Diversified Finance: Why Banking Group Diversification Limits National Financial Regulation

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

Banking groups shift lending across affiliates when regulation tightens This weakens policies aimed only at banks Effective oversight requires sector-wide and global coordination

The landscape of worldwide finance has experienced a subtle transformation, altering its basic structure. Financial institutions no longer function as separate entities limited by national boundaries. Instead, the financial sector is dominated by diverse banking groups that conduct banking activities, manage assets, provide private credit, and manage wealth in various locations. This change in structure has ramifications for how finance is controlled. Policy makers' actions to tighten bank rules do not always wipe out credit. Credit shifts location. Recent research on lending shows that tighter rules on banks often cause lending to move to related non-bank entities within the same financial groups. The intended policy outcome, which is to lower credit risk, is weakened when the activity moves to other entities. This tendency shows a structural push-and-pull between the spread of finance and the power of control. The spread of finance is a key idea. Institutions expand into different areas and regions to reduce risk and maintain stable income. Yet that same spread can weaken control when financial groups can move activities within it. When lending spans several companies or borders, the power of national rules to shape the full flow of credit diminishes. As financial institutions around the world keep expanding, the big challenge for policymakers is to control not just banks, but a financial system composed of interconnected institutions that do business across several areas and regions.

How Banking Group Spread Affects Entity-Based Rules

Having a variety has long been a core part of how financial institutions do things. Banks head into new markets, lines of work, and areas to balance risks and keep earnings steady. Over time, this growth has led to large banking groups with many smaller parts operating under different legal and control structures. These parts may appear separate on paper, but in reality, they function as an interlinked network. However, according to a 2022 article in Palgrave Macmillan titled "The regulators’ dilemma and the global banking regulation: the case of the dual financial systems," most regulatory control systems are designed around single institutions rather than these broader networks. Supervisors set capital requirements, rules for maintaining sufficient cash, and limits on lending for specific banks. These rules assume that limiting a bank's financial records will directly affect the credit supply and the stability of the financial system. That idea becomes less reliable when banks are part of a spread financial group.

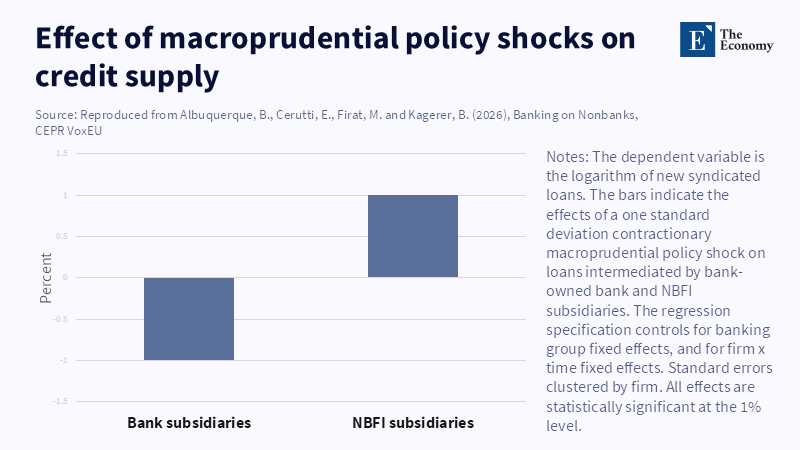

Research on loan information clearly shows this. In the syndicated loan market, tighter policies affecting banks are frequently associated with greater lending by financial institutions affiliated with the same banking groups but not with banks. So, the reduction in bank lending doesn't completely turn into a drop in total credit supply. Instead, credit activity is moved around within the group's bigger financial network.

This swap challenges the main idea behind many control tools. If financial groups can shift lending across different parts due to control changes, policies targeted at individual banks might yield weaker results than people think. The control boundary around a bank no longer captures all financial activities within the larger group.

How Banking Group Spread and the Growth of Non-Bank Financial Dealing Relate

The spread of non-bank financial institutions has strengthened this trend. In the last two decades, asset managers, investment funds, insurance companies, and other financial go-betweens that are not banks have taken on a bigger role in financial dealings. These institutions frequently perform tasks traditionally handled by banks, such as issuing credit, handling cash, and managing investments.

Reports from around the world tracking financial flows show that non-bank financial intermediaries hold a large share of global financial assets. According to these global tracking efforts, the wider financial sector, excluding banks, now holds almost half of global financial assets, indicating the rapid growth of market-based finance (Financial Stability Board, 2023). This growth has spread out the sources of credit and investment, but it has also made financial rules more complex.

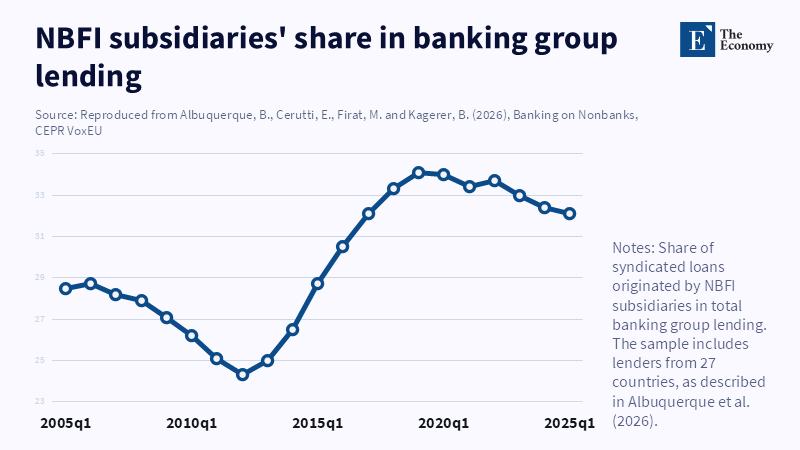

Banks and institutions that are not banks are increasingly linked together. Financial groups often run both types of institutions within the same company structure. When banks face greater regulatory pressure, financial activity can shift to related institutions that are not banks and operate under different regulatory frameworks.

