[Fed Watch] Fed Holds Rates at 3.50–3.75%, Rate Cut Expectations Recede Amid War-Driven Uncertainty

Authored On

Modified

Concerns Over Prolonged War-Driven Inflation Officially Reflected

Rising Pressure From Oil and Interest Rates, Currency Markets React

Transmission to Real Economy Signals Weaker Consumption and Downside Growth Risks

The Federal Reserve has held its benchmark interest rate steady for a second consecutive meeting, effectively postponing a definitive stance on the direction of monetary policy. The primary rationale cited was the uncertainty surrounding the economic impact of developments in the Middle East. As a result, market attention is shifting away from the immediate rate decision itself toward how the conflict may shape future inflation and growth trajectories. In bond and foreign exchange markets, movements reflecting the possibility of renewed rate hikes have emerged, while concerns are growing in the real economy that rising energy prices could translate into increased pressure on consumer spending.

Persistent Inflationary Pressure

On the 18th (local time), following the previous day’s session, the Federal Reserve concluded its Federal Open Market Committee (FOMC) meeting and decided to maintain the benchmark interest rate at 3.50–3.75%. This marks the second consecutive hold following three rate cuts between September and December last year and another hold in January. In this decision, Governor Stephen Miran advocated for a 0.25 percentage point cut, but the remaining 11 members voted to keep rates unchanged, underscoring the Fed’s strong internal vigilance regarding inflation. In its post-meeting statement, the Fed noted that “uncertainty about the economic outlook remains elevated,” adding that “the implications of developments in the Middle East for the U.S. economy remain uncertain,” explaining the rationale behind the decision.

Internal views on the future rate path were detailed through the dot plot. Among the 19 participants—12 voting members and 7 non-voting regional Fed presidents—year-end rate projections were distributed as follows: 7 participants projected 3.50–3.75%, 7 projected 3.25–3.50%, 2 projected 3.00–3.25%, 2 projected 2.75–3.00%, and 1 projected 2.50–2.75%. Compared with the December dot plot—where projections were more widely dispersed, including higher ranges—the current distribution indicates a prevailing expectation of maintaining current levels or gradual easing.

In its updated economic projections released alongside the decision, the Fed raised its forecast for this year’s personal consumption expenditures (PCE) inflation to 2.7%, up 0.3 percentage points from December. Core PCE, excluding food and energy, was also revised upward from 2.5% to 2.7%. Real GDP growth for this year was projected at 2.4%, up 0.1 percentage points, while next year’s growth forecast was raised by 0.3 percentage points to 2.3%. The unemployment rate was projected at 4.4% for this year and 4.3% for next year, showing little change. The Fed stated that “inflation remains somewhat elevated,” signaling concern that upward price pressures may persist longer than previously expected.

Rising energy prices were also identified as a key variable in policy decisions. Recently, U.S. oil prices climbed to around $99 per barrel, a level seen as exerting upward pressure across the broader price environment. Federal Reserve Chair Jerome Powell emphasized that supply shocks cannot be dismissed lightly, stating that “whether to look through supply shocks is not a trivial decision,” and that “even shocks typically considered transitory under normal conditions require a cautious approach.” This suggests that the surge in global oil prices linked to the Middle East conflict may extend beyond a short-term factor and influence the medium- to long-term inflation trajectory.

