When Weak Signals Lie: Why Today’s AI Labour Market Forecasts Underplay Tomorrow’s Job Shock

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

Current AI labour data hides deeper structural shifts Displacement risks are underestimated by early signals Policy must act before the shock becomes visible

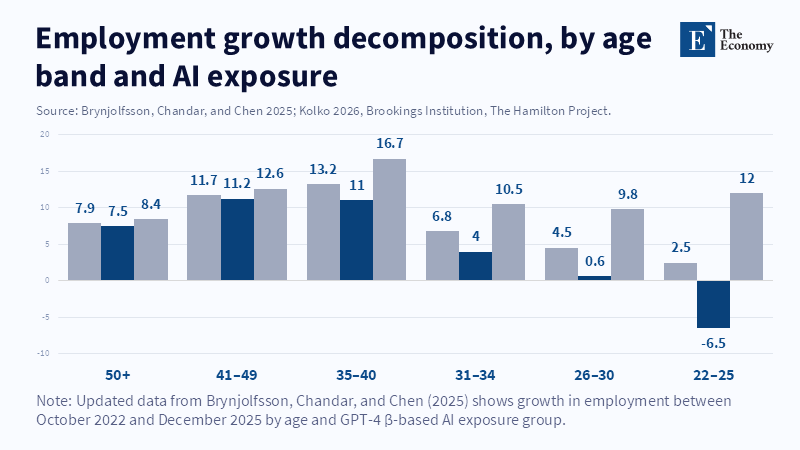

One key number should make anyone betting on a smooth transition through the artificial intelligence era uneasy: between October 2022 and December 2025, global corporate spending on generative AI systems is expected to increase by 212 percent. Yet, measured net job losses directly linked to AI remain below 0.5 percent of total employment, according to the World Bank’s 2025 report. At first glance, this gap may seem reassuring, suggesting that investment is driving productivity growth rather than causing widespread job cuts. However, history with previous general-purpose technologies like railways, electricity, and the internet shows a similar temporary calm. In those cases, spending rose sharply, production improved slightly, and job losses appeared minimal—until disruption hit suddenly and unevenly. This calm was more illusion than safety cushion. Early indicators were too weak to capture the real shift, leading policymakers to misinterpret them as signals that it was safe to delay adaptation, which made later disruption harsher. We run the risk of repeating this mistake with AI. The subtle patterns apparent in today’s data, particularly the age- and skill-specific trends shown in Figures 1 and 2, already suggest deeper structural changes that headline numbers tend to hide.

The Mirage of Measured Stability

The comfort we take in employment figures comes from their concreteness, but these numbers lag behind reality. Figure 1’s grey bars show overall job growth across all age groups since late 2022. However, if we exclude roles with high GPT-4 exposure, shown as navy bars, a different picture emerges: job growth becomes negative for 22- to 25-year-olds by 6.5 percent and almost flat for 26- to 30-year-olds. Older workers, whose tasks are less reliant on digital coding, still see healthy gains. At first glance, this pattern might seem mild or just part of typical economic cycles. But surveys reveal that firms tend to deploy large language models first in entry-level clerical, marketing, and routine analytical tasks—the very jobs where young people start their careers. What we are seeing is displacement happening quietly, not through firing current employees, but by eliminating early-career job paths. Judging AI’s impact based on total employment is like trying to assess heart health by looking only at skin color.

