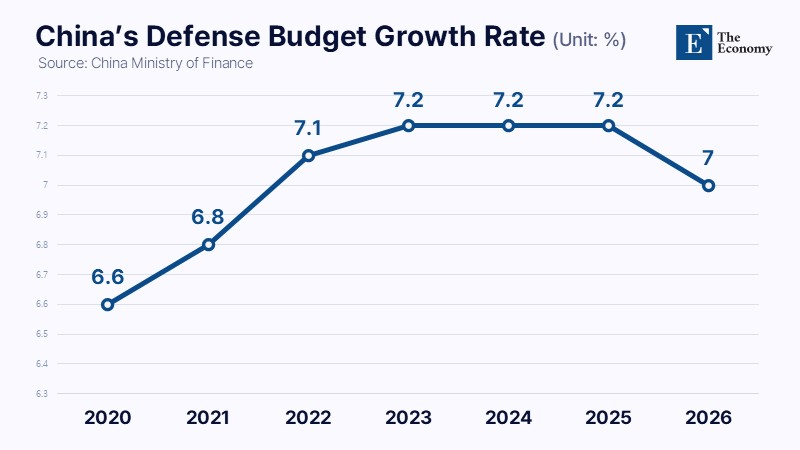

China’s enormous military expenditures are also increasingly cited as a factor aggravating domestic demand weakness. During the early years of President Xi Jinping’s administration from 2012 to 2015, China’s defense budget growth ranged between 10.1% and 12.2%. Growth later stabilized around the 7% level, recording 7.6% in 2016, 7.0% in 2017, 8.1% in 2018, and 7.5% in 2019. Although the increase temporarily slowed to 6.6% in 2020, spending growth accelerated again after Beijing unveiled its “military centennial” modernization objective in October 2020. Defense budget growth subsequently reached 6.8% in 2021, 7.1% in 2022, and 7.2% annually from 2023 through 2025. This year’s defense budget was set at approximately $262 billion, marking a 7.0% increase from the previous year.

Experts, however, argue that official figures fail to fully capture the true scale of China’s military spending. Off-budget expenditures such as R&D, overseas weapons procurement, and military pensions are excluded from official calculations, while funding for paramilitary organizations including the People’s Armed Police and coast guard forces is also omitted. China’s comparatively low labor costs further complicate accurate comparisons. Major institutions therefore present widely differing estimates. Although Beijing officially reported a 2024 defense budget of approximately $235 billion, the U.S. Senate estimated actual military spending at roughly $700 billion. The International Institute for Strategic Studies estimated China’s defense expenditures at around $330 billion during the same period, while the Stockholm International Peace Research Institute (SIPRI) projected approximately $318 billion. The American Enterprise Institute (AEI) has argued that China’s actual military spending is nearly three times higher than official disclosures and may have already approached U.S. defense spending levels by 2022.

The broader concern is that rising security-related expenditures are crowding out fiscal capacity for domestic consumption stimulus and economic recovery measures. Beijing has recently introduced policies such as consumption vouchers and appliance subsidies, yet it continues to avoid direct cash transfers or large-scale welfare expansion. The government remains focused on preserving fiscal stability and industrial competitiveness while distancing itself from U.S.-style large-scale consumption stimulus programs. In a recent report, the International Monetary Fund (IMF) warned that China’s economy remains excessively tilted toward exports and manufacturing investment, arguing that Beijing should pursue a transition toward consumption-driven growth through stronger social safety nets and structural shifts in fiscal spending priorities.

Similar Post