Europe’s Industrial Crossroads: Why an Effective EU Industrial Strategy Must Begin with Strength, Not Subsidy

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

Europe should build an EU industrial strategy based on its own strengths Subsidies work only when strong markets and supply chains exist Europe must reinforce its industrial advantages, not copy U.S. policy

In 2023, the United States saw a large increase in industrial investment—the biggest in decades. After the Inflation Reduction Act (IRA) was passed, companies quickly announced investments totaling over $360 billion in clean energy and manufacturing across the nation. Factories for batteries and electric vehicles, along with projects for hydrogen and semiconductor facilities, began appearing on investment maps almost immediately. This sudden surge sparked discussions in Europe, where officials wondered whether the European Union should adopt the American approach. At first, the answer might seem simple: If subsidies are bringing factories to the U.S., Europe should respond with its own subsidies. But this idea misses an important point. According to Le Monde, the IRA succeeded in the United States because it supported industries with high demand, access to strong capital markets, and advanced technologies. The main issue facing Europe is therefore different. Instead of just copying the U.S.'s policies, the EU needs to determine where its companies already have a strong edge in the world and then create an industrial plan that builds on those strengths. Without this solid base, subsidies could become costly gestures rather than real drivers of industrial growth.

EU Industrial Strategy and Europe’s Structural Investment Gap

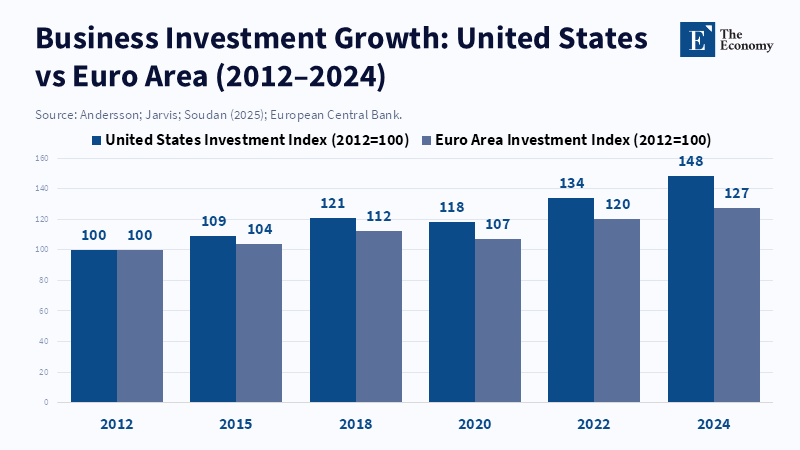

Any serious conversation about the EU’s industrial strategy must start with Europe’s investment situation. Over the last 10 years, the euro area has consistently invested less in business compared to the United States. Research from the European Central Bank shows that investments in things other than housing in the U.S. have grown much faster than in the euro area since the early 2010s. According to the OECD, while the United States leads the European Union in investment capacity and competitiveness, the report does not specifically cite stronger venture capital systems, more connected financial markets, or faster company growth as the main reasons for this difference. The gap is particularly relevant in important sectors such as advanced manufacturing, clean technology, and digital infrastructure.

Several structural issues explain the investment gap. Europe’s financial markets are still divided by national borders, making it more expensive for companies to raise the capital they need to expand across the single market. Also, rules and regulations can vary across member countries, which slows down large industrial projects and makes investors unsure. Energy costs in Europe have also been less stable in recent years, especially after the energy crisis caused by Russia’s invasion of Ukraine. These factors influence where companies decide to locate their factories, even before governments offer financial incentives.

Research conducted for the European Parliament highlights the limits of using subsidies to compete in this kind of environment. If countries try to attract investment mainly by offering subsidies, projects might just move from one country to another within the EU, rather than increasing Europe’s overall industrial capacity. In other words, these incentives may just shift investments internally rather than making the EU more competitive globally. This would go against the goal of an EU industrial strategy.

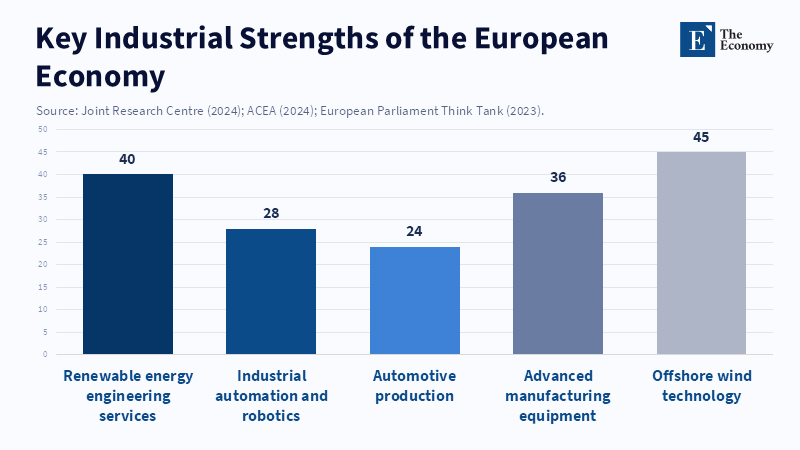

So, a better plan would be to first identify which European industries are already competitive. These include equipment for advanced manufacturing, industrial automation, renewable energy engineering, and automotive systems. Many European companies are leaders in specific parts of global supply chains, even if the final products are assembled elsewhere. Supporting these industries with focused policies—such as funding for innovation, procurement plans, and supply chain partnerships—can strengthen Europe’s industrial base more effectively than trying to create entire industries from scratch with only subsidies.

