Technology and the Future of Supply Chains: Why Critical Minerals Cooperation Matters

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

China’s rare earth dominance comes mainly from processing technology Supply disruptions often trigger innovation elsewhere Critical minerals cooperation is key for resilient supply chains

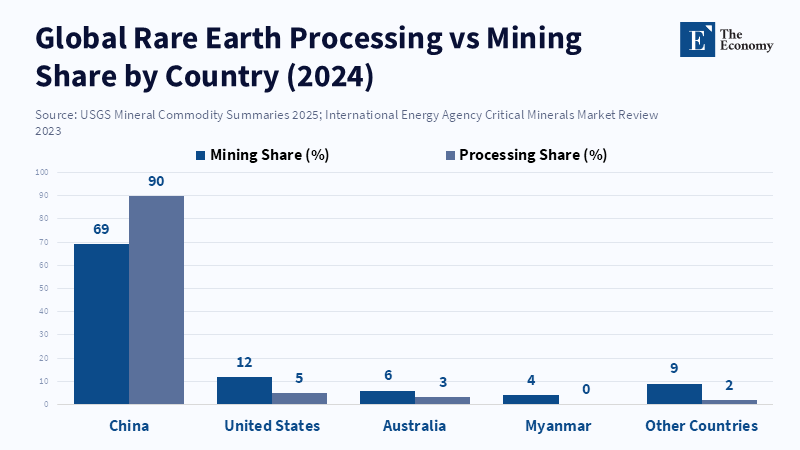

In 2024, data indicate that China accounted for close to 90% of the world's rare-earth element production, even though its raw ore production was much lower. This difference points to an important reality about today's market for critical minerals: having the raw materials isn't the same as having power in the supply chain. Instead, what really matters is technological know-how – especially in how minerals are processed, how chemicals are used to separate them, and what standards are used in manufacturing. China has become a leader in rare earths by investing for years in advanced refining methods, developing expertise, and expanding its manufacturing capabilities. Because of this, many experts believe the market is driven more by technology than by political power. But this idea may not completely appreciate an important part of how the economy works. When one country has a strong lead in a technology important to industry, other countries will start investing in alternative options. This leads to new ideas and changes in how supply chains work worldwide. So, for decision-makers, the main thing isn't just dealing with competition between countries. It's also about making sure that working together on critical minerals helps improve technology everywhere.

Working Together on Critical Minerals Beyond Just Politics

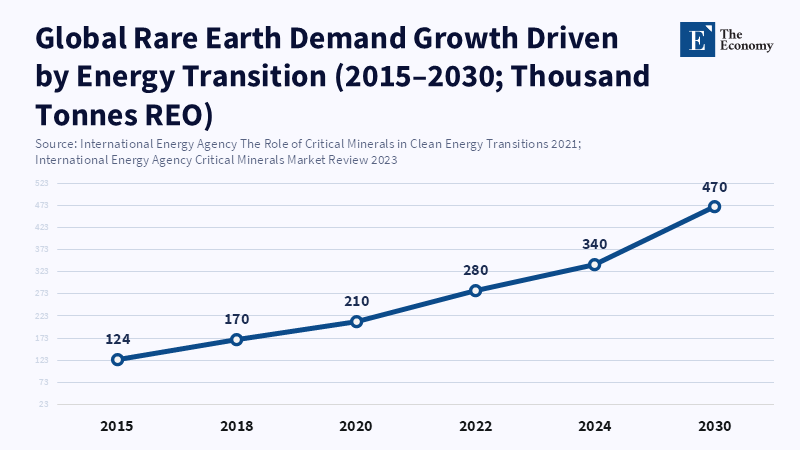

When people talk about critical minerals, it's often about competition between countries. Governments are worried about supply shortages, export restrictions, and the fact that only a few countries produce most of these minerals. These worries make sense. Rare earth elements are needed for many advanced technologies, like electric cars, wind turbines, smartphones, and defense systems. As the world's economy shifts toward more digital and clean energy technologies, demand for these materials is expected to increase significantly.

But the way the rare-earth industry is structured makes this political story more complex. China's leading role isn't just because it has the most mineral deposits. Countries such as Australia, the United States, and Brazil also contain significant amounts of rare-earth elements. Instead, China gained an advantage by building up its ability to process and separate these items on a large scale.