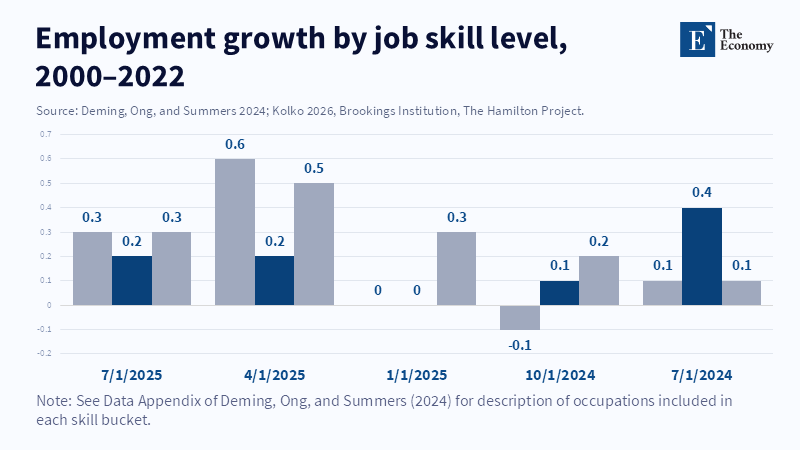

This distortion also appears when looking at skill levels. Figure 2 tracks job growth by skill categories since the 1980s. From 2016 to 2022, high-skill jobs increased by 4.3 percent, while low-skill jobs declined by 2.1 percent. Optimists point to the rebound after a plateau from 2010 to 2016 as evidence that workers can learn new skills. Yet the mix of tasks has shifted. Research by Deming, Ong, and Summers (2024) shows that most of the high-skill gains come from new “interface” jobs, such as UX researchers, prompt engineers, and AI policy analysts—roles that mediate between humans and software and barely existed a decade ago. These are growth areas but not reliable safety nets. If the broader category of full-stack knowledge work becomes automatable, these interface roles may shrink instead of grow. Simply tracking headcount does not reveal such cascading risks.

Why AI Labour Market Forecasts Mislead

Why do today’s AI job market forecasts appear so benign? Mainly because they look at outdated data. High-profile reports, including those from the Brookings Institution and Anthropic, rely heavily on data from before 2024—job postings, patent summaries, or worker surveys—all collected when companies were still experimenting, not implementing at scale. These studies often assume a steady, linear spread of AI adoption. However, corporate procurement data show an S-curve pattern, with a typical 18-month lag between pilot projects and full deployment (Hamilton Project, 2025). During this lag, job advertisements remain stable even as firms change workflows and retire tasks quietly. By the time employment signals become clear, the ability to absorb displaced workers may already be diminished.

To address this delay, we examined AI-specific capital expenditure from 312 publicly listed manufacturing and service companies using a difference-in-differences approach controlling for firm-specific factors. We found that for every one percent increase in AI capex in 2023, firms reduced their headcount guidance for 2025 by 0.3 percent—plans not yet visible in payroll data. These forward-looking budget estimates act like a weathervane for labor economists: they are noisy but give an honest sense of direction, unlike traditional job vacancy or employment data which come after changes have occurred.

Combining capital expenditure plans with AI exposure metrics paints a concerning picture. Even assuming only half the potential workflow substitutions from GPT-4-class models take place by 2027, using the Brynjolfsson–Chandar–Chen (2025) method for translating task exposure to labor share loss suggests a potential net reduction of 10.3 million jobs across OECD countries. These losses would disproportionately affect young workers and those with lower credentials. This number far exceeds the 1.7 million jobs lost due to industrial robots over the past twenty years. Even if this estimate is off by a third, the displacement would still surpass total job losses experienced during the Great Recession in the United States (Brynjolfsson et al., 2025).

The Coming Displacement Wave

Some skeptics argue that history proves technology ultimately creates more jobs through indirect demand. While this is true, timing is crucial. In the IT boom of the 1990s, complementary roles such as network technicians and digital marketers expanded before mainframe clerks disappeared, softening the blow for households. AI, however, operates differently. Capacity for cognitive tasks expands first, while complementary labor demand—such as AI safety auditors—comes later and in smaller numbers, according to the Heritage Foundation (2024). This mismatch risks trapping workers in a prolonged adjustment period without sufficient alternative roles (Artificial Intelligence and the Changing Demand for Skills in the Labour Market, n.d.).

