NFT Fraud: How Rare Trades and Wash Trading Created the Illusion of Value in the NFT Market

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

A small number of NFT sales created the illusion of a large and valuable market Infrequent trades and wash trading inflated prices and distorted demand Most NFT collections ultimately generated little or no real value

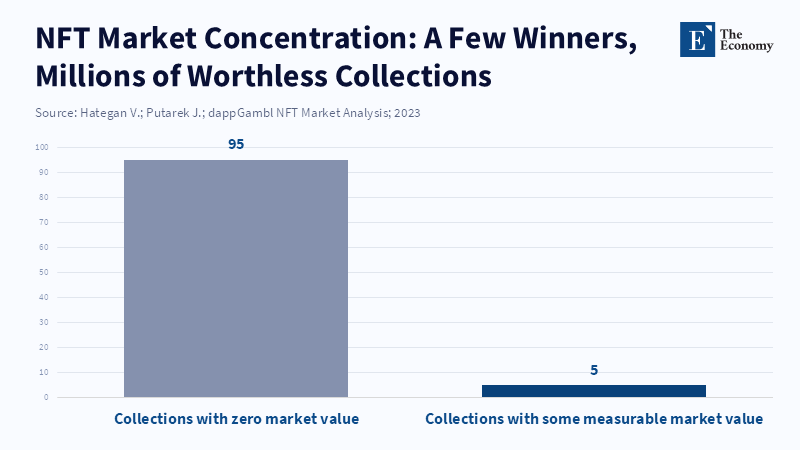

A staggering ninety-five per cent – this number alone warrants careful thought. An unbiased look at the NFT space, covering 73,257 collections, found that about 69,795 of them had essentially no financial value. This means around 23 million people are holding tokens that are practically worthless. According to a study by La Morgia and colleagues, wash trading has impacted 5.66% of all NFT collections, creating an artificial trading volume of more than $3.4 billion. To put it plainly, a small number of high-profile transactions and attention-grabbing headlines gave the false impression of a thriving, easily accessible market. The truth, however, was that the market was filled with hard-to-sell NFTs, artificially inflated sales, and market manipulation. This situation wasn't by chance. It was a predictable outcome of objects that are rarely traded, created digitally, and subjected to deliberate market tactics. To simply call this a bubble doesn't fully capture what happened. A more accurate term is NFT trickery. This refers to methods that exploited the lack of easy trading, public attention, and lax market regulations to create artificial price increases, which were then amplified by the media and market hype.

NFT Trickery and the Misleading Nature of Infrequent Trades

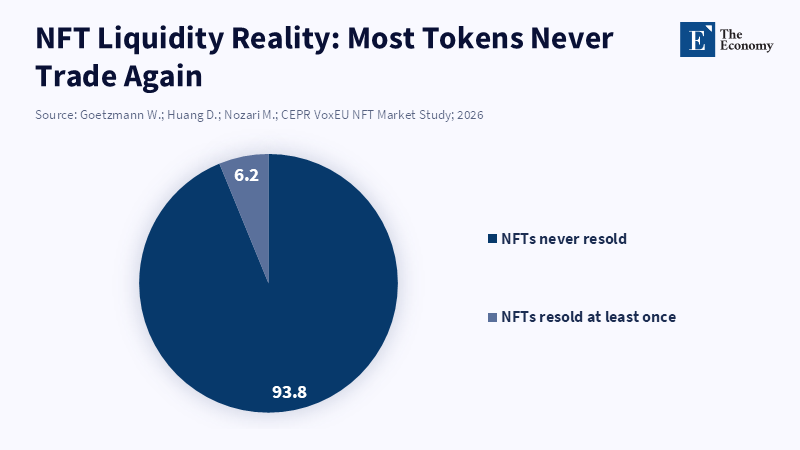

The basic strategies at play were quite simple but impactful. When a market sees little trading activity, each transaction has a disproportionate impact on price charts. When a few individuals orchestrate sales, set artificially high minimum prices, or repeatedly transfer an item between wallets they control, publicly available price data rises. Observers then mistakenly believe that these high but infrequent trades represent real market demand. In 2021, the market reached record highs, with monthly trading volumes in the billions. Yet, a closer examination shows that most tokens never left their original owners. This discrepancy creates a dangerous illusion: reported prices don't reflect a genuine interest from a wide range of buyers. Marketplaces that show minimum prices make this illusion seem permanent. People see a price on a webpage and assume it's a reliable figure. In reality, most collections show no signs of a secondary market. A small number of items account for most of the money being exchanged. These patterns change regular scarcity – which can create actual value when there's consistent demand – into artificial scarcity. This artificial scarcity collapses once the charade ends. For those teaching about market structures or how to understand the digital world, the lesson is clear: how often something is traded is just as important as its price. Price data needs to be considered in light of ease of trading, the degree of ownership concentration, and the history of who's involved in the transactions.