Processing rare earth elements is very complicated. They are often found together in mineral deposits and must be separated using chemical processes repeated many times. This requires special machines and very skilled engineers. Starting in the 1980s and 1990s, companies in China invested heavily in these technologies and formed industry clusters that worked together, connecting mines, processing plants, and magnet manufacturers.

Because of this, supply chains around the world have changed so that raw materials are mined in different places, but mostly processed in China. Even Chinese producers rely on imported concentrates from countries such as Australia and Myanmar to keep their refineries running. This shows that the rare earth industry is a complex international network, not a monopoly held by a single country.

Some specialists maintain that the main thing isn't competition between countries, but instead the ability to use technology. They say the most important thing in the market is the ability to purify and process minerals well. But leadership in technology for important industries doesn't usually last forever. As the need for these minerals grows and supply chains become politically sensitive, governments and companies invest heavily in developing new technologies. This makes the market's future structure uncertain.

Technology Leadership and the Limits of Industrial Power

China's power in the rare-earth sector extends beyond processing. It also controls the technical rules for how minerals are measured, tested, and approved for use in industry. Standards are very important in global markets because they determine how materials are evaluated and traded.

Recent developments in China's rare-earth industry show this. Industry groups have proposed standardized methods for testing many rare-earth elements. This is to make the methods for measuring and setting quality levels more official. These standards can make the industry more consistent and open. At the same time, they may strengthen existing advantages if other countries adopt the same standards.

Setting standards has been an effective instrument in industrial competition for a long time. When a country establishes widely accepted technical standards, companies around the world must change their production systems to meet them. This can make companies that already follow the standard even stronger. But strengthening technology leadership can also have unexpected effects. When companies anticipate supply problems, they often respond by investing in new ideas. The rare earth industry is a good example of this.

In the early 2010s, China imposed export restrictions, which significantly affected global supply. This prompted other countries to invest in research and development to reduce their dependence on Chinese materials. Companies and research groups began exploring new ways to separate minerals, recycle materials, and develop alternative materials. Research shows that this kind of response to find new ideas is common when supply chains are restricted. Companies increase research spending to identify substitutes and new production methods when key materials become scarce or politically restricted. Over time, these new technologies can weaken the power of dominant suppliers.

Governments have already begun responding to these incentives. The United States, the European Union, and Japan have implemented policies to enhance domestic refining capacity and support research into mineral processing technologies. These actions are meant to diversify supply chains and also develop new technical skills.

Working Together on Critical Minerals and the Response of Innovation

Even amid growing competition, a stable, long-term rare-earth market depends heavily on international cooperation. Scientific collaboration has been crucial to the development of mineral processing technologies. Universities, research centers, and industrial labs around the world have helped advance materials science and chemical engineering.

The response of innovation to supply problems underscores the importance of these research networks. Following China's export restrictions in the early 2010s, scientists began exploring new ways to reduce reliance on rare-earth elements. Researchers investigated more efficient methods for recycling electronic waste and developed alternative materials that could replace rare-earth magnets in some applications. These inventions show how technology can change supply chains. While substitutes rarely eliminate demand completely, they can reduce our reliance on certain suppliers. Over time, technological changes can shift the industry's competitive landscape.

But political tensions are now threatening the cooperative environment that supports these inventions. Export controls, concerns about national security, and limits on technology sharing have begun to curtail scientific exchange between major economies. While these policies are meant to secure sensitive technologies, they also risk slowing down research in areas that depend on international collaboration. This problem is especially important in the critical minerals sector. Many of the technological problems facing the industry—such as improving the efficiency of mineral extraction or reducing environmental harm—require diverse expertise and large-scale testing. Collaborative research programs often provide the resources needed to deal with these problems.

Strengthening cooperation on critical minerals through joint research projects could therefore be very important toward stabilizing global supply chains. By supporting international scientific partnerships, governments can encourage innovation that benefits the entire industry rather than fragmenting technological development.

Education and Research in the Future Economy of Critical Minerals

What the critical minerals market looks like in the future will depend not only on industrial policy but also on education and scientific training. Universities and research centers are key to developing the technologies that turn mineral resources into cutting-edge industrial materials. Expanding graduate education in areas such as materials science, chemical engineering, and mineral processing could greatly enhance countries' technological capabilities as they diversify their supply chains. These programs should center on collaboration across fields and on alliances with industry to ensure that research results are translated into practical technologies.

