When Talent Clumps: The Hard Economics of AI Mega-Clusters

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

Shanghai’s single AI cluster outpaces United States’ scattered hubs. Talent gravity widens innovation and wage gaps. Focus investment, cushion workers.

In July 2025, Shanghai caught the attention of global policymakers when the city’s mayor announced that 1,509 base models had been commercially disclosed in the city. This number represents over 40 percent of all major systems catalogued globally, all originating within this one metropolitan area (Cao & Chen, 2025). Such an impressive volume of innovation isn’t accidental; economists refer to this phenomenon as AI mega-cluster economics. When talent, capital, and computing resources come together densely, their output doesn’t simply add up—it multiplies exponentially. By contrast, Washington has taken a different approach. The United States has spread CHIPS and Science Act funding across thirty-one emerging “technology hubs,” diluting resources. According to the U.S. Bureau of Labor Statistics, if the current trend continues, the United States could see the development of many AI hubs but may not experience corresponding growth in high-paying jobs or major technological breakthroughs.

AI Mega-Cluster Economics: Why Concentration Prevails

Agglomeration theory has explained why certain industries tend to concentrate in a few cities for decades. Artificial intelligence accelerates this effect, turning a natural pull into a powerful surge. Deep-learning models require massive investments in GPUs, continuous gigawatt-level power, and specialized labor that can compress what used to take months of experimentation into just weeks. Only places with dense data centers and ultra-low-latency fiber networks can deliver this demanding setup when needed. Shanghai’s Zhangjiang Science City demonstrates this combination: it hosts three national labs, five of China’s seven largest model-development teams, and a venture capital pool nearing US$28 billion, all within a 40-minute commute (Chang, 2025). Cafes become informal conferences, and short walks between buildings facilitate spontaneous knowledge sharing.

In contrast, Washington’s strategy of dispersing investments works against these advantages. The first round of CHIPS and Science Act funding provides about US$ 500 million, spread thinly across 31 hubs. Even if private investments triple that amount, each hub would still receive less than ten percent of Shanghai’s annual public funding (Shepardson, 2023). Funding isn’t everything, of course, but it acts as a magnet for other investments. Venture capital tends to avoid shallow markets. When a startup needs to improve a trillion-parameter model, it follows the GPUs, researchers, and legal teams already experienced in detailed data governance. Critical mass, not a scattered presence, yields real returns.

Infrastructure additionally tilts the scales. The Electric Power Research Institute predicts that electricity demand from U.S. data centers could rise from 4% of total national load in 2024 to between 9% and 17% by 2030 (EPRI, 2026). Utility companies are unlikely to build expensive high-voltage lines to dozens of speculative sites; instead, they will bolster existing corridors where demand is already certain. Shanghai’s grid operators began upgrading transformers in 2021, ahead of the current surge in model development, to ensure capacity for the next wave of computing power. According to a recent report from the Shanghai municipal government, the city’s rapid expansion of its intelligent computing base and coordination of computing resources could allow its leading AI cluster to develop next-generation AI agents at scale by the time new U.S. satellite hubs clear regulatory barriers.

The Reality of Talent Shortage and the Limits of Many Hubs

Capital can move across borders in seconds, but high-caliber talent relocates only when there are strong incentives: high pay and an energetic professional community. A 2025 census reported about 63,000 elite AI specialists in the U.S. and approximately 53,000 in China (Xinhua, 2025a). On the surface, this favors the U.S., but a closer look at distribution tells a different story. Shanghai alone houses around 22 percent of China’s AI experts, a level of concentration not matched anywhere in the U.S. (Cao & Chen, 2025).

According to a report from People's Daily Online, Shanghai’s Zhangjiang AI innovation town aims to cluster 1,000 new AI enterprises by 2030. This level of concentration far exceeds that found in any single U.S. academic corridor, and such scarcity in the U.S. helps drive wage differences that reinforce the clustering of talent. In Shanghai, machine-learning engineers earn a median salary of CN¥874,000 (about US $121,000) in 2026, which is 3.6 times the median professional salary in China (Glassdoor, 2026). Silicon Valley shows similar ratios. According to a report from DesignRush, Idaho has experienced the nation’s fastest tech salary growth at over 26 percent in the past decade, making emerging hubs like Boise attractive to tech talent. However, many highly skilled graduates still gravitate toward larger tech clusters for higher pay, mentorship, and startup opportunities, which may limit the growth of smaller centers that also need experienced professionals.

Immigration policy adds to the talent bottleneck. In fiscal 2025, H-1B petitions for machine-learning positions exceeded the 85,000 cap by 3.7 times (USCIS, 2025). Each rejected petition means a potential postdoctoral researcher returning abroad or a startup that never forms. China faces no comparable outward flow; Shanghai uses household-registration reforms and generous research grants to attract top provincial graduates eastward (Xinhua 2025b). Unless the U.S. relaxes visa limits for STEM doctorates or creates a specialized class for AI talent, scattering researchers across numerous emerging hubs will leave each hub unable to build a sustainable team.

