“From Bond Issuance to Private Equity Capital” Google Forms AI Cloud Venture With Blackstone as Funding Pressures Intensify

Authored On

Modified

Surging cloud demand drives sharp escalation in infrastructure investment burdens Blackstone to inject $5 billion and secure majority ownership stake Alphabet’s growing dependence on external capital underscores limits of internal funding capacity

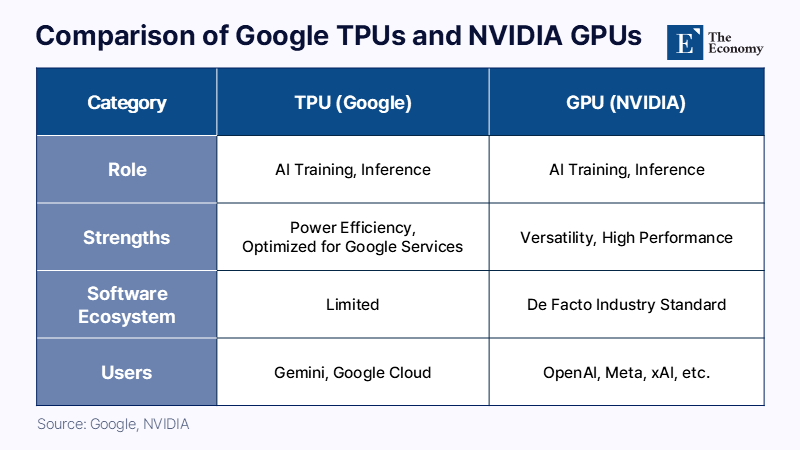

Google and Blackstone, the world’s largest private equity firm, are moving to establish a joint artificial intelligence (AI) cloud venture. As Google begins aggressively supplying its in-house AI chips — Tensor Processing Units (TPUs) — to external customers, the initiative is increasingly viewed as a direct challenge to Nvidia’s dominance over the AI infrastructure market. At the same time, analysts argue the partnership also exposes mounting financial strain inside Google, which has now reached the point of drawing in private equity capital to sustain its enormous AI data center spending commitments. Alphabet has already pursued large-scale fundraising efforts, including the issuance of 100-year bonds and yen-denominated debt. Since the emergence of generative AI, competition to expand data centers, AI servers, and cloud infrastructure has intensified so rapidly that internal cash flow alone is increasingly viewed as insufficient to sustain the pace of infrastructure expansion.

Blackstone Secures Majority Control of Google Joint Venture

On May 19 local time, The Wall Street Journal reported that Google and Blackstone plan to jointly establish an AI cloud company in the United States. Blackstone is expected to invest $5 billion in initial capital and secure the position of largest shareholder in the venture. Google will contribute its proprietary TPU AI semiconductors and related software stack. Benjamin Treynor Sloss, a longtime leader of Google’s site reliability engineering (SRE) division, has reportedly been selected as chief executive officer of the joint entity.

The venture is expected to emerge as a direct competitor to CoreWeave, which currently dominates the AI cloud market. CoreWeave supplies computing infrastructure to major AI developers including OpenAI and Anthropic using Nvidia-based chips. The Google-Blackstone alliance aims to disrupt that market using TPUs as its primary weapon. Its target is to secure 500 megawatts of AI data center power capacity by 2027. That level roughly matches the electricity consumption of a mid-sized city housing hundreds of thousands of residents, with plans for further phased expansion to support rapidly growing AI computing demand.

At the center of the venture lies Google’s broader commercialization push for TPUs. Google originally developed TPUs as specialized AI semiconductors primarily used internally for services such as Search, YouTube, and Gemini. Through this venture, however, Google is building a framework to supply them directly to outside AI companies at scale. Google has recently signed TPU supply agreements with major AI firms including Anthropic, developer of Claude, and Meta, the parent company of Facebook. Market observers note that the Blackstone partnership carries broader significance because it extends beyond TPU supply into the joint construction of large-scale AI data centers and cloud infrastructure.

The current AI cloud market remains dominated by Nvidia GPU-based operators. Major AI companies including OpenAI and Anthropic largely procure computing capacity through Nvidia-powered AI cloud providers. However, since the generative AI boom began, worsening GPU shortages and rapidly escalating costs have accelerated demand for alternative chips. Google is now positioning TPUs as a means of reducing the market’s dependence on Nvidia. Blackstone, meanwhile, has also accelerated investment across AI infrastructure. Since 2021, the firm has acquired data center companies including QTS and AirTrunk while investing in key AI ecosystem players such as CoreWeave, Anthropic, and OpenAI.