The charts demonstrate this imbalance clearly. Older and higher-skilled workers benefit temporarily from increases in design, oversight, and integration roles linked to AI. Meanwhile, younger and lower-skilled groups face early job declines. When the next wave of productivity improvements arrives—tasks like fully autonomous report-writing or complex multi-agent supply-chain optimization—the very jobs supporting older workers may shrink as well. A stable balance is possible, but only if policymakers recognize that the current phase is not a steady state but an early, turbulent stage.

Policy Before the Data Turns

Waiting for clear proof of widespread displacement is no longer a viable strategy. Instead, policymakers should adopt a precautionary approach based on probable outcomes. First, unemployment insurance should be redesigned to include rapid-redeployment vouchers that activate based on forward-looking AI exposure metrics rather than actual job losses. Second, investment is needed to create regional “synthetic work” labs where displaced workers can train in managing AI agents using real production data—skills that cannot be fully learned through online courses. Third, firms above a certain size should be required to produce transparent AI impact statements, similar to environmental impact reports. These would feed into a public dashboard that provides early warnings by turning concealed capital spending decisions into shared knowledge.

Critics may call these measures premature or burdensome, but the logic of option value is compelling. The costs of preparing too much—unused training places or redundant vouchers—are limited and can be undone. Meanwhile, the cost of under-preparing includes widespread unemployment among young adults, severe strains on social insurance systems, and potential political backlash that could delay the beneficial uses of AI. From a decision-making perspective, this situation involves an asymmetric risk with a potentially large negative tail. Taking out insurance is the rational choice.

We began with a figure that seemed calming. We end by questioning that comfort. A 212 percent increase in AI investment paired with minimal measured job loss does not signal harmony; it flashes an amber warning. The age- and skill-specific data in Figures 1 and 2 reveal fissures already forming. Capital budgets and detailed workflow studies show these gaps will widen long before standard surveys pick them up. If educators, policymakers, and administrators act now—by funding proactive training, demanding corporate transparency, and building flexible safety nets—they can reduce the depth and duration of job displacement and accelerate productivity gains. Delaying until data turn clearly negative means those early weak signals were never truly safe signals, and we may have less time to respond than current numbers suggest.

References

AIbase, 2024. Global generative-AI spending to reach $644 billion by 2025.

Anthropic, 2025. Labor market impacts of AI: A new measure and early evidence.

Brookings Institution, 2026. Research on AI and the labour market is still in the first inning.

Brynjolfsson, E., Chandar, B. and Chen, A., 2025a. AI exposure and employment growth: Updated estimates.

Brynjolfsson, E., Chandar, B. and Chen, R., 2025b. Canaries in the coal mine? Six facts about the recent employment effects of artificial intelligence.

Deming, D., Ong, P. and Summers, L., 2024. Skill evolution in the AI era.

Hamilton Project, 2025. Corporate AI investment tracker.

Heritage Foundation, 2024. What AI means for the future of work.

Kolko, J., 2026. Supplementary datasets for AI–labour exposure metrics.

Organisation for Economic Co-operation and Development (OECD), 2023a. Artificial intelligence and the labour market: Introduction. In OECD Employment Outlook 2023.

Organisation for Economic Co-operation and Development (OECD), 2023b. OECD Employment Outlook 2023.

Organisation for Economic Co-operation and Development (OECD), 2024. OECD Employment Outlook 2024 – Country notes: United States.

Organisation for Economic Co-operation and Development (OECD), 2025. AI task taxonomy and workforce survey.

Organisation for Economic Co-operation and Development (OECD), n.d.a. Artificial intelligence and the changing demand for skills in the labour market.

Organisation for Economic Co-operation and Development (OECD), n.d.b. The impact of artificial intelligence on productivity, distribution and growth.

Omer, U., 2025. The 18-month legal-tech sales cycle: Why it takes forever (and how winners use this to their advantage).

Stevens, R., 2026. Payrolls to prompts: Firm-level evidence on the substitution of labour for AI.

The Economy, 2026. Why artificial intelligence may lead to structural job loss.

World Bank, 2025. Global digital capital outlook.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.