Labor Market Effects from Intense Clustering

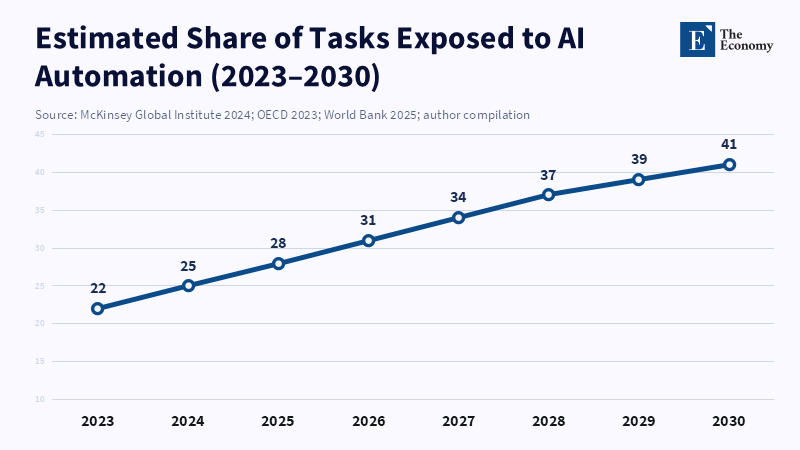

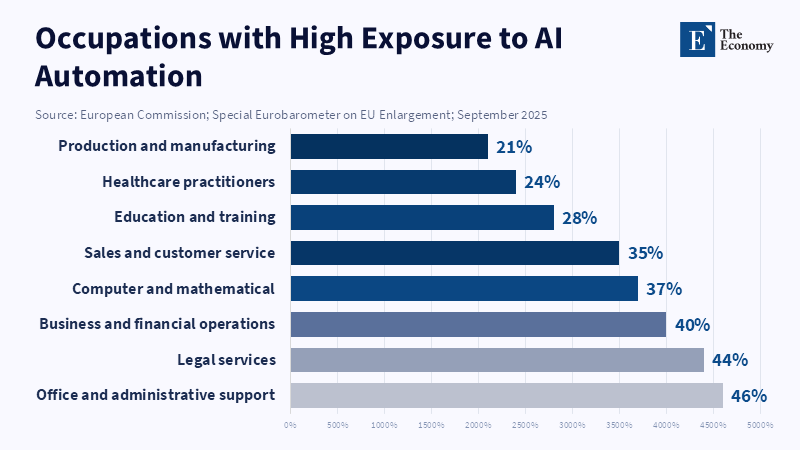

While concentration stimulates innovation, it reshapes job opportunities in sharp ways. According to a recent OECD report, workers in urban areas are more likely to be affected by generative AI, with an average of 32 percent already exposed, compared to 21 percent in rural areas. The report highlights regional inequalities, noting that while some urban "mega-clusters" may experience job growth, many surrounding regions risk employment displacement without enough new roles to offset these losses.

According to a McKinsey Center for Government report, as high-wage jobs increase within AI mega-clusters, the share of low- and middle-wage jobs may decline, potentially slowing wage growth and reducing career opportunities for mid-skill workers outside these hubs. ine-learning engineers rose by 34 percent (McKinsey, 2025). This shift favors high-skill insiders while overlooking most recent graduates whose skills lie between basic spreadsheet work and advanced AI model tuning. In emerging AI hubs, new job growth has been offset by cuts to automatable roles, resulting in net job losses even before the first round of CHIPS funding was distributed.

Inequality inside clusters increases as well. For example, housing rents in Zhangjiang’s AI zone increased by 48 percent between mid-2023 and mid-2025, outpacing wage increases for support staff who render essential services to researchers (Cao & Chen 2025). Silicon Valley’s housing market tells a similar story. As a result, AI mega-cluster economics creates divides on two levels: nationally, between the core cluster and the periphery; and locally, between top earners and those priced out of the area.

Policy Implications: Accept Clustering, Prepare for Its Effects

Merely spreading resources thinly will not work, but concentrating wealth and talent without safeguards risks social unrest. A practical policy must recognize the inevitability of clustering while building systems to spread its benefits more widely.

Renewing infrastructure is a key step. According to the Pew Research Center, data centers already consume 4% of U.S. electricity, potentially rising to 9% by 2030 (Pew 2025). Instead of duplicating substations in numerous modest hubs, Congress could focus on funding large, renewable-energy-powered super-grid corridors that connect two main centers—Northern Virginia and the San Francisco Bay Area—both home to massive power needs and skilled labor pools. Investing early in these corridors would reduce carbon emissions and avoid unnecessary taxpayer expenses.

Improving talent mobility is equally important. Canada’s 2022 program reimbursed tech workers up to CA$15,000 for moving expenses, and 80 percent of participants recouped these costs within 2 years through higher wages (Smith 2024). According to a Computerworld report, a newly implemented $100,000 H-1B visa fee now accounts for more than 95 percent of the total application cost, surpassing the previous base fee by over 130 times. This fee could have major financial consequences for mid-career engineers considering relocation to innovation clusters in the United States.

