When the Signal Is Noisy: Rethinking CDS Market Efficiency in Modern Financial Markets

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

CDS spreads do not always reflect true credit risk Market frictions and low liquidity distort price signals Better transparency can improve CDS market efficiency

In global finance, the speed at which credit default swap (CDS) spreads move across markets is remarkable. Even a minor shift, measured in basis points, can alter the perceived risk of a bank, a company, or a country. A market smaller than it used to be generates these signals. The Bank for International Settlements reported that the global CDS market had around $9 trillion in gross notional outstanding in 2024. Before the global financial crisis, this figure was over $60 trillion. Although the market has shrunk, CDS spreads still play a role in how market participants and regulators view credit risk, appearing in financial news, central bank reports, and risk dashboards worldwide. The issue is that the information conveys the impression of a smoothly running market. What is really happening is that the CDS market is affected by trading problems, insufficient assets that can be quickly converted into cash, and the way companies are organized. These things can make price signals confusing. Policymakers and experts might get the wrong idea about what the market is telling them if spreads reflect how quickly something can be sold rather than default risk. So it is important to look at how well the CDS market works again. The goal is not to ignore CDS markets but to know what they cannot do and to make rules that help people understand their signals.

Reasons to be Doubtful of CDS Market Efficacy

The main point of a credit default swap is easy to understand. One party makes regular payments to another to protect the other if a borrower cannot repay their debt. The payment, known as the CDS spread, should reflect the likelihood that the borrower will default on their debt. The spread is expected to reflect the collective beliefs of many investors who are aware of the borrower’s financial status. When markets have many participants and active competition, this combining process can lead to prices that closely match market conditions.

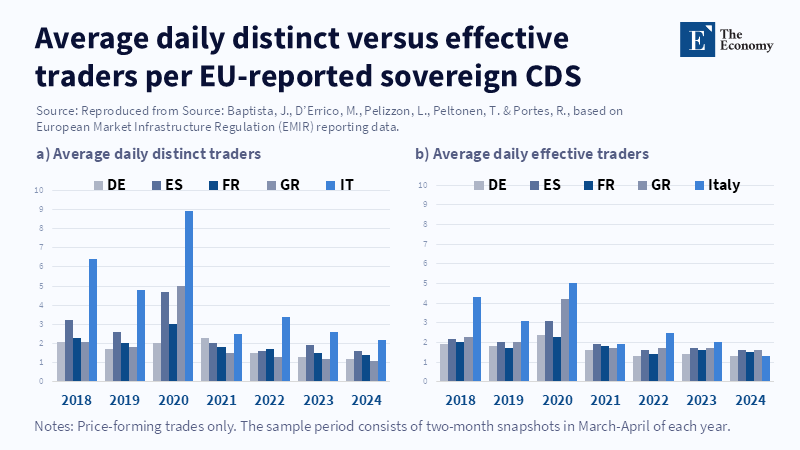

CDS markets do not fit the ideal model of an efficient financial market. Most trading is done by a small group of big banks that act as dealers and provide assets that can be quickly converted to cash. These institutions are in the middle of most trades, and their choices affect the spreads seen in the market. If a dealer wants to reduce risk or change what they have available, spreads can change even if there are no new details about the underlying borrower.

Studies on the small details of how the CDS market works show that how easy it is to sell assets impacts how prices are set. Arakelyan and Serrano show that CDS spreads usually include a liquidity payment, meaning that part of the spread compensates investors for the cost of trading the contract rather than for the expected loss from default. This payment may rise when it is harder to convert assets into cash. As a result, spreads can go up even if the borrower’s credit rating does not change.

Research on policy shows similar results. A paper by the European Systemic Risk Board says that CDS markets are still controlled by a small group of participants and that access to assets may become difficult during financial distress. When assets can quickly be exchanged, price changes become more common, and spreads may go higher than what they are actually worth. This change is important for decision-makers who rely on CDS spreads to anticipate problems. It can be hard to tell whether rising default risk is real or just a temporary market issue.