What the Inflation Reduction Act Actually Teaches EU Industrial Strategy

Before we apply any lessons from the Inflation Reduction Act to Europe, it is important to understand how the law is structured. The IRA created a wide-ranging system of tax credits and financial rewards to accelerate the local production of clean technologies, such as electric vehicles, batteries, hydrogen, and renewable energy equipment. Though it’s mostly seen as a climate policy, the law also acts as a strong industrial policy tool.

Many of the IRA's incentives are directly tied to requirements for local production or local supply chains. For instance, tax credits for electric vehicles are tied to where the batteries are made and where the key minerals come from—they must be sourced from the U.S. or from allied countries. These rules encourage companies to establish manufacturing plants in the American market. According to Stephanie J. Rickard, while traditional protectionist measures like tariffs have been used recently in the United States, the Trump administration has actually moved away from providing subsidies as part of industrial policy, instead expressing an intention to reduce government-funded business incentives. The scale of these incentives is a key aspect of the policy debate. Initial estimates put the total cost of the IRA’s climate and energy measures at around $369 billion over 10 years. But as companies began announcing new projects, analysts raised their estimates. The International Energy Agency estimates that global investments in clean energy exceeded $1.7 trillion in 2023, with a large share of that focused in the U.S. after the IRA was introduced. These investment expectations sent strong signals to investors and corporations thinking about new manufacturing capabilities.

Still, the IRA’s success isn’t only because of subsidies. The U.S. already had several advantages that made the policy even more helpful. The country has a large and well-connected domestic market, strong venture capital networks, and high demand for new technologies such as electric vehicles, artificial intelligence infrastructure, and cloud computing. Essentially, subsidies supported industries that were already expecting fast growth.

Europe is different. According to research by the European Investment Bank, industrial incentives work best when they are part of a supportive and helpful environment that includes financing, research, and market requirements (European Investment Bank, 2023). Without those things in place, subsidies might attract some investment announcements, but they won’t necessarily establish enduring industrial centers. For Europe, the lesson is not to give up on industrial policy, but to create one that accounts for the continent’s current economic strengths.

Where Europe Is Competitive: The Core of EU Industrial Strategy

Suppose the EU wants to create an industrial strategy that endures; it begins by identifying which European industries already lead in technology. One clear example is renewable-energy engineering. European companies were pioneers in many of the technologies used in offshore wind power, and they continue to be leaders in several parts of the global industry, including turbine design, project engineering, and maritime logistics.

These skills have been developed over decades of experience. Offshore wind projects need special ships, advanced materials, and complex engineering services. European companies have developed strong networks of suppliers and research institutions around these technologies. Supporting this system with targeted policies could strengthen Europe’s leading role in the worldwide shift to clean energy.

Research into Europe’s economic structure also shows how important services and innovation are to European industrial competitiveness. According to recent research, Europe’s industrial strengths often lie in combining advanced engineering with specialized services rather than in dominating mass production. This strategy helps European firms secure profits from the high-value segments of global value chains, even when most manufacturing occurs elsewhere.

The car industry is another good example. Europe is still one of the world’s largest producers of cars and car parts. As the industry moves toward electric mobility, maintaining technological leadership in car engineering, charging infrastructure, and advanced manufacturing systems could be more important than duplicating every step of the battery supply chain within Europe.

Policy research commissioned by the European Parliament stresses the importance of strengthening value chains rather than pursuing complete industrial self-sufficiency. In a globalized production context, economic security often depends on maintaining strong positions within international supply networks. An EU industrial strategy grounded in these realities can strengthen Europe’s advantages without copying the industrial structures of other economies.

From Subsidy Competition toward Strategic EU Industrial Strategy

The renewed interest in industrial policy around the world has led governments to compete by offering ever larger subsidy programs. While this kind of competition might seem unavoidable, history suggests that industrial policy is most successful when it supports industries that already have domestic capabilities. East Asian economies that successfully implemented industrial strategies did so by supporting industries that already showed potential for export, rather than creating entirely new sectors solely through subsidies.

