Power Failure: America’s AI Energy Bottleneck and the Coming Productivity Divide

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

AI will not just augment workers; it will replace many with a few “superhuman” operators The real divide is access to compute and energy, not worker readiness Without new policy, AI will create structural labor redundancy

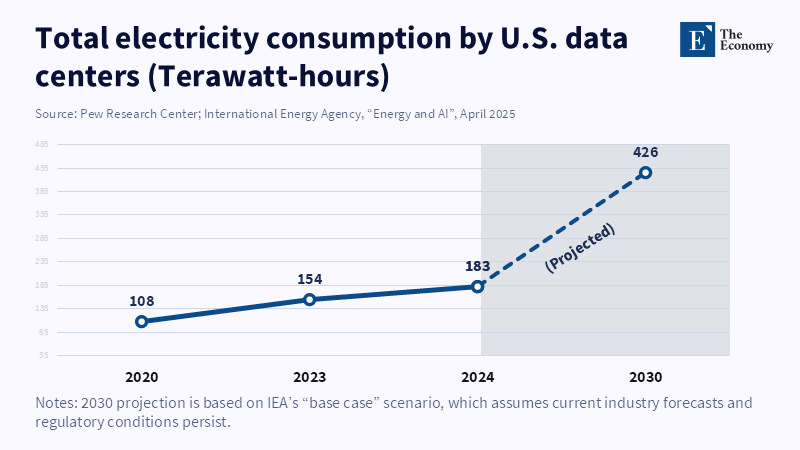

The artificial intelligence boom is often described as a race to build faster chips, larger models and more expansive data centres. Yet the most consequential constraint may not lie inside a server rack but far outside it—on the electric grid. Data centres consumed roughly 108 terawatt-hours of electricity in the United States in 2020. By 2024 that number had climbed to around 183 terawatt-hours, and mainstream projections suggest consumption could exceed 400 terawatt-hours by 2030. That trajectory represents one of the fastest expansions of industrial electricity demand in modern history. Policymakers typically interpret this jump as evidence of technological progress. But the trend reveals something more troubling: the American grid is approaching a structural limit that could limit the very AI growth policymakers hope to accelerate. The emerging AI energy bottleneck is therefore not simply a technical challenge. It is a labour-market challenge as well. When the electricity supply powering advanced computing becomes scarce or unreliable, the consequences extend well beyond data centres. They ripple across factories, offices and entire regional economies.

AI Energy Bottleneck and the Limits of the American Grid

Much of the policy conversation about artificial intelligence infrastructure focuses on data-centre construction. Legislators debate tax incentives for server campuses, zoning changes for technology corridors and subsidies for semiconductor fabrication. But the critical constraint is neither land nor buildings; it is electricity. The United States operates one of the largest electrical systems in the world, yet much of that infrastructure was designed decades before hyperscale computing existed. Many transmission lines date from the mid-twentieth century, and grid modernization has progressed far more slowly than digital innovation.

Artificial intelligence workloads create a type of electricity demand different from traditional industrial consumption. Training large models requires enormous bursts of power delivered with high reliability and minimal interruption. The International Energy Agency estimates that a single frontier-model training run can consume as much electricity as the annual energy use of thousands of households. When multiplied across dozens of data centres running continuously, these loads become comparable to the consumption of entire metropolitan areas. Unlike older industrial processes, AI clusters cannot simply pause operations during peak load periods. Interruptions may halt training operations or simultaneously disrupt cloud services relied upon by thousands of companies.

The challenge becomes clearer when examining the pace of growth in computing capacity. Artificial intelligence workloads have expanded at a rate far exceeding improvements in the electrical grid. Studies from energy researchers indicate that electricity demand from data centres could double or even triple by the end of this decade if AI deployment continues at current rates. Meanwhile, new high-voltage transmission lines often require years of regulatory approval and construction before they can deliver additional capacity. The mismatch between these two timelines creates a bottleneck that may become increasingly difficult to manage.

