Warning That Stablecoins Could Become a “Trigger for Financial Crisis”; Without Global Coordination, Worldwide Financial Panic May Follow

Authored On

Modified

Urgent need to address stablecoins as a threat to the global financial order Structural flaws in stablecoins, a flashpoint lurking in the regulatory blind spot Left unchecked, they could fuel risk-asset investment and trigger a “bank run”

Warnings are mounting from international institutions and academia over the “systemic risk” that stablecoins could unleash. If the crypto market suffers a major shock or liquidity tightens in traditional short-term funding markets, the result could be a wave of mass redemptions — a stablecoin “bank run” — that sends shockwaves across the global financial system. Concerns are also intensifying that, because stablecoins are largely operated through a U.S. Treasury-centered structure, crises could drive capital sharply into the United States, simultaneously deepening global liquidity imbalances and financial instability.

BIS Chief Calls for International Standards to Block “Regulatory Arbitrage” Exploiting National Gaps

According to Reuters on April 20, Pablo Hernandez de Cos, general manager of the Bank for International Settlements (BIS), said in a speech in Japan that “global coordination is critically important, given the potential for stablecoins to weaken a country’s monetary and fiscal policies, generate stress in financial markets, and undermine anti-illicit-financing efforts.” He added that, absent such coordination, divergent national regulatory frameworks for stablecoins could produce severe market fragmentation or enable harmful regulatory arbitrage. Regulatory arbitrage refers to the practice of firms seeking out the loosest jurisdictions in pursuit of risk-free profits.

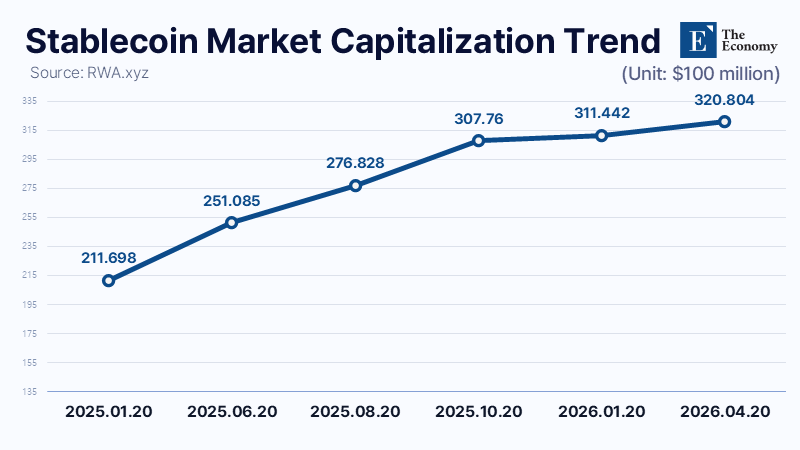

He went on to say that current stablecoins “function like financial assets in capital markets,” warning that this creates a significant risk of triggering a bank run during unexpected episodes of market turmoil. Referring to Tether and Circle — the two dominant issuers that account for roughly 85% of the $315 billion global stablecoin supply — he said they exhibit characteristics “closer to securities than money.” He took particular issue with redemption frictions that frequently cause them to deviate from par. In that sense, de Cos added, they currently operate more like exchange-traded funds than currency.

De Cos also weighed in on the core debate over whether stablecoins should be allowed to pay interest like traditional bank deposits. He said that if stablecoin holdings do not bear interest — particularly during periods of elevated rates, when the opportunity cost of holding them remains high — migration from bank deposits into stablecoins may prove less pronounced. He added that this would hold only if a ban on interest payments for stablecoins can actually be enforced.

Potential to Trigger a Financial Crisis Through a Bank Run

De Cos’s remarks align with concerns that academics and financial experts have raised for years. At the center of the debate is structural fragility. Jean Tirole, a Nobel laureate in economics and professor at the Toulouse School of Economics in France, has likewise warned that a bank run becomes highly likely if confidence in stablecoin oversight or in the underlying reserve assets that determine a coin’s value begins to erode. He said many investors mistakenly view stablecoins as a “perfectly safe deposit,” when in fact they are not. He stressed in particular that, because the returns on U.S. currency, deposits and short-term Treasuries permitted as stablecoin reserves are relatively low, issuers may be tempted to seek higher returns by investing in riskier assets.