For Europe, this suggests a shift in the policies that should be focused on. Instead of primarily focusing on subsidy levels, policymakers should strengthen the industrial systems that support innovation and production. Renewable energy offers a clear opportunity. Europe’s leadership in offshore wind technology could be strengthened through long-term infrastructure planning, investments in cross-border grids, and coordinated procurement plans.

Financial integration is another important part of an effective EU industrial strategy. Many innovative European companies struggle to grow because financial markets are still fragmented across the Union. According to Le Monde, integrating the European Union’s capital markets is seen as key for closing economic gaps with the United States, competing with China’s industrial growth, and supporting the EU’s green and digital transitions.

Coordination between member countries is also essential. Industrial policy in Europe is often implemented at the national level, leading countries to compete for the same investment projects. Without stronger coordination, subsidy competition might fragment the single market and weaken shared European goals. A clear EU industrial strategy would coordinate national incentives with broader European priorities, ensuring that public investment strengthens the Union’s industrial base rather than just moving projects around between member countries.

The Tactical Decision Behind EU Industrial Strategy

Europe is at a key point in the development of global industrial policy. The success of the Inflation Reduction Act has led to a wave of policy responses across developed economies. Though the lesson from the American experience isn’t just that subsidies attract investment. The more important lesson is that industrial policy works best when incentives support industries with strong markets, technological capabilities, and investment systems.

For Europe, the challenge is more strategic than just financial. An effective EU industrial strategy should begin by identifying which industries within European firms already have global advantages. These include renewable-energy engineering, advanced manufacturing technologies, and specialized industrial services. Policies that strengthen these systems can create long-term economic robustness while supporting the continent’s shift to a cleaner state.

Subsidies can still be important, but they should be used as focused accelerators, not as universal solutions. When they are aligned with strong industrial foundations, incentives can attract investment and stimulate innovation. When used without a clear strategy, they risk becoming expensive policy experiments with limited long-term impact.

So, Europe has a clear choice. It can try to copy the United States' subsidy model, or create a different industrial strategy based on its own economic strengths. The second path may require more careful planning, but it offers a much more sustainable way to grow. If European regulators create industrial policies grounded in real comparative advantages, the EU can remain a key actor in the global clean-technology economy rather than just react to policies made elsewhere.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

ACEA (European Automobile Manufacturers’ Association) (2024) Economic and Market Report: Global and EU Auto Industry – Full Year 2024. Brussels: ACEA.

Andersson, M., Jarvis, V. and Soudan, M. (2025) ‘Business investment: why is the euro area lagging behind the United States?’, ECB Economic Bulletin. Frankfurt: European Central Bank.

Arjona, R. and Tarantino, E. (2024) ‘The EU’s path to service growth and clean tech’, VoxEU / CEPR.

Battistini, N., Chiaie, S. D. and Gareis, J. (2023) ‘Monetary policy and housing investment in the euro area and the United States’, ECB Economic Bulletin, Issue 3.

Böckerman, P., Grönqvist, C. and Oikarinen, E. (2012) ‘Service innovation in manufacturing firms: Evidence from Spain’, Technovation, 32(2), pp. 144–155.

Cato Institute (2023) The Budgetary Cost of the Inflation Reduction Act’s Energy Subsidies. Washington, DC: Cato Institute.

European Commission (2023) Investment Barriers in the European Union 2023. Luxembourg: Publications Office of the European Union.

European Investment Bank (2023) The Inflation Reduction Act and the European Economy. Luxembourg: European Investment Bank.

European Parliament (2023) Global Value Chains: Potential Synergies Between External Trade Policy and Internal Economic Initiatives to Address the Strategic Dependencies of the EU. Brussels: European Parliament Think Tank.

International Energy Agency (2023) World Energy Investment 2023. Paris: International Energy Agency.

Joint Research Centre (2024) Advanced Manufacturing Industry is Growing Significantly in the EU. European Commission Joint Research Centre.

Jurkovic, P. (2023) What is the Inflation Reduction Act? London: UK in a Changing Europe.

Jan De Nul Group (2025) Jan De Nul. Aalst: Jan De Nul Group.

McKinsey & Company (2022) ‘The Inflation Reduction Act: Here’s what’s in it’, McKinsey Global Institute.

Scheinert, C. (2023) EU Response to the US Inflation Reduction Act. Brussels: European Parliament, Policy Department for Economic, Scientific and Quality of Life Policies (PE 740087).

U.S. Department of the Treasury and Internal Revenue Service (2023) U.S. Department of the Treasury, IRS Release Proposed Guidance to Continue U.S. Clean Energy Manufacturing Boom, Strengthen America’s Energy Security. Washington, DC: U.S. Department of the Treasury.

Westphal, L. E. (1990) ‘Industrial policy in an export-propelled economy: lessons from South Korea’s experience’, Journal of Economic Perspectives, 4(3), pp. 41–59.

Le Monde Editorial Board (2024) ‘Only an integrated capital market will give the EU the means to achieve its ambitions’, Le Monde.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.