“Litigation Risk Cleared”: OpenAI Accelerates IPO Preparations, Though Profitability Concerns and Intensifying Competition Remain Key Variables

As one of the youngest members of the team, Tyler Hansbrough is a rising star in financial journalism. His fresh perspective and analytical approach bring a modern edge to business reporting. Whether he’s covering stock market trends or dissecting corporate earnings, his sharp insights resonate with the new generation of investors.

Authored On

Modified

OpenAI Moves Aggressively Toward IPO After Concluding Court Battle With Musk Growth Momentum Fails to Match Massive Investment Scale as AI Bubble Debate Persists Competitive Positioning War Across Global AI Industry Intensifies From Anthropic and Google to China

OpenAI, the developer of ChatGPT, is accelerating its push toward an initial public offering (IPO). The company recently secured a major legal victory in a lawsuit brought by Tesla CEO Elon Musk, removing a significant overhang and strengthening momentum for large-scale capital raising. Even so, market participants argue that it remains too early to conclude that the IPO will be a success, citing variables such as enormous artificial intelligence (AI) infrastructure spending and increasingly fierce market competition.

OpenAI Secures IPO Momentum Through Court Victory

On May 20, The Wall Street Journal (WSJ), citing multiple sources, reported that OpenAI has recently been preparing its prospectus in coordination with banks and plans to confidentially submit the filing to the U.S. Securities and Exchange Commission (SEC) as early as May 22. The company is reportedly targeting September for the listing, though the timeline remains subject to change. OpenAI’s current valuation is estimated at approximately $852 billion, while its target valuation reportedly exceeds $1 trillion.

Market observers point to the legal battle with Musk as a key catalyst behind OpenAI’s renewed IPO drive. The court recently ruled in OpenAI’s favor. Musk had previously argued that OpenAI CEO Sam Altman abandoned the company’s founding mission of conducting “AI research for the public good” by transforming OpenAI into a profit-oriented entity, thereby undermining the purpose of the roughly $38 million in seed funding Musk contributed during the company’s founding in 2015. OpenAI countered that Musk left the company after failing to secure full control and later filed the lawsuit to restrain a competitor after establishing his own AI venture, xAI.

On May 18, the Oakland division of the U.S. District Court for the Northern District of California dismissed Musk’s lawsuit following a trial that lasted roughly three weeks after opening arguments began on April 27. The jury unanimously sided with OpenAI after less than two hours of deliberation. The central basis for the verdict was that Musk had exceeded the statute of limitations for filing the lawsuit. Judge Yvonne Gonzalez Rogers stated that “substantial evidence supported the jury’s conclusion.” Although Musk’s legal team has said it cannot accept the ruling, the likelihood of overturning the decision appears low given that the statute-of-limitations issue falls largely within the realm of factual determination.

Persistent Concerns Over Profitability

Despite the legal victory, the prevailing view across Wall Street is that uncertainty surrounding OpenAI has not been fully resolved. Concerns remain over the company’s massive AI infrastructure spending and long-term profitability. OpenAI’s AI infrastructure expenditures have recently ballooned to levels comparable with those of global big tech firms. OpenAI co-founder Greg Brockman testified in court that the company’s computing-related spending this year is expected to reach approximately $50 billion. Such spending levels are unprecedented for a standalone AI company.

The company is also committing enormous sums to long-term cloud agreements aimed at securing computing capacity. OpenAI plans to spend a total of $300 billion on its cloud contract with Oracle between 2027 and 2031, equivalent to roughly $60 billion annually. Oracle is reportedly securing hundreds of thousands of Nvidia GB200 graphics processing units (GPUs) to build AI clusters for OpenAI, with related hardware investments alone estimated at around $40 billion. In addition, OpenAI signed a separate $38 billion cloud and GPU supply agreement with Amazon Web Services (AWS) last year.

The problem is that OpenAI’s top-line growth has failed to keep pace with the surge in investment costs. According to multiple media reports, OpenAI Chief Financial Officer Sarah Friar recently warned company executives that “if revenue does not grow quickly enough, we may not be able to pay for our computing contracts.” The concern appears rooted in weaker-than-expected results last year. OpenAI reportedly failed to meet its internally established targets for ChatGPT weekly active users, which had been set at 1 billion users, as well as its annual revenue targets. With concerns over excessive valuations across the broader AI industry still unresolved, these developments could weigh heavily on future investor sentiment.