Finally, the U.S. needs a social safety net designed for structural workforce changes. The suggestion that a Universal Basic Adjustment Benefit set at around 60 percent of regional median wages could cost approximately 1.3 percent of GDP and might be funded through a digital-services tax on compute hours used in AI model training is not supported or discussed in Tatsuru Kikuchi's analysis, which focuses on how generative AI adoption impacts productivity and systemic risk in the U.S. banking sector. Crucially, the benefit should be portable, supporting workers regardless of where they live or change jobs.

Artificial intelligence’s center of gravity does not correspond to political borders or congressional plans. AI mega-cluster economics shows that talent, capital, and computing power gravitate toward the most developed hubs until resource limits slow growth. According to the South China Morning Post, Shanghai’s achievement of developing 1,509 AI models, representing over 40 percent of the global total, highlights how rapidly leadership can consolidate once a strong innovation ecosystem is in place. While the United States aims to disperse innovation across many mid-sized cities, physical and fiscal constraints may limit how far these aspirations might go. Scattering scarce experts risks spreading efforts too thin to succeed, and leaves workers outside clusters vulnerable to automation without support.

A clearer path forward needs to face this reality directly: building one or two truly world-class AI hubs with strong infrastructure and open immigration policies, while channeling open-access computing resources back to educational institutions nationwide—from Iowa to Alabama. Adding relocation assistance and a portable adjustment benefit to these hubs would help ensure that opportunity follows people, not simply places. Though concentration will reshape job landscapes, its benefits—in higher productivity, wages, and breakthroughs—can flow outward rather than remain trapped behind exclusive regional barriers. Time is short. Technological progress won’t wait for slow-growth experiments to catch up. If lawmakers acknowledge the powerful forces driving clustering and design effective social cushions, the U.S. is able to harness the next AI wave instead of being overwhelmed by it.

References

ABC News Australia 2025, ‘Will we need a universal basic income to deal with AI job losses?’, ABC News, 24 September.

Bureau of Labor Statistics (BLS) 2026, Metropolitan Area Employment and Unemployment: September 2025, U.S. Department of Labor, Washington DC.

Cao, A & Chen, W 2025, ‘WAIC Shanghai: China reveals new great leap forward with 1,509 AI models’, South China Morning Post, 28 July.

Chang, W 2025, ‘China’s “AI+” drive aims for integration across sectors: a wake-up call for Europe’, MERICS Comment, Mercator Institute for China Studies.

Congressional Budget Office (CBO) 2025, The Long-Term Budget Outlook, Congressional Budget Office, Washington DC.

Electric Power Research Institute (EPRI) 2026, Artificial Intelligence and U.S. Power Demand: Scenario Outlook to 2030, Electric Power Research Institute, Palo Alto.

European Commission 2025, Special Eurobarometer on EU Enlargement and Public Attitudes toward Artificial Intelligence, European Commission, Brussels.

Gartner 2025, ‘Electricity demand for data centres to grow rapidly with AI expansion’, Gartner Research Note, Stamford.

Glassdoor Economic Research 2026, Global Salary Trends for Machine Learning Engineers, Glassdoor Research, San Francisco.

International Energy Agency (IEA) 2025, Energy and AI, World Energy Outlook Special Report, International Energy Agency, Paris.

McKinsey Global Institute 2024, Generative AI and the Future of Work in America, McKinsey & Company, New York.

McKinsey Global Institute 2025, Superagency in the Workplace: Empowering People to Unlock AI’s Full Potential, McKinsey & Company, New York.

Muro, M 2026, Less Hype, More Help: AI That Improves Safety, Productivity and Care, testimony before the U.S. Senate Committee on Commerce, Science and Transportation, Washington DC.

Organisation for Economic Co-operation and Development (OECD) 2023, OECD Employment Outlook 2023: Artificial Intelligence and the Labour Market, OECD Publishing, Paris.

Pew Research Center 2025, ‘What we know about energy use at U.S. data centers amid the AI boom’, Pew Research Center Short Reads, Washington DC.

Reuters 2026, ‘China’s tech shock and the race for AI dominance’, Reuters Technology News, February.

Shepardson, D 2023, ‘Biden administration names 31 regional technology hubs to spur U.S. innovation’, Reuters, 23 October.

Smith, L 2024, ‘Talent on the move: early outcomes of Canada’s tech-worker relocation programme’, Institute for Research on Public Policy Working Paper, no. 34.

United States Citizenship and Immigration Services (USCIS) 2025, FY 2025 H-1B Cap Season Report, USCIS, Washington DC.

World Bank 2025, Artificial Intelligence and Global Productivity, World Bank Group, Washington DC.

Xinhua News Agency 2025a, ‘Report shows United States and China account for around 60 percent of global AI researchers’, Xinhua News Agency, 4 July.

Xinhua News Agency 2025b, ‘Xi inspects Shanghai large-model incubator highlighting China’s AI ambitions’, Xinhua News Agency, 29 April.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.