Explosive Growth in Google Cloud Drives Full-Scale Infrastructure Investment War

Behind Google’s increasingly aggressive pursuit of external capital lies the simultaneous surge in its cloud business and the escalating burden of AI infrastructure investment. Alphabet’s cloud division has emerged as the company’s strongest growth engine amid expanding AI demand. In the first quarter of this year, Alphabet posted consolidated revenue of $109.9 billion, while Google Cloud revenue surged 63% year-over-year to $20 billion. Cloud backlog also expanded sharply from $240 billion in the previous quarter to $460 billion. Markets expect roughly half of that amount to convert into revenue within the next two years.

The problem is that demand growth is now outpacing infrastructure expansion capacity. Exploding demand for generative AI training and inference has turned access to data centers, electricity, servers, networking equipment, and AI accelerators into the defining constraint on cloud companies’ future growth ceilings. The result is a paradoxical structure in which rising cloud revenue simultaneously requires even larger upfront investment commitments. Generative AI services are also fundamentally more capital-intensive than traditional cloud businesses. Conventional cloud operations could previously accommodate demand largely through expansion of general-purpose server fleets. AI cloud infrastructure, however, requires tightly integrated deployments of GPU clusters and ultra-high-speed networking systems.

Although Google remains one of the few major technology companies possessing proprietary TPUs, chip design capabilities alone cannot resolve infrastructure bottlenecks. Actual service expansion requires vast data center land acquisitions, power procurement, cooling systems, server racks, long-term customer agreements, and enormous upfront capital expenditures. Google has already entered a phase where AI infrastructure spending pressures are escalating rapidly. During its latest earnings announcement, Alphabet raised its annual capital expenditure forecast to roughly $75 billion, explaining that a substantial portion would be directed toward AI servers and data center construction. That figure represents a multiple increase compared with just two years ago. Anthropic’s decision to expand usage of Google Cloud and TPUs while securing multi-gigawatt TPU capacity has further increased the burden on Google. In order to retain major AI research labs and enterprise customers, cloud operators must demonstrate access to actual deployable computing capacity.

Google Turns to PEF Capital Following Samurai Bonds Amid Escalating AI Investment Pressures

Those pressures are increasingly visible in Alphabet’s financing strategy as well. The company is preparing to issue yen-denominated bonds — widely known as Samurai bonds — for the first time in its history. While the exact issuance size has not been disclosed, the deal is expected to reach several billion dollars. The bonds will reportedly be structured as global yen-denominated debt targeting not only Japanese investors but also global institutional buyers. Bank of America, Mizuho, and Morgan Stanley are serving as lead underwriters and are currently gauging investor demand in the United States ahead of setting final issuance terms later this month.

Market participants view Alphabet’s decision to tap Japanese bond markets as a stark illustration of the scale of AI infrastructure financing pressures facing even the world’s largest technology companies. Earlier this month, Alphabet also issued $17 billion worth of euro-denominated bonds and Canadian dollar debt. The company explained that it aimed to reduce borrowing costs and diversify global funding channels by issuing large amounts of overseas debt carrying lower interest rates than dollar-denominated financing. Markets, however, interpret the move as evidence that internal cash flow alone is becoming insufficient to sustain expansion of data centers and the AI chip ecosystem.

Analysts broadly view Blackstone’s $5 billion equity investment as a continuation of that same trend. Google’s willingness to dilute ownership in order to accelerate cloud infrastructure expansion is increasingly seen as evidence that the AI investment race has begun exerting pressure across corporate financial strategy itself. Under conventional corporate financing hierarchies, internal cash reserves, bank borrowing, and bond issuance are generally utilized first, while equity financing remains the most burdensome option — a framework widely referred to in finance as the “Pecking Order” theory.

From a corporate perspective, cash depletion and debt financing impose relatively limited burdens because debt can eventually be repaid without diluting managerial control. Equity financing, however, carries fundamentally different implications. External investors secure ongoing participation rights in future profits and asset appreciation. Companies may face future dividend obligations, while strategic decision-making processes become increasingly shaped by outside stakeholders. Moreover, private equity capital from firms such as Blackstone is typically deployed with eventual exit strategies in mind, making it functionally closer to high-cost capital than long-term strategic investment. Nevertheless, Google’s decision to establish a joint venture backed by outside capital strongly suggests that the company can no longer sustain the pace of AI infrastructure expansion through internal funding capacity alone.

Similar Post