He also noted that U.S. Treasury yields were negative for years and can fall even further in real terms when inflation accelerates. In such circumstances, if stablecoins decline, governments could come under enormous pressure to rescue instruments that had effectively been treated like deposits. He acknowledged that these risks could be managed if global regulators were adequately staffed and approached the issue with exceptional caution. But he stressed that, with President Donald Trump and other senior figures in the U.S. administration holding personal stakes in crypto, political interests and ideological considerations could become obstacles to stronger regulation.

Michael Barr, the Federal Reserve’s vice chair for supervision, also pointed to the risks posed by stablecoins. He identified money laundering and terrorist financing as the foremost concerns. Barr said criminals are exploiting the fact that stablecoins can be purchased in secondary markets without customer identification requirements, arguing that regulatory and technological remedies are essential to block such abuse. He identified financial stability as the second major risk. Investors generally assume that stablecoins can be redeemed at par whenever they choose, but if the quality of reserve assets deteriorates, issuers may be unable to withstand large-scale withdrawals in a crisis.

Barr also said that issuers have an incentive to invest reserves in higher-risk assets in order to maximize returns, warning that while such a strategy boosts profits in boom periods, it can destroy confidence in the system during market stress. He invoked the era of free banking in 19th-century America, the Panic of 1907, the 2008 global financial crisis, and the liquidity strains suffered by money market funds during the 2020 pandemic, calling them reminders of “the painful history caused by privately issued money with inadequate safeguards.”

The reserve assets held by stablecoin issuers may be considered safe assets, but the picture changes once investors begin to doubt even those holdings. If, in a crisis, investors begin to fear they may not get their money back, mass redemptions could follow and quickly trigger a liquidity crunch. A clear example came during the collapse of Silicon Valley Bank in 2023, when USDC — issued by Circle — fell to $0.88 simply because 8% of its reserves were deposited at the failed bank. At the time, USDC holders sought to redeem $10 billion, pushing up short-term market rates.

The United States Gains, While Other Countries Bear the Cost

There is also a growing view that while the spread of stablecoins benefits the United States, it could become a new source of financial-crisis risk for the rest of the world. In a Financial Times column, chief economics commentator Martin Wolf argued that the international proliferation of dollar-based stablecoins effectively amounts to the privatization of seigniorage and serves to shift America’s fiscal problems onto the instability of global finance.

Wolf said the particularly rapid growth of stablecoins in the United States has been driven by high credit-card fees, inefficient remittance systems and costly cross-border payments. He argued that the U.S. financial system is slower and more expensive in payments than Europe’s, and that excessive influence by oligopolistic firms has needlessly raised consumer costs. Those inefficiencies, he said, have become the very foundation supporting the growth of privately issued dollar stablecoins. He also raised the possibility that the U.S. Treasury could deploy stablecoins strategically. According to Wolf, Washington could view the overseas expansion of dollar stablecoins as a means of ensuring that the world continues absorbing vast U.S. Treasury issuance. In effect, that would make stablecoins part of an American strategy to reinforce financial hegemony.

Wolf argued that if the United States continues tolerating the international spread of stablecoins under a lax regulatory regime, other countries will need defensive strategies to protect their own monetary and financial sovereignty. He pointed to the United Kingdom as a model case. When the Bank of England unveiled proposed rules for pound-denominated stablecoins late last year, it said regulated stablecoins could make domestic and international payments faster and cheaper while improving functionality. In that context, Wolf urged governments to build precise, independent and transparent regulatory frameworks in order to avoid the risks posed by America’s lightly regulated stablecoin model.

In practice, stablecoin issuers invest most of their reserves in U.S. Treasuries. That structure creates a channel through which global capital flows into U.S. financial markets via stablecoins. As a result, capital from other countries, including emerging markets, can be drawn into the United States, leaving those economies exposed to a more fragile financial position. This asymmetry becomes even more acute in times of crisis. If confidence in stablecoins falters, mass redemptions can force reserve-asset liquidations. That raises the likelihood of shocks to the Treasury market and a simultaneous squeeze in global liquidity. Through stablecoins, the United States lowers its funding costs and entrenches dollar supremacy, while other countries are left to absorb the resulting financial risks in full.

Similar Post