This lesson also applies to how we measure and judge value. If school programs use NFTs to teach about digital ownership, they should discuss prices alongside transaction counts and ownership distribution. A $100,000 sale is interesting, but looking at a broader picture shows whether it was a legitimate market activity or just a publicity stunt. In the classroom, a straightforward activity – comparing prominent sales to the percentage of items traded multiple times – can show the difference between genuine market activity and hype. For those making policy, the message is also clear: monitoring should focus on how often trades occur, how diverse the participants are, and where offers come from, rather than just on the highest prices reached. These features can be measured on public blockchains and within marketplace records. They reveal whether a price reflects independent decisions from many people or just a few staged transfers.

NFT Trickery, Fake Trading, and Artificial Scarcity

Fake trading and insider dealing were used to manufacture value. Studies examining transaction patterns have found numerous signs of circular trades, repeated buying and selling between related wallets, and trades that don't lead to any new economic ownership. Technical analysis of large, public datasets shows that these patterns are measurable, repeatable, and can sometimes be profitable for those who organize them. Market participants who have ways to coordinate and access to money were able to artificially raise minimum prices and create the appearance of competitive bidding. This led to visible price increases without creating a sustainable market. When marketplaces didn't stop these practices, they continued because they were effective. They attracted attention, made listings seem more valuable, and created stories of unique success.

This isn't just theoretical. Several studies conducted between 2022 and 2024 found that large-scale fake trading occurred and traced its effects on trading volumes and perceived profits. Audits of marketplaces and analyses by independent researchers found that much of the reported trading volume came from trades involving the same people or addresses, indicating they were working together. Regulators and risk agencies noted that NFTs were susceptible to illegal finance and scams, citing thefts, fraud, and the use of NFT transfers to hide profits. These findings should change how we teach, regulate, and design marketplaces. For teachers, the lesson needs to move from what an NFT is to how markets can be manipulated. For leaders and platform designers, the fix is both technical and procedural. They need to require analysis of where NFTs come from, show flags for fake trading, limit the number of new tokens listed until certain ownership requirements are met, and set fees that discourage trading in circles. The biggest problem here isn't that some people lost cash, which happens in other markets – it's that market rules were deliberately used to mislead people about where real demand existed.

NFT Trickery, Investor Behavior, and the Illusion of Choice

People's behavior made these problems worse. The desire to sell investments that are doing well and keep those that are doing poorly skewed the visible record of NFT profits. Owners kept tokens that had lost value and sold those that had risen in value, making it seem like winning tokens were more common than they were. This effect makes profits seem bigger than they are. In stable markets where trading happens regularly, this isn't as much of a problem. But in markets where things don't trade easily, it becomes a big issue. When you combine this with the media's focus on exceptional stories, you get a situation where staged trades create headlines, headlines attract attention, and attention brings in temporary buyers. This leads to short-term price increases that reinforce the initial false impression. This cycle turned a few successes into a myth that everyone can make money.

This way of thinking has genuine effects on governance. Lessons on finance should teach people how this effect can make profits seem larger than they actually are, using NFT data as a clear example. Leaders who manage college funds or pilot projects run on campus need to ask for more than just simple price figures. They need to ask how many times assets have been traded, how concentrated the buyers are, and how many unique wallets account for a given amount of trading. These simple checks reveal the problem and prevent people from assuming that a few lucky trades represent the market as a whole. When teachers allow students to use old NFT data for projects, they should require them to calculate adjusted rates or simulate the effect of removing the top 0.5–1% of trades on returns. These projects teach people to be critical and give them the skills to work with data that is unfair and not easily traded – skills that are useful way beyond the world of digital currency.

NFT Trickery and Policies: How to Spot It, Stop It, and Educate

Because this situation involves both technical and behavioral issues, the fix needs to be three-pronged: better methods to detect trickery, ways to prevent it, and public education. Finding trickery is doable right now. Blockchain transparency enables flagging circular trades, linked wallets, and rapid price changes that don't align with diverse buyer activity. A few academic groups have developed algorithms that can detect these signs; putting these tools into market control panels should be standard. Stopping trickery requires changes to marketplace rules, such as informing people about bulk trades, setting minimum independent-buyer limits before projects can list a minimum price, and default marketplace audits that mark suspicious patterns for buyers. Fee structures are important, as well. Marketplaces that reward turnover and top-line trading volume over real sales create the wrong motivation. Policymakers should consider simple rules requiring marketplaces to implement anti-manipulation monitoring, provide clear ways for people to report fraud, and work with law enforcement when theft or scams occur.