Government funding in research facilities will also be essential. Labs, pilot processing plants, and shared research platforms can speed up innovation in mineral processing and materials engineering. These investments allow scientists to test new extraction methods, recycling systems, and environmentally friendly production methods. International research partnerships are especially important here. Joint projects can bring together scientists from different countries to address complex technological challenges. Shared research programs reduce wasted effort and speed the development of new technologies.

The importance of these actions becomes clearer when we consider the future demand. The global change to clean energy will require large amounts of critical minerals for renewable energy systems and electric vehicles. Meeting this demand will require a large increase in processing ability and technological innovation. Lacking ongoing research investment, supply constraints could slow the adoption of clean energy technologies. But innovation thrives in environments where research knowledge flows freely between institutions and countries. Limiting collaboration may therefore hurt efforts to build strong supply chains.

Educational institutions, therefore, have an increasingly important role in the global economy. By training skilled scientists and engineers and supporting international research networks, they can help ensure that technology is sustained to increase global mineral production capacity.

Innovation Will Reshape the Critical Minerals Order

China's leading role in the rare earth industry stems from decades of investment in technology, not just from controlling mineral resources. Advanced processing methods, industrial standards, and specialized skills have enabled the country to become the main hub of global supply chains. These advantages are big, but they are not permanent.

History shows that supply problems and government actions often encourage innovation in other regions. Companies and research groups respond by developing new technologies, alternative materials, and better recycling systems. Over time, these innovations themselves reduce our dependence on dominant suppliers. The biggest long-term risk to global supply chains is therefore not just competition between countries. It is the splitting up of scientific collaboration that allows technology to progress. If research networks are divided by political tensions, innovation may slow, and supply problems could worsen.

Strengthening cooperation on critical minerals should therefore be a main priority for decision-makers. Investments in education, international research partnerships, and open scientific collaboration can help make sure that technology continues to increase global supply. In the end, what the future of the critical minerals economy looks like will be decided not just by geology or politics, but by how fast technology advances. If cooperation continues to support innovation, supply chains will change in ways that reduce dependence on any one country. The question for decision-makers is whether global research systems will remain collaborative enough to enable that change.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Alfaro, L., Fadinger, H., Schymik, J. & Virananda, G. (2025) Trade and Industrial Policy in Supply Chains: Directed Technological Change in Rare Earths. National Bureau of Economic Research Working Paper.

Baskaran, G. (2025) ‘China's rare earth dominance: Myanmar plays a critical role’, CNBC, 24 June.

Humphries, M. (2023) Rare Earth Elements: The Global Supply Chain. Congressional Research Service.

International Energy Agency (IEA) (2021) The Role of Critical Minerals in Clean Energy Transitions. Paris: International Energy Agency.

International Energy Agency (IEA) (2023) Critical Minerals Market Review 2023. Paris: International Energy Agency.

Investing News Network (2025) ‘Rare-earth element: top countries by reserves’, Investing News Network.

Katsaliaki, K., Galetsi, P. & Kumar, S. (2022) ‘Supply chain resilience initiatives and strategies: A systematic review’, Computers & Industrial Engineering, 170.

Mancheri, N. (2015) ‘World trade in rare earths, Chinese export restrictions, and implications’, Resources Policy, 46, pp. 262–271.

Mondo Internazionale (2025) ‘Rare Earth Elements: China’s Strategic Ace in Geopolitics’, Mondo Internazionale.

Rand, B. (2025) ‘China’s Rare Earth Restrictions Drive Innovation Abroad’, Harvard Business School Working Knowledge.

Rare Earth Exchanges (2026) ‘China Rare Earth Society Moves to Formalize Testing Standard for 15 Rare Earth Elements’, Rare Earth Exchanges.

Textor, C. (2025) ‘China: rare earths global production share 2024’, Statista.

United States Geological Survey (USGS) (2025) Mineral Commodity Summaries: Rare Earths. Reston, VA: U.S. Geological Survey.

Zhou, W. (2026) ‘China’s critical mineral strategy beyond geopolitics’, East Asia Forum.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.