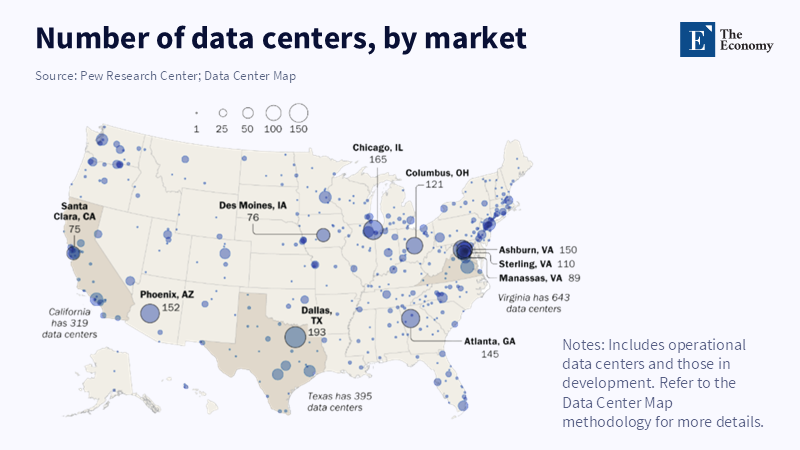

Transmission congestion already illustrates the problem. Several regions hosting major data-centre clusters—Northern Virginia, Phoenix and Dallas among them—have experienced rising electricity demand that strains local grids. Utilities have to respond by building additional generation capacity, upgrading substations and upgrading transmission corridors. Each of those projects requires considerable capital and a long planning horizon. Even when new capacity eventually arrives, it often does so years after demand has already surged.

The result is a fragile equilibrium in which hyperscale computing centres compete for power with residential users and traditional industries. When supply tightens, electricity prices rise. That dynamic affects not only technology companies but also manufacturing plants, hospitals and households connected to the same grid. The bottleneck, therefore, represents a wider economic issue rather than a narrow technological constraint.

Concentrated Infrastructure and the Geography of AI

Electricity demand alone does not explain the full scale of the emerging bottleneck. Geographic concentration plays an equally important role. Data-centre development in the United States has clustered heavily in a small number of regions where fibre connectivity, tax incentives and existing technology ecosystems already exist. Northern Virginia, for example, hosts the world’s largest concentration of data centres. Hundreds of facilities operate within a relatively small area, acting as the backbone of global cloud infrastructure.

This clustering generates powerful monetary advantages. Technology firms benefit from proximity to specialised labour, suppliers and network infrastructure. The concentration also creates a self-sustaining cycle in which additional investment gravitates toward rare assets already hosting large digital frameworks. Yet the same concentration magnifies the stress placed on local electricity networks. When dozens of hyperscale facilities draw power simultaneously, the demand can exceed what existing transmission lines were designed to deliver.

Utilities and regulators face difficult choices in such circumstances. They can approve new generation projects, expand transmission capacity or impose higher tariffs on heavy electricity users. Each option carries economic consequences. Expanding generation capacity requires investment that may ultimately be charged to consumers through higher electricity bills. Delaying upgrades risks service interruptions or reliability concerns that discourage future investment.

The concentration problem also reveals a strategic contrast with developments elsewhere in the world. China’s technology policy has increasingly integrated energy planning with digital infrastructure development. Large data-centre clusters have been paired with extensive funding in renewable energy and grid expansion. In rWithin areasrounding Shanghai, policymakers have pursued the deliberate construction of surplus electricity capacity to accommodate digital industry growth. Energy infrastructure is therefore treated as a core component of industrial strategy rather than an afterthought.

That approach contrasts with the more fragmented planning structure in the United States, in which energy policy is divided across federal agencies, state regulators and private utilities. While this decentralized model stimulates rivalry and creativity, it can also slow large-scale infrastructure expansion. Transmission projects often require coordination across multiple jurisdictions, each having its own regulatory framework. The resulting delays make it difficult for grid expansion to keep pace with the rapidly developing demands of artificial intelligence.

When Energy Security Becomes Labour Security

The consequences of the AI energy bottleneck go beyond technology firms and power utilities. They increasingly shape labour-market dynamics throughout the broader economy. Artificial intelligence promises enormous productivity gains, but those gains depend on reliable access to computing resources. When electricity constraints restrict computing availability, the distribution of economic benefits becomes uneven.

Regions with ample electricity capacity can host large clusters of AI infrastructure and the high-skill employment that accompanies them. Engineers, data scientists and system architects tend to concentrate near these hubs. Surrounding industries—from construction firms to equipment suppliers—also benefit from the economic activity generated by technology investment. The result is a reinforcing cycle of regional prosperity.

Regions with constrained electricity supply experience a different outcome. When grid capacity cannot support additional data-centre development, technology firms shift investment elsewhere. The regional workforce, therefore, misses out on the high-value employment opportunities linked with the AI economy. Over time, these disparities contribute to a widening productivity gap between energy-rich regions and those constrained by infrastructure limitations.

The labour implications reach even further. Artificial intelligence systems dramatically increase the productivity of individuals who deploy them effectively. In some cases, a single engineer furnished with advanced AI tools can perform tasks that previously required entire teams. If reliable computing resources are concentrated in a small number of geographic clusters, the economic power of those locations grows disproportionately. Workers located outside these clusters may find themselves excluded from the productivity gains that AI enables.

This phenomenon resembles earlier periods of industrial transformation. During the twentieth century, manufacturing centres flourished within regions having access to cheap electricity and transit networks. Communities lacking those advantages struggled to compete. The AI era may replicate this digital scale. Electricity infrastructure becomes the modern equivalent of railroads and ports: a prerequisite for participation in the dominant industries of the time.