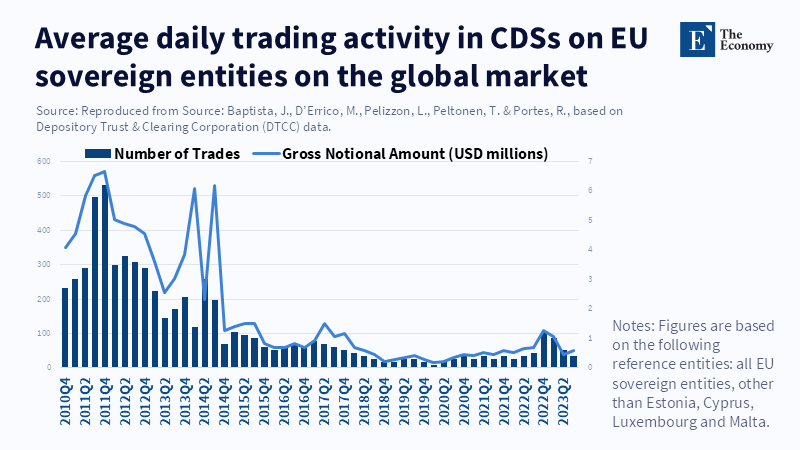

Another factor that hurts how well the CDS market works is its shrinking size. Due to trade compression and regulatory changes, the gross notional amount of CDS contracts has decreased. While this has boosted financial stability by reducing how much people owe to each other, it has also reduced the number of trades, thereby improving price discovery. Because there are fewer trades, a single trade can significantly change the quoted spreads. This makes the price signals less clear.

Market Details and the Problem of CDS Market Efficacy

To understand why CDS spreads sometimes do not match market conditions, you need to pay attention to the specifics of how trading is carried out. Financial experts say that market performance occurs when many traders who know what they are doing work together, enabling assets to be sold quickly. Prices then show collective market knowledge. But this process stops working when only some people are involved or when trading costs are high.

Theoretical research on broken markets gives insight into this problem. Albagli, Hellwig, and Tsyvinski say that when markets lack all the facts or when few people participate, price signals can become confusing. Investors may then act in response to prices that do not completely show market conditions. These problems can alter investment choices and lead to inefficient outcomes.

CDS markets have things that cause these problems. One is that bid-ask spreads are wider than those for more liquid financial instruments. These spreads are the amounts dealers charge for providing assets that can be quickly turned into cash. When price shifts are common or regulations tighten, dealer balance sheets may be strained, leading the people who make markets to trade less. It also means fewer trades occur and it is tougher to find prices.

Another issue is how derivatives markets are connected. CDS trading occurs alongside other credit instruments, such as corporate bonds and structured products. What happens in one market can affect other markets. Traders may quickly shift positions between markets when financial trouble arises, altering risk conditions. These quick changes can make prices swing for a short time, but they do not directly reflect changes in credit conditions.

Real data support these microstructural effects. During the European sovereign debt crisis, CDS spreads on sovereign issuers widened significantly. Some of this was due to real worries about fiscal policy; researchers found that a lack of assets and worried dealers also contributed to higher spreads. Similar things have occurred in corporate CDS markets, where spreads can change significantly when the market is struggling.

The European Systemic Risk Board says that these things happen often. The structure of the CDS market makes it likely to have problems if assets are hard to obtain and if one company has too much control. Because of these structural features, spreads should be seen as signals influenced by both credit risk and market conditions.

Policy Changes to Make CDS Market Efficacy Stronger

Knowing the disadvantages of the CDS market health does not mean leaving the market. CDS contracts can still be used to protect credit and provide information about how the market assesses risk. The goal of policy must be to increase the trustworthiness of the signals it creates.

One thing that can be done is to be more open about trading. Rules put in place after the financial crisis require detailed reports of derivatives trades to be submitted to trade repositories. But, regulators are the only ones who can access most of this data. Posting combined facts on trading volumes and market participants would help experts assess how well CDS price signals work. It is more likely that spreads reflect real changes in credit risk when markets are very active.

Central clearing is another area where policy choices affect market effectiveness. Clearinghouses lower counterparty risk by requiring participants to post margin for derivatives trades. These protections increase economic security; they can also change trading behavior. Margin requirements often rise when the market is moving. When margins rise sharply, traders may reduce positions or sell assets that can be quickly sold out of the market. This action can make price movements larger and reduce the spread details. The European Systemic Risk Board says that margin actions can change derivatives markets in ways that worsen market conditions. Creating margin plans that account for asset conditions may help stabilize price formation.

Allowing more people to join CDS markets would improve price discovery. Right now, trading is mostly done by a small group of big banks. Getting institutional investors and non-bank asset providers who can be quickly sold to join would increase the variety of ideas reflected in market prices. If there were more participants, individual dealers would have less effect on spread movements.

Another helpful policy innovation would be to develop metrics that measure the effectiveness of CDS price signals. These measures could track things like how often trades occur, how much of the market a company controls, and bid-ask spreads. Experts could then understand CDS spreads based on the market conditions where they are created. Spreads would have greater informational value when assets can be quickly turned into cash and many people are participating. You would have to be more careful when it is hard to get assets.