Research on financial transactions shows that banks and non-bank institutions are becoming increasingly interconnected. Studies show that credit and risk transfer are increasingly occurring through networks linking banks, investment funds, and other financial go-betweens. Because of this, financial activity might cross institutional borders without leaving the larger financial group.

Information from lending markets backs up this idea. When bank lending is constrained, non-bank lenders often increase their participation in those markets, helping keep total credit supply steady. In some cases, these lenders are directly tied to banking groups whose bank parts face tighter rules.

Different ways of doing things observed in private banking also show how financial institutions adapt to these structural pressures. Research on Swiss private banks shows that institutions are expanding their operations into different areas and providing financial support to maintain earnings and remain strong in a changing global environment. This spread shows a broader trend in global finance toward geographically dispersed institutions that operate across many areas.

How Financial Networks Across Borders Affect National Power

The control challenge becomes even harder when financial groups operate in different countries. Big banks have smaller companies, branches, and related institutions in many countries. Money and credit risks move between these parts through internal money networks that connect global financial markets.

Cross-border banking activity remains a key part of the international financial system. Numbers from international banking show that cross-border bank claims remain in the tens of trillions of US dollars, indicating the scale of global financial ties. These networks link financial institutions across countries, enabling money and lending to move quickly.

In this setting, national control tools face natural limits. When regulators tighten rules at home, financial institutions might respond by moving operations to smaller companies operating in other countries. This kind of control lets financial groups continue doing business while adapting to different national control systems.

Global wealth handling gives a clear example of this. Private banks often serve clients worldwide and manage assets through networks of smaller companies across different financial centers. According to a 2025 report by KPMG and the University of St. Gallen, Swiss private banks now manage assets totaling CHF 3.4 trillion for clients worldwide, underscoring the sector’s international reach. These cross-border structures make oversight particularly challenging. While financial institutions do business around the world, the power to control mostly stays national. Because of this, no single regulator has a complete view of the entire financial group. So, risk exposures might build up across countries even when individual national regulators enforce strict rules within their own borders.

Moving Toward a Planned Way to Control Finance

To address these problems, control systems need to reflect the evolving structure of financial markets. When financial groups are spread out, actions can be moved across smaller companies and areas; control needs to look at the whole financial system rather than individual institutions.

One way is to grow control based on actions. Instead of focusing solely on institutional groups like banks or asset managers, regulators could target financial activities such as lending, using debt, and changing cash. This would reduce pressure on financial institutions to move actions across companies just to dodge control limits.

Working together around the world is just as important. Because financial groups do business across borders, effective oversight requires cooperation among national regulators. Sharing data systems, planning stress tests together, and adopting the same control standards could help authorities monitor risks across entire financial groups.

But policymakers also need to recognize the natural limits of control in a globally interconnected financial system. Money flows and new financial ideas will continue to enable institutions to expand into different countries and regions. Control can soften these trends, but it can't eliminate them. So, the realistic goal is not complete control but a closer match between control and financial structure. By recognizing the interconnectedness of modern finance, policymakers can design control systems better suited to managing risk in a globally spread financial system.

Banking Group Diversification and the Limits of National Regulation

The rise of spread banking groups has deeply changed the link between financial institutions and control. Financial groups now operate as complex networks encompassing banks, non-bank financial intermediaries, and countries. These structures make institutions stronger by spreading out, but they also weaken the effectiveness of traditional control methods.

Information from lending markets shows that tighter controls aimed at banks can cause lending to shift to related companies within the same financial groups that are not banks. At the same time, the rapid spread of finance beyond banks and across borders has created a financial system that exceeds the reach of any single national regulator.

These changes suggest that financial control needs to change. Effective oversight requires policies that cover the entire financial sector and a stronger plan among regulators across countries. Without these changes, control actions might continue to make unplanned moves in financial activities rather than truly lower risk. Having a variety has long been a basis of financial strength. But in a tied global system, it also creates new challenges for policymakers. Seeing this double role is key to planning control systems that can keep strength in modern finance.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Albuquerque, B., Cerutti, E.M., Firat, M. and Kagerer, B., 2026. Banking on Nonbanks. IMF Working Papers 2026. International Monetary Fund.

Bank for International Settlements, 2026. Statistical release: BIS international banking statistics and global liquidity indicators at end-September 2025. Bank for International Settlements.

Claessens, S., Doerr, S., Eren, E. and Gambacorta, L., 2023. The rise of non-bank financial intermediation and its implications for financial stability. BIS Bulletin. Bank for International Settlements.

Financial Stability Board, 2025a. FSB reports continued growth in nonbank financial intermediation in 2024 to $256.8 trillion. Financial Stability Board, December.

Financial Stability Board, 2025b. Global Monitoring Report on Nonbank Financial Intermediation 2025. Financial Stability Board.

Laamanen, T., Starck, T. and Kauto, J., 2025. The Effects of Diversification on Swiss Private Bank Performance. Institut für Betriebswirtschaft (IFB-HSG), University of St. Gallen.

Laamanen, T., Starck, T., Kauto, J. and Hintermann, C., 2025. Clarity on Swiss Private Banks 2025: The Effects of Diversification on Swiss Private Bank Performance. KPMG and University of St. Gallen.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.