If electricity supply cannot expand fast enough to support widespread AI deployment, the result may be what economists describe as structural labour redundancy. Productivity gains from AI systems could enable a relatively small number of workers to generate vastly greater economic output. Meanwhile, regions without adequate energy infrastructure would struggle to attract the investment necessary to create new employment opportunities. The technology, therefore, risks amplifying existing economic divides rather than reducing them.

Rewiring the Infrastructure of the AI Economy

Addressing the AI energy bottleneck requires more than incremental upgrades to existing infrastructure. The scale of projected electricity demand suggests that a comprehensive modernization of the grid may be necessary. Several policy avenues could be considered in such a fort.

First, expanding high-capacity transmission networks would allow electricity generated in resource-rich regions to reach areas where digiin which digitalcture is concentrated. Long-distance transmission corridors can connect renewable energy sources in the Midwest and Southwest to major technology hubs along the coasts. However, such projects require streamlined permitting processes and coordination across state boundaries. Without regulatory reforms, transmission expansion will continue to lag behind demand.

Second, investment in large-scale energy could help balance the changing demand patterns associated with artificial intelligence workloads. Battery storage systems allow excess electricity generated during periods of low demand to be stored and deployed during peak consumption. Such flexibility reduces the strain placed on generation capacity while improving grid stability.

Third, energy-efficiency standards for data centres may play an increasingly important role. Advances in cooling technologies, processor efficiency, and data-centre design can markedly reduce the amount of electricity required per unit of computation. Policymakers could encourage these improvements through incentives tied to energy efficiency indicators. These measures would not eliminate the demand surge created by artificial intelligence, but they could slow its growth enough for system improvements to catch up.

Finally, integrating energy planning with digital industrial policy would ensure that new AI infrastructure projects are matched by corresponding investments in power generation and transmission. This integrated approach mirrors strategies adopted by several technology-focused economies. Treating electricity infrastructure as a central component of AI competitiveness rather than a peripheral issue may prove essential for sustmaintaining long-termnomic growth.

Artificial intelligenceis frequently depicted ass a software revolution drivia algorithms and and data. In reality, it is equally a hardware revolution powered by electricity. The rapid rise in data-centre electricity demand—from just over one hundred terawatt-hours in 2020 to projections exceeding four hundred terawatt-hours by 2030—illustrates how quickly digital infrastructure can reshape national energy systems. If the United States fails to modernize its grid in response to this surge, the country risks confronting an AI energy bottleneck that constrains technological progress and deepens regional inequality.

The stakes go beyond maintaining technological leadership. Electricity infrastructure determines where the benefits of artificial intelligence will be realized and who will participate in the resulting productivity gains. Regions capable of supplying reliable, affordable power will attract investment, talent and innovation. Those who cannot may find themselves watching the next industrial revolution unfold elsewhere. Rewiring the grid, therefore, represents more than a technical challenge. It constitutes a strategic decision about the future geography of work, productivity and economic opportunity in the age of artificial intelligence.

References

Bureau of Labor Statistics (2024) Productivity and Costs by Industry: Manufacturing and Information Sectors. Washington, DC: U.S. Department of Labor.

Choubey, A. (2026) ‘US power demand surge from data centers could lift fossil fuel generation, EIA says’. Reuters.

Department of Energy (DOE) (2024) National Transmission Needs Study. Washington, DC: U.S. Department of Energy.

Electric Power Research Institute (EPRI) (2024) Powering Intelligence: Analyzing Artificial Intelligence and Data Center Energy Consumption. Palo Alto: Electric Power Research Institute.

Energy Information Administration (EIA) (2023) How much electricity is lost in electricity transmission and distribution in the United States? Washington, DC: U.S. Energy Information Administration.

Gartner (2025) Forecast: Data Center Power Demand Growth Driven by Artificial Intelligence. Stamford, CT: Gartner Research.

International Energy Agency (IEA) (2025) Energy and AI. Paris: International Energy Agency.

Leppert, R. (2025) ‘What we know about energy use at U.S. data centers amid the AI boom’. Washington, DC: Pew Research Center.

Marshall, C. (2026) ‘Data centers’ share of U.S. electricity seen doubling by 2030’. E&E News.

McKinsey Global Institute (2024) Artificial Intelligence and Energy Demand: Infrastructure Implications for the Global Digital Economy. New York: McKinsey & Company.

National Energy Administration (NEA) (2025) Special Action Plan for Large-Scale Development of New Energy Storage (2025–2027). Beijing: National Energy Administration.

Powell, L. (2025) ‘China’s Data Centres: Watts Behind the Bytes’. Observer Research Foundation.

Reuters (2026) ‘US Department of Energy to invest $1.9 billion in power grid upgrades’. Reuters.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.