Global AI Competition Intensifies Further

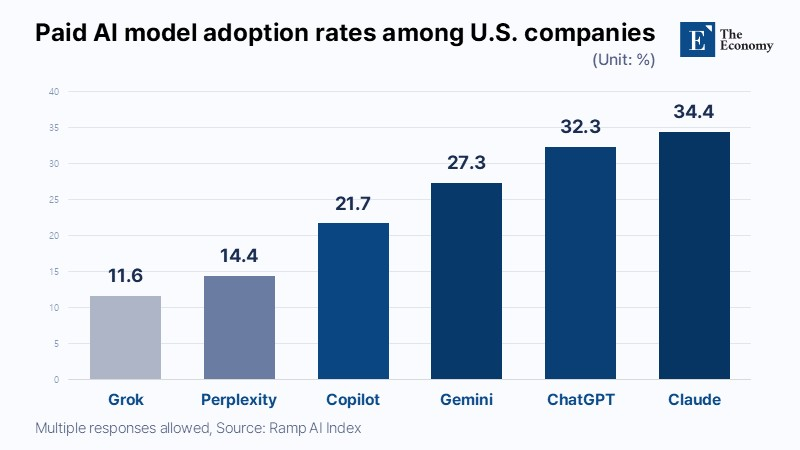

Fierce market competition is also viewed as a major obstacle to a successful IPO. At present, Anthropic is widely regarded as OpenAI’s primary rival. While OpenAI aggressively targeted the consumer market through ChatGPT, Anthropic rapidly expanded its presence in enterprise AI. Demand for Anthropic’s Claude model has surged particularly in sectors such as finance, legal services, and coding, where reliability and long-context processing capabilities are critical. According to an analysis conducted by U.S. fintech firm Ramp using corporate card and spending data from roughly 50,000 American companies, 34.4% of U.S. firms adopting paid AI services last month selected Claude, slightly surpassing ChatGPT at 32.3%.

Anthropic is also demonstrating stronger profitability metrics. According to a WSJ report published on May 20, Anthropic recently told investors that its second-quarter revenue is projected to reach approximately $10.9 billion, more than double its first-quarter revenue of $4.8 billion. Operating profit for the same period is projected at roughly $559 million. The growth was attributed to the rising influence of its AI coding tool Claude Code and ongoing efforts to improve infrastructure efficiency. Anthropic explained that while it spent 71 cents on computing costs for every dollar of revenue in the first quarter, that figure is expected to decline to 56 cents in the second quarter.

Google also remains one of OpenAI’s most formidable competitors. The company has leveraged its existing ecosystem spanning Search, Android, YouTube, and cloud services to build a large AI user base. Google is also viewed as having successfully vertically integrated major segments of the AI ecosystem, including proprietary AI semiconductors (TPUs), data centers, and search data. Its recently unveiled next-generation model, Gemini 3.5 Flash, drew market attention for significantly lowering token costs through TPU utilization and lightweight architectural design. Google stated that Gemini 3.5 Flash outperformed its previous flagship model, Gemini 3.1 Pro, in areas such as AI agents and coding, while delivering output speeds four times faster than competitors at half or even one-third of the cost.

Low-cost AI models emerging from China are also intensifying competitive pressure. DeepSeek’s next-generation V4 Preview model, unveiled last month, reportedly demonstrated performance comparable to the latest flagship models from major big tech firms across coding, agent capabilities, and knowledge benchmarks. Other Chinese technology companies, including Moonshot, Xiaomi, and Zhipu, have also launched models with similar performance levels in recent months. As the performance of low-cost AI models continues to improve, corporate AI deployment strategies are gradually shifting. Companies are increasingly adopting a so-called “advisor model” approach, using inexpensive open-source models by default while assigning only unresolved or highly complex tasks to frontier models developed by OpenAI or Anthropic.

As one of the youngest members of the team, Tyler Hansbrough is a rising star in financial journalism. His fresh perspective and analytical approach bring a modern edge to business reporting. Whether he’s covering stock market trends or dissecting corporate earnings, his sharp insights resonate with the new generation of investors.

Similar Post