What Teachers and Policy Makers Need to Know About CDS Market Efficacy

The debate about the health of the CDS market also means that financial markets are taught and studied. Derivative prices are presented in many finance courses as simple reflections of what the market expects. Students are taught to get default rates from CDS spreads and to see these values as market measures of credit risk. This way of thinking ignores the market setting where prices are formed.

Putting market bits together into a financial education would create a more realistic picture of derivatives markets. Students should examine how assets that can be quickly converted into cash, dealer actions, and changing regulatory rates affect prices. Studying times of market trouble from the past can show how spreads react not only to market conditions, as well as to changes in trading conditions.

For decision-makers, it is important to understand that CDS spreads should be considered alongside other factors, not in isolation. CDS data can provide remarkable market details; however, other factors need to be added, such as bond markets, balance sheets, and metrics for how everything is working. Using details from many sources reduces the risk that short-term issues due to asset shortages will be mistaken for market transitions in credit risk.

There is also a need for coordination internationally. CDS markets work across governments, and trading conditions in one place can change prices everywhere. If they set the same transparency standards and share data among regulators, it would improve the group's overall understanding of market activity. Such cooperation could help governments tell whether price shifts and temporary asset problems are real.

These lessons are more marketable because the CDS market has gotten smaller since the financial crisis. Even if the market is smaller, it can still greatly affect ideas of risk. When policymakers and investors treat CDS spreads as precise signals, they may overlook the structural factors that determine those prices. Understanding the disadvantages of the CDS market helps people analyze market data more carefully. Financial markets remain strong sources of information, but their signals do not always clearly reflect economic reality. Not having enough assets, market rules, and regulations all affect how prices go up. Policymakers and teachers can ensure that CDS markets continue to provide insights if they remember these things, which helps them not overstate how clear their signals are. The key between details and noise in a difficult financial system is not in the data but in how it is understood.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Adrian, T., Fleming, M., Goldberg, J., Lewis, M., Natalucci, F.M. & Wu, J.J., 2013. Dealer balance sheet capacity and market liquidity during the 2013 selloff in fixed income markets. Federal Reserve Bank of New York Economic Policy Review.

Albagli, E., Hellwig, C. & Tsyvinski, A., 2018. Imperfect financial markets and investment inefficiencies. Toulouse School of Economics Working Paper No. 891.

Arakelyan, A. & Serrano, P., 2016. Liquidity in credit default swap markets. Journal of Multinational Financial Management, 37–38, pp.139–157.

Ashcraft, A.B. & Santos, J.A., 2009. Has the credit default swap market lowered the cost of corporate debt? Journal of Monetary Economics, 56(4), pp.514–523.

Baptista, J., D’Errico, M., Pelizzon, L., Peltonen, T. & Portes, R., 2026. Credit default swaps: analysis and policies. VoxEU Column, Centre for Economic Policy Research.

Bank for International Settlements, 2024. OTC derivatives statistics at end-June 2024. BIS Quarterly Review. Basel: Bank for International Settlements.

Colliard, J. & Foucault, T., 2012. Trading fees and efficiency in limit order markets. Review of Financial Studies, 25(11), pp.3389–3421.

Congressional Research Service, 2024. Derivatives trading in U.S. banking. Washington, DC: Congressional Research Service.

Entrop, O., Schiemert, R. & Wilkens, M., 2011. Valuation differences between credit default swap and corporate bond markets. Journal of Credit Risk, 7(3), pp.1–24.

European Systemic Risk Board, 2025. Credit default swaps: analysis and policies. Frankfurt: European Systemic Risk Board.

Fu, X., Li, M.C. & Molyneux, P., 2021. Credit default swap spreads: market conditions, firm performance, and the impact of the 2007–2009 financial crisis. Empirical Economics, 60, pp.2851–2879.

Longstaff, F.A., Mithal, S. & Neis, E., 2005. Corporate yield spreads: default risk or liquidity? New evidence from the credit-default swap market. Journal of Finance, 60(5), pp.2213–2253.

Massa, M. & Zhang, L., 2023. Credit default swaps, fire-sale risk, and the liquidity provision in the bond market. Journal of Financial and Quantitative Analysis.

Paddrik, M. & Tompaidis, S., 2019. Market-making costs and liquidity: evidence from CDS markets. Office of Financial Research Working Paper.

The North American Journal of Economics and Finance, 2013. Determinants of bank credit default swap spreads: the role of the housing sector. North American Journal of Economics and Finance, 24, pp.243–259.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.