“Middle East Shockwaves Ripple Through Markets” China and Japan Dump U.S. Treasuries as Surging Long-Term Yields Intensify Pressure on Warsh Fed to Turn Hawkish

As one of the youngest members of the team, Tyler Hansbrough is a rising star in financial journalism. His fresh perspective and analytical approach bring a modern edge to business reporting. Whether he’s covering stock market trends or dissecting corporate earnings, his sharp insights resonate with the new generation of investors.

Authored On

Modified

China and Japan unload massive volumes of U.S. Treasuries amid Middle East-driven market turmoil Sharp rise in long-term Treasury yields delivers a severe blow to financial markets Kevin Warsh, once an advocate of monetary easing, now faces mounting pressure for a policy pivot

China and Japan have aggressively sold U.S. Treasury holdings. As prolonged Middle East instability intensifies currency pressures across major Asian economies, both countries have moved to liquidate dollar-denominated assets in an effort to defend their currencies and diversify foreign-exchange reserves. The development is expected to add further upward pressure to already rapidly rising long-term U.S. Treasury yields. Analysts argue that Kevin Warsh, the incoming Federal Reserve chair, may need to abandon his previously dovish stance and adopt a more hawkish posture to stabilize mounting volatility in the bond market.

China and Japan Accelerate Treasury Liquidation

According to CNBC, citing U.S. Treasury Department data on the 19th local time, China’s U.S. Treasury holdings in March fell roughly 6% month-over-month to $652.3 billion, the lowest level since September 2008. During the same period, Japan—the largest foreign holder of U.S. debt—also sold approximately $47 billion in Treasuries, reducing its holdings to $1.191 trillion. Total foreign ownership of U.S. Treasuries consequently declined from $9.49 trillion in February to $9.25 trillion in March.

CNBC reported that the selloff emerged as international crude prices surged and Asian currencies weakened sharply amid escalating Middle East tensions. The Strait of Hormuz, a critical shipping route through which roughly 20% of global oil flows transit, has remained effectively blocked since the United States and Israel launched preemptive strikes against Iran late in February. As a result, global oil prices have hovered near $100 per barrel for months. Major Asian economies heavily dependent on Middle Eastern crude imports, including Japan, have faced their most severe energy shock in decades, while widening current-account deficits have sharply intensified exchange-rate pressures. The Treasury liquidation is therefore being interpreted as a form of foreign-exchange market intervention aimed at currency stabilization.

China’s ongoing reserve diversification strategy is also viewed as a key driver behind the Treasury selloff. Data from China’s State Administration of Foreign Exchange show that between 2014 and 2018, roughly 60% of China’s foreign-exchange reserves consisted of dollar-denominated assets, a substantial portion of which was presumed to be invested in U.S. Treasuries. At the time, Treasuries were widely regarded as definitive safe-haven assets due to their deep liquidity and interest-bearing nature relative to gold. However, Beijing began restructuring its dollar-centric reserve portfolio in 2017, and accelerated Treasury liquidation following the freezing of Russian overseas assets after Moscow’s invasion of Ukraine in 2022. Massive U.S. debt levels and policy uncertainty have further undermined the appeal of dollar assets. Gold has increasingly filled the gap left by dollar-denominated holdings. The People’s Bank of China’s gold reserves stood at 74.64 million ounces last month, extending gains for an 18th consecutive month.