Education connects all of this together. Teachers should include market structure analysis in any classes that cover digital assets. This involves doing data-driven projects (not just reading): ask students to pull trading counts, calculate relationships, and simulate the effect of removing the top 0.5% of trades on returns. These skills connect class discussions to practice. For regulators, the takeaway is simple: view NFTs not as a new thing that requires heroic levels of new theory, but as a social system in which motivation, exposure, and weak rules made it easy for people to take advantage. Weak control isn't a mystery. These are problems we can solve if markets and educators demand transparency and build it.

The NFT event was more than just a strange internet thing. It was a test of how markets assign value to limited information and how people's attention can be used for cash and misdirected. When focus, manufactured trades, and rarely traded items meet weak marketplace rules, the result isn't just a rise and fall. It's a system that can be tricked into creating false value. To call this situation just a bubble doesn't tell the whole story. A better way to describe it is NFT trickery. This doesn't mean everyone was intending to commit a crime. It points to the structural and deliberate tricks that created false price signals and misled people. Teachers, leaders, and policymakers should focus on teaching the importance of trade and on fixing misaligned incentives, requiring platforms to show where creations come from and flag manipulation, and ensuring that any public use of NFTs comes with market analysis. This is how we turn a costly lesson into one that strengthens markets and protects people. According to research by von Wachter and colleagues, only 3.93 percent of addresses and 2.04 percent of NFT sale transactions in their sample showed signs of market abuse. This data should inform how we teach about NFT markets, shape marketplace design, and develop regulations to ensure genuine creative efforts are rewarded rather than manipulated activity.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Aceh, H. D. (2024) ‘The relationship between trading volume and stock price volatility in the Indonesian capital market’, Global Research in Economics and Advance Theory (GREAT) Journal, 12.

Beikzadeh, P. and Mosharraf, M. (2024) ‘Dissecting the NFT market: Implications of creation methods on trading behavior’, Ledger, 5(1).

Beikzadeh, P. and Mosharraf, M. (2024) ‘Dissecting the NFT market: Implications of creation methods on trading behavior’, Ledger, 1(1), pp. 1–15.

Bonifazi, G., Cauteruccio, F., Corradini, E., Marchetti, M., Montella, D., Scarponi, S., Ursino, D. and Virgili, L. (2023) ‘Performing wash trading on NFTs: Is the game worth the candle?’, Big Data and Cognitive Computing, 7(1).

Colavizza, G. (2022) ‘Seller–buyer networks in NFT art are driven by preferential ties’, arXiv preprint.

Easton, J. (2023) ‘95% of NFTs are now worthless, report finds’, FStech Financial Sector Technology, September.

Gao, B., Wang, Y., Wei, Q., Liu, Y., Goh, R. S. and Lo, D. (2025) ‘AiRacleX: Automated detection of price oracle manipulations via LLM-driven knowledge mining and prompt generation’, arXiv preprint.

Goetzmann, W., Huang, D. and Nozari, M. (2026) ‘The non-fungible token bubble: What investors actually earned’, VoxEU / CEPR Policy Portal.

Hategan, V. and Putarek, J. (2023) Dead NFTs: The evolving landscape of the NFT market. dappGambl Industry Report.

Khatri, Y. (2021) ‘NFT trading volume surpassed $13 billion in 2021’, The Block, December.

Korteweg, A., Kräussl, R. and Verwijmeren, P. (2016) ‘Does it pay to invest in art? A selection-corrected returns perspective’, Review of Financial Studies, 29(4), pp. 1007–1038.

Morgia, M. L., Mei, A., Mongardini, A. M. and Nemmi, E. N. (2022) ‘A game of NFTs: Characterizing NFT wash trading in the Ethereum blockchain’, arXiv preprint.

Odean, T. (1998) ‘Are investors reluctant to realize their losses?’, The Journal of Finance, 53(5), pp. 1775–1798.

U.S. Department of the Treasury (2024) Treasury releases first ever non-fungible token illicit finance risk assessment, May.

Wachter, V., Jensen, J. R., Regner, F. and Ross, O. (2022) ‘NFT wash trading: Quantifying suspicious behaviour in NFT markets’, arXiv preprint.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.