$15 Billion Inflows Defy U.S.-China Tensions, Sparking Strongest Buying in Five Years

Authored On

Modified

Reassessment of Valuation Appeal in Chinese Equities

Beijing’s Backing of “Tech Rise” Proves Effective

All-Out Push to Revive Markets Amid Persistent Geopolitical Risks

Even amid escalating U.S.-China trade frictions, American investors aggressively accumulated Chinese and Hong Kong equities, signaling the strongest level of interest in five years. The move reflects a convergence of perceptions that U.S. equities have reached elevated levels and that Chinese technology firms offer compelling undervaluation, triggering a substantial return of Western capital. Institutional reforms, including expedited listing reviews in Hong Kong, alongside technological breakthroughs in artificial intelligence (AI), further acted as key magnets for global funds. Despite lingering market uncertainty, the logic of capital seeking returns appears to be exerting greater force.

A Clear Signal of a Full-Fledged Return of Western Capital

According to multinational bank BNP Paribas, U.S. investors were net buyers of $9 billion in Asian equities in the fourth quarter of last year, bringing total annual investment to $80 billion. Of that amount, 19%, or $15 billion, flowed into China or Hong Kong. After posting net selling from the second half of 2024 through the first half of 2025, U.S. investment in China and Hong Kong reversed to net buying in the fourth quarter of last year. Hong Kong’s Hang Seng Index surged 28% over the past year, outperforming the S&P 500’s 16% gain, while U.S. holdings of Chinese and Hong Kong equities rose 46% year-over-year to $415 billion from $280 billion.

This capital movement is widely interpreted as evidence that, even amid intensifying trade tensions, investment flows have gravitated toward tangible returns and valuation appeal. Interest in China among major U.S. institutional investors has climbed to its highest level in five years. According to a Morgan Stanley report released late last year, more than 90% of surveyed investors said they were willing to increase exposure to Chinese equities. The figure marks the highest level since early 2021, when China’s stock market peaked, and is viewed as a signal of a broader return of Western capital.

Investors indicated they are seeking undervalued innovative assets in China, focusing on emerging sectors such as humanoid robotics and biotechnology, as well as new consumer enterprises. Laura Wang, Morgan Stanley’s chief China equity strategist, said that despite elevated levels of interest, the return of U.S. investors to China remains in its early stages, with significant room for further inflows. Growing recognition that Chinese policymakers have begun implementing gradual measures to stabilize the economy and nurture capital markets has reinforced optimism that the worst period has passed.

Concerns over stretched valuations in U.S. equities and portfolio reallocation strategies have also shaped these flows. Chris Wood, global head of equity strategy at Jefferies, said at a forum in Hong Kong that U.S. equities appear to have peaked, making it a more opportune time to buy European and Chinese stocks. He cited the United States’ 67.2% weighting in the MSCI World Index and a market capitalization-to-GDP ratio of 209% as evidence. Portfolio diversification demand has consequently shifted in significant part toward China and Hong Kong.

Blunt Corporate Support Drives Investment Returns Higher

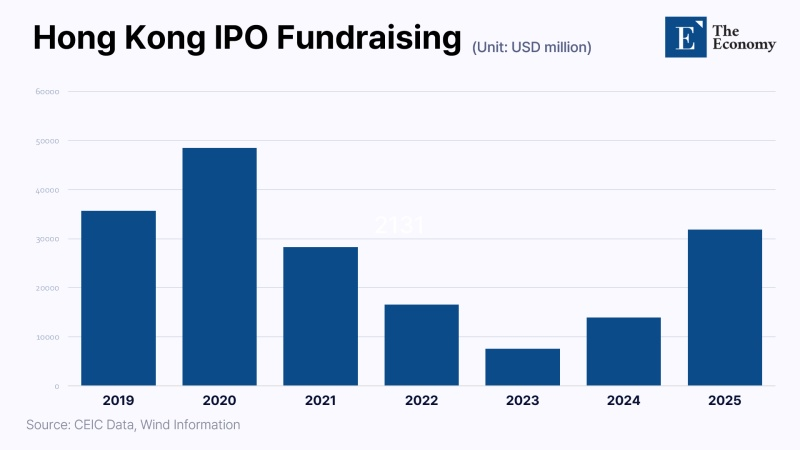

Domestically, Beijing’s industrial policy has proved instrumental. Extensive support for advanced industries, particularly AI and semiconductors, has fueled corporate growth and enhanced investment appeal. Data from the International Financial Center show that companies raised $37.15 billion through initial public offerings (IPOs) in Hong Kong last year, more than doubling from the prior year. The number of companies listing on Hong Kong Exchanges and Clearing rose more than 70% year-over-year to 117, surpassing both the New York Stock Exchange and Nasdaq to rank first globally in IPO activity.