Financial Markets on Alert as Long-Term Yields Surge

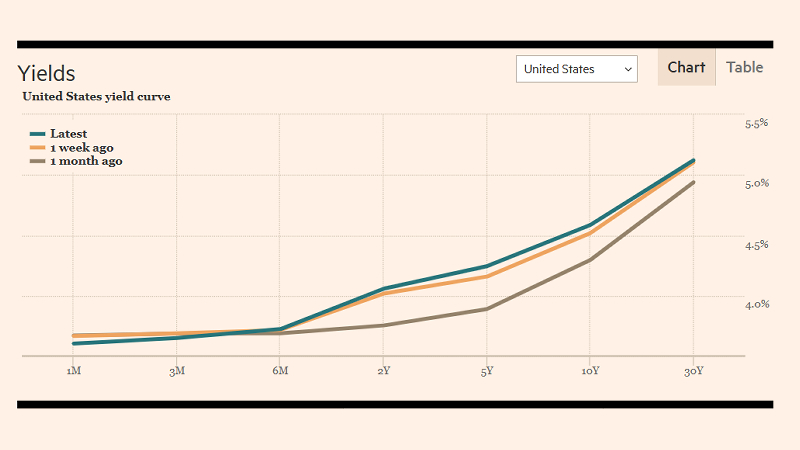

The sovereign-level liquidation trend is expected to exacerbate the recent surge in U.S. Treasury yields. On the 19th, the yield on the 30-year U.S. Treasury bond climbed 0.07 percentage points from the previous session to 5.19%, marking its highest level since the 2007 global financial crisis. The benchmark 10-year Treasury yield also rose to 4.67%, its highest reading since January of last year. As geopolitical risks stemming from the Middle East and persistently elevated oil prices intensified upward pressure on long-term rates, bond demand weakened sharply, triggering steep declines in bond prices. Bond prices and yields generally move inversely.

The situation is increasingly viewed as a severe threat to global financial markets that had previously been buoyed by enthusiasm surrounding artificial intelligence (AI). The U.S. 10-year Treasury yield effectively functions as the benchmark risk-free rate across global markets. Investors use Treasury yields as a near risk-free reference point under the assumption of enduring U.S. government stability. This dynamic explains why growth stocks tend to come under pressure during periods of rising Treasury yields. Valuations for sectors such as AI, semiconductors, and digital platforms depend heavily on future earnings expectations rather than current profits. As interest rates rise, the present value of those future cash flows declines sharply, increasing valuation pressure across high-growth sectors.

Shrinking system-wide liquidity presents an additional risk factor. Higher Treasury yields typically drive up deposit rates, corporate bond yields, and bank lending rates simultaneously. For corporations, financing costs for investment rise materially, while investors can secure meaningful returns without assuming excessive risk exposure. The result is a highly unfavorable backdrop for equities and other risk assets. Analysts warn that the threat may continue to intensify. According to Bank of America’s latest monthly global fund manager survey, nearly two-thirds of respondents expect the 30-year U.S. Treasury yield to exceed 6% within the next 12 months. Only 20% anticipated yields falling below 4%.

Will the Warsh Fed Deliver a Hawkish Signal?

Against this backdrop, market expectations are increasingly converging around the view that the Federal Reserve will maintain a prolonged pause in rate cuts. Persistent inflationary pressure and rising Treasury yields are constraining hopes for monetary easing. Prediction market platform Kalshi currently prices the probability of a Fed rate cut before 2027 at roughly 38%, down sharply from approximately 96% in February. CME FedWatch estimates a 98.8% probability that the Fed will hold rates unchanged through the end of June, while the probability of rates remaining unchanged through July also exceeds 94%.

Such market sentiment is poised to become a major burden for Warsh, who will assume office as the 17th chair of the Federal Reserve on the 22nd. Warsh has long argued that productivity gains driven by AI development could offset inflationary pressure and justify monetary easing. However, current market conditions offer little support for that position. Long-term Treasury yields continue to trend higher, while sentiment within the Fed itself increasingly suggests that rate cuts remain difficult in the near term. During last month’s Federal Open Market Committee (FOMC) meeting, policymakers reportedly displayed significant divisions over the possibility of additional tightening. Analysts warn that if Warsh delivers an excessively dovish message under current conditions, bond market volatility could accelerate substantially.

As a result, some corners of Wall Street are now arguing that Warsh must pivot quickly and deliver hawkish signals after taking office. Ed Yardeni, president and chief investment strategist at Yardeni Research, wrote in a recent client note that “the current market environment is no longer suitable for an easing bias, and the Fed should withdraw its dovish inclination at the June meeting.” He added that “if the Fed maintains an accommodative posture, investors will conclude that policymakers are falling behind the inflation curve and will demand a higher inflation risk premium.” Subadra Rajappa, head of U.S. rates strategy at Société Générale Americas, likewise told Bloomberg that “Treasury yields are approaching an unanchored state,” adding that “the Fed must shift from an easing bias toward neutrality and stand ready to act if necessary.”

As one of the youngest members of the team, Tyler Hansbrough is a rising star in financial journalism. His fresh perspective and analytical approach bring a modern edge to business reporting. Whether he’s covering stock market trends or dissecting corporate earnings, his sharp insights resonate with the new generation of investors.

- Previous “AI Calling the Shots and Making the Calls” — FIFA Turns the World Cup Into a Full-Scale Testbed for Sports AI After Years of Technological Buildout

- Next “$1 Billion in Annual Savings” Google Unveils Token-Cost Disruption Strategy, Targets Market Share Expansion as AI Industry Dynamics Shift

Similar Post