Warnings of Rate Reversal and Expanding Market Sell-Off

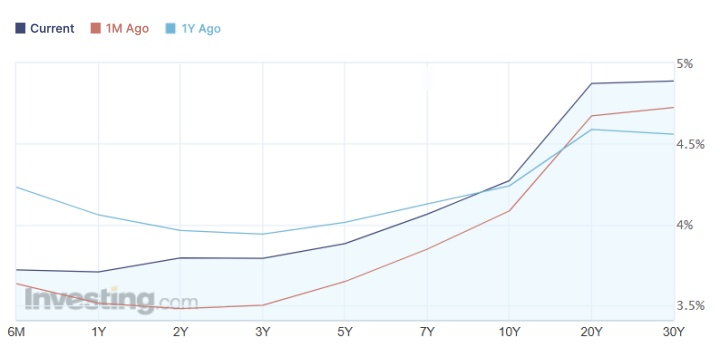

As expectations for rate cuts fade, some market participants are beginning to consider the possibility of renewed rate hikes. A prolonged Middle East conflict could reignite inflation through higher oil prices, leading U.S. interest rates to remain elevated longer than anticipated. In the New York bond market on the same day, U.S. Treasury yields rose across the curve. The policy-sensitive two-year yield increased by 9.1 basis points to 3.762%, the 10-year yield rose 5.9 basis points to 4.261%, and the 30-year yield climbed 2.6 basis points to 4.878%. This reflects the broad impact of retreating rate-cut expectations.

As war-related risks intensify, the trajectory of oil prices has increasingly become a central variable in monetary policy considerations. Following U.S. and Israeli strikes on Iran, concerns over supply disruptions grew as Iran targeted refining facilities and signaled potential moves to restrict passage through the Strait of Hormuz. During this period, oil prices briefly surged to around $120 per barrel before partially stabilizing below $100. Nevertheless, expectations persist that supply-driven upward pressure could strengthen again. Consulting firm Wood Mackenzie projected that if the conflict continues for more than three months, oil prices could exceed $150 per barrel.

These oil price dynamics are directly influencing broader financial markets. The U.S. dollar strengthened against the euro for three consecutive days, approaching its highest level of the year, while the dollar index—measuring the currency against six major peers—rose more than 1.5% to its highest level since November last year. In contrast, currencies of energy-importing countries weakened. The Indian rupee and Japanese yen each declined by more than 1.5% following the outbreak of the conflict, while the euro fell about 2% and the Korean won dropped roughly 3%. The euro–dollar exchange rate declined 0.5% to 1.1513, trading near its lowest level since November.

International organizations and major financial institutions have also warned that a prolonged conflict could simultaneously drive higher interest rates and increased market volatility. The Bank for International Settlements (BIS) warned that “if the Middle East conflict evolves into a prolonged war, a sharp rise in interest rates and a broad-based market sell-off will be unavoidable.” BMO Capital Markets similarly noted that “the fiscal consequences of a prolonged conflict are likely to extend the weakness in U.S. Treasurys,” while Benjamin Ford of Macro Hive added that “uncertainty in energy supply, combined with geopolitical risks, is driving increasing volatility in foreign exchange markets.”

“Invisible Tax” Pressures Consumer Spending

Experts argue that rising energy prices ultimately function as a de facto tax on consumers, reducing disposable income and weakening spending capacity. Tavis McCourt, a strategist at Raymond James, estimated that “every $20 increase in oil prices adds approximately $150 billion in annual consumer spending burden.” Industry estimates also suggest that a $10 increase in oil prices raises gasoline prices by about $0.25 per gallon, illustrating how energy costs translate directly into everyday consumer expenses.

This pressure is already reflected in consumer sentiment indicators. The University of Michigan’s consumer sentiment index fell to 55.5 in March, down 1.1 points from 56.6 in the previous month, marking its lowest level since December last year. Joanne Hsu, who oversees the survey, explained that “responses collected before the Iran war showed improvement compared with the prior month, but sentiment deteriorated sharply in responses gathered over the subsequent nine days, fully offsetting earlier gains.” She added that “while consumers immediately felt the impact of rising gasoline prices, the extent to which those increases will pass through to other goods remains highly uncertain.”

The contraction in consumption is also showing differentiated effects across income groups. Krishna Guha, vice chairman at Evercore ISI, warned that “persistent increases in oil prices could widen the K-shaped divergence across the economy.” He pointed to data showing that wages for higher-income groups rose 4.2% year-over-year in February, while wage growth for lower-income groups was limited to 0.6%. This indicates that even under the same energy price shock, lower-income households face disproportionately greater burdens. Earlier in the year, expectations had been that tax refunds from the Trump administration’s tax cuts would support consumption, but rising oil prices are now weakening that outlook and exerting downward pressure on the consumer base.

Similar Post