While tightening oversight of mainland-listed firms, Chinese authorities have adopted an aggressive dual-track approach by offering exceptional support to Hong Kong’s financial markets. In April of last year, the China Securities Regulatory Commission announced plans to support IPOs of major Chinese enterprises in Hong Kong and to ease rules governing stock trading links between Hong Kong and mainland exchanges. As a result, the range of exchange-traded funds (ETFs) eligible under the Shenzhen-Hong Kong and Shanghai-Hong Kong Stock Connect programs was expanded, and real estate investment trusts (REITs) were included in cross-border trading. Hong Kong Exchanges also sharply reduced listing review periods to 30 business days for high-quality companies with market capitalizations exceeding $1.3 billion, underscoring proactive reforms.

In addition, Hong Kong Exchanges established a dedicated support team for technology companies in May of last year and introduced confidential listing review procedures to protect early-stage firms. Consequently, a substantial portion of newly listed companies concentrated in information technology and healthcare. AI-driven drug discovery company Insilico Medicine, digital twin specialist 51World, and home robotics developer Unitree Robotics successfully raised capital in Hong Kong, positioning themselves at the forefront of China’s technological ascent. PricewaterhouseCoopers projected that IPO activity could reach as much as $41.6 billion this year.

Chinese AI-related stocks have maintained strength in contrast to U.S. software companies unsettled by AI-driven volatility. MiniMax Group, an AI firm that drew significant investment from Alibaba, surged 488% following its January listing, while Knowledge Atlas Technology climbed 524%. AI chip design companies Biren Technology and Montage Technology posted gains of more than 80% and 98%, respectively, meeting market expectations. Charu Chanana, chief investment strategist at Saxo Markets, said China’s focus on commercializing AI has left it comparatively less exposed to shifts in investor sentiment.

Balancing Capital Repatriation and Rising Taiwan Strait Tensions

Against this backdrop, Beijing has launched a full-scale campaign to revive equity markets and recapture departing Western capital. In a report earlier this month, Barings noted that Hong Kong and Chinese equity markets have enhanced their medium- to long-term investment appeal on the back of technological innovation, industrial upgrading, and expanded policy support. From a valuation perspective, Chinese equities are trading at discounts of more than 35% relative to major U.S. and European markets. William Fong, head of Hong Kong and China equities at Barings, said China’s industrial transformation presents an attractive opportunity for long-term investors and represents a favorable moment for portfolio diversification as markets enter a structural rebound phase.

Large-scale IPOs are also in the pipeline. Syngenta Group, the agricultural subsidiary of China National Chemical Corporation, is considering a listing of up to $10 billion to test market appetite, while Kunlunxin, the AI chip unit affiliated with Baidu, has filed for an IPO on the Hong Kong Stock Exchange, reinforcing the trend of technology firms gravitating toward Hong Kong. The developments also present significant opportunities for Chinese investment banks. Last year, Chinese firms accounted for nearly 70% of underwriting fees in Hong Kong’s IPO market, totaling $579 million.

Hong Kong authorities are moving in tandem to strengthen the city’s dominance in capital markets. Hong Kong Exchanges plans to maximize efficiency and liquidity by refining listing rules, including narrowing bid-ask spreads. With 488 companies currently awaiting listing approval, the sustained IPO momentum underpins Hong Kong’s reestablished role as the primary dollar-funding gateway for Chinese enterprises. Mainland capital participation in Hong Kong equities has reached record highs, fundamentally improving liquidity conditions and reinforcing the market’s competitive standing as a long-term strategic base.

Nevertheless, despite these supportive measures, geopolitical tensions surrounding the Taiwan Strait remain a critical variable constraining asset revaluation. After President Donald Trump imposed a 15% tariff on all countries worldwide, heightened uncertainty has compounded ongoing geopolitical risks, acting as a barrier to sustained Western investment. Investors continue to weigh short-term policy effects against the trajectory of external tensions in assessing China’s long-term growth prospects. Ultimately, the success of China’s equity market revival strategy will hinge on how effectively it restores confidence in its role as both a core production base and a financial hub.

Similar Post