Asian Secondary Currency System: Asia’s Strategy to Reduce Dependence on the US Dollar

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

Asia needs a regional financial system to reduce dependence on the US dollar Currency baskets help institutions but not everyday transactions A practical Asian secondary currency system offers the most realistic path forward

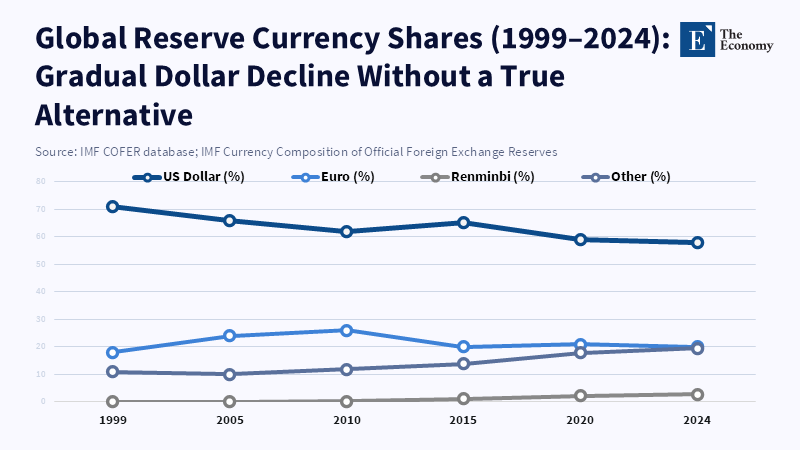

Despite the rise of other currencies, the US dollar still dominates global official reserves. At the end of 2024, central banks reported that 57.8% of allocated foreign-exchange reserves were in US dollars. Asian policymakers should note that a sudden liquidity shortage in the dollar could cause market turmoil. In such events, markets would look for stability and safety, but the euro, with less than 20% of reserves and a smaller sovereign debt market, may not suffice. The renminbi also has limited use in global payments. Asia should not try to replace the dollar with a new dominant currency. Instead, it should create a strong, practical alternative that serves businesses, households, and public services within realistic timelines. The goal is not to overthrow the dollar but to build a regional financial system that reduces financial volatility from global shocks.

Why an Asian secondary currency system matters now

The dollar's strength is firmly established in reserves, bank lending, cross-border payments, and expectations. Many contracts, invoices, and debt agreements assume the dollar will operate smoothly, making them vulnerable when the US tightens monetary policy or its sovereign market encounters stress. Recent data reinforces this point. Reserve data from the International Monetary Fund (IMF) in late 2024 showed about 58% of disclosed reserves in dollars, and surveys from the Bank for International Settlements (BIS) showed that the dollar accounted for approximately 90% of foreign exchange trades. In contrast, the euro accounts for about 20% of official reserves, and the renminbi remains under 10% for payments and under 3% in many reserve tallies. These differences represent gaps in market depth, liquidity, and global acceptance.

Given these problems, Asia can't afford to wait for a broad political agreement to reorganize global liquidity. A well-designed regional system can reduce exposure to abrupt changes in the supply and demand for safe assets, while also decreasing transaction costs for trade and investment within Asia. This approach delivers both time and reduces overall risk.

Two common suggestions have surfaced. One is a shared platform that combines existing currencies into a regional payment system and reserve pool (a collective fund created by several countries to provide support and stability to member economies). The other is to promote either the renminbi (China’s currency) or, less realistically, the euro (Europe’s single currency) as a new regional anchor currency, which means a main currency used to stabilize and facilitate trade within the region. While both ideas have potential, they also have limitations. Platforms can streamline settlement (the process of completing a financial transaction), standardise system operations, and reduce reliance on a single external currency. However, if these platforms still mainly settle in dollars, they address the route, not the fundamental vulnerability. A shift to a single currency requires deep capital-market reforms (major changes in how financial markets operate) and international trust. China's capital account (the record of financial transactions with the rest of the world) and market structures are still partially restricted to foreigners, while Europe's fragmented fiscal measures (inconsistent government spending and tax policies) and smaller bond market limit the euro's capacity to absorb sudden global demand.A third approach is an Asian secondary currency system; a regionally managed structure with multiple instruments designed for practical, everyday use, not simply as headline reserve holdings.

While a basket of currencies—a grouping of multiple national currencies weighted together—can be attractive to central bankers for smoothing valuation shocks and hedging (reducing risk), these baskets are not directly usable for common transactions. A currency basket is essentially an accounting tool that requires a trading market, liquid hedging instruments (markets or contracts that let parties protect against price moves), and widely accepted payment contracts. If a business needs to pay a supplier in basket units, the supplier must be able to easily convert those units into their local currency. This process requires deep, liquid markets in the underlying currencies and payment systems that enable instant, low-cost cross-border settlement (i.e., the completion of international payments).

Why currency baskets will not work for everyday transactions

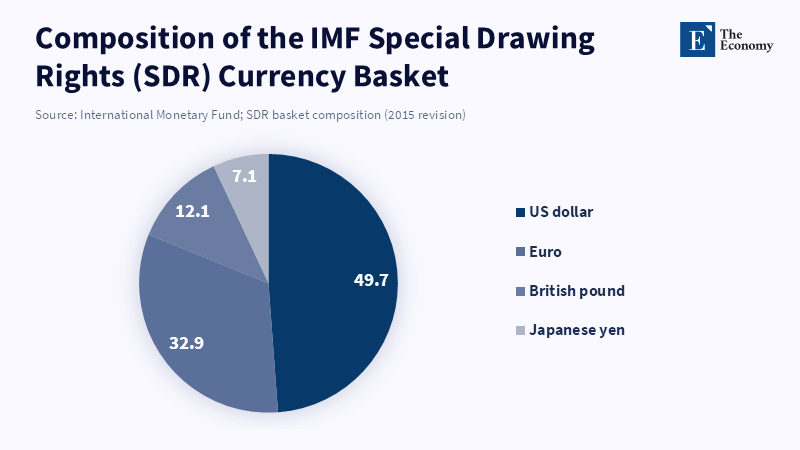

Past attempts have shown the limits of baskets. The IMF uses Special Drawing Rights (SDRs) as accounting instruments. (SDRs are an international type of monetary reserve currency created by the IMF to supplement member countries' official reserves.) BRICS (a group of major emerging economies: Brazil, Russia, India, China, and South Africa) proposals have mainly produced discussion papers and pilot platforms, not clearing systems (financial systems for settling payments) widely used by the public.

According to an IMF article, efforts to implement multi-currency systems in Asia regularly face settlement challenges and issues of political mistrust. The article suggests that for an Asian secondary currency system to be effective, practicality ought to be a key focus. It should offer real-time settlement (immediate payment completion), broad invoicing acceptance, easy conversions for small and medium-sized enterprises (SMEs—businesses with limited scale), and standardized legal provisions for cross-border contracts. It should create assets considered safe across the region, such as pooled instruments (financial assets backed by multiple parties) or regional bonds with strong credit backing, which can be used as collateral (assets pledged to secure a loan). It should also incorporate system operation via common messaging standards, shared Know Your Customer (KYC) solutions (tools for verifying identity and preventing crime) that protect privacy and comply with anti-money-laundering regulations, and readily available central bank swap lines (arrangements that allow central banks to exchange currencies).

To get the private sector to use regional tools, offer incentives such as lower settlement fees, trade finance within the regional unit, and pilot deals for major firms and payment providers. These steps turn currency baskets into real benefits for businesses and families and encourage regional liquidity.

When considering the method, official reserve shares are based on IMF COFER aggregates (2024 Q4), and market shares are based on BIS triennial FX turnover. According to the OECD, in 2025, foreign investors held 34 percent of outstanding US Treasury bonds and 26 percent of euro area bonds, while Japan’s central bank held the largest share of domestic bonds at 39 percent, which provides important context for estimating payment-system capacity and regional bond liquidity where daily data is unavailable. Final GDP and cross-border trade volumes. These estimates are approximate, focusing on orders of magnitude and policy feasibility rather than exact auction results.

To successfully build an Asian secondary currency system, initial efforts should concentrate on technical infrastructure rather than ceremonial gestures. Immediate improvements can be made through a shared settlement hub (a centralized payment processing platform) that supports multi-currency netting (offsetting obligations in multiple currencies) and instant finality (irrevocable payment completion), which can lower transaction costs and reliance on outside currencies for trade. Regulators should promote system operation for payment systems and allow payment providers to use and settle regional short-term assets on permissioned ledgers (restricted-access digital records) to increase liquidity. These measures will reduce barriers to firms accepting regional settlement and make it easier for retail use.

Building an Asian secondary currency system

According to the Basel Committee on Banking Supervision, the revised Basel Core Principles outline minimum standards for the effective regulation and oversight of banking systems and can inform how central banks might coordinate on creating secure regional instruments. While the aim is not to rival the volume of US Treasuries, developing high-quality, short-term regional bills backed by national commitments could offer reliable collateral for regional banks and payment providers. Even a modest regional bill can stabilize intra-regional money markets and reduce the need to sell into foreign sovereign paper during crises.

Next, align incentives by using public procurement rules to encourage invoicing and settlement in regional instruments for cross-border projects. Development banks and export credit agencies can offer discounts on deals using regional settlement. To motivate private banks, it is possible to ensure that verified regional bills receive good treatment in stressed scenarios. Because markets respond to incentives and rules, adoption will follow.

Any pooled instrument needs clear governance, transparency, and backing, including legally binding swap lines, transparent issuance rules, and an independent record of holdings and redemptions. The euro's success as a reserve and invoicing currency was based on strong capital markets and political arrangements, not just on policy decisions. Therefore, Asia can gradually build credible regional assets by starting with short-dated, well-governed instruments, testing them in stress scenarios, and then expanding their maturities and uses.

Such steps will face resistance on the theory that this would split global markets and hurt efficiency. There may also be concerns about geopolitics if one state dominates the project. These constitute valid concerns. The approach is to limit domination through multistate governance, rotating oversight, and technical rules that prevent unilateral freezes. Moreover, the goal is to increase resilience, not to replace the dollar. By properly designing the system, the risk of firms and households getting stuck during dollar disruptions will be reduced. It also reduces the pressure for sudden currency shifts, which could cause retaliation or division.

Asia must act decisively to develop its own robust regional currency system, drawing on lessons from the euro’s slow progress. Prioritize building market depth and institutional trust with practical tools that meet trade and reserve needs. Commit to concrete steps today, and encourage leaders, policymakers, and private-sector innovators to urgently collaborate, implement pilot programs, and accelerate adoption. By working together, Asia can create a resilient, credible financial alternative that safeguards the region against future volatility.

Asia’s path toward financial resilience

In conclusion, the data is clear: the dollar remains dominant in official reserves and foreign exchange trades. The euro is the only current second option, but it isn't large enough to meet global demand for safe, liquid assets. The renminbi has advanced but continues as a regional instrument with limited global use. Asia's best strategy entails building an Asian secondary currency system with settlement systems, short-term instruments, operational standards, and clear governance. These are technical and political problems that can be addressed through commitment, pilot projects, and reliable support.

If policymakers want to avoid future dollar shocks that force Asia into using a weak backup, they have to prioritize systems and assets that work for businesses today. A key test will be whether a trader in Jakarta can pay a supplier in Hanoi in a regional unit that settles fast and converts cheaply, and is accepted as collateral during a crisis. If the answer is no, Asia faces risks. If the answer is yes, Asia will have built a practical safeguard, which is a more secure path through the next global crisis. That is the realism needed now, and the system should be built now to allow markets to assess its value.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

European Central Bank (2025) The international role of the euro. European Central Bank.

Fund, I. M. (2024) IMF Data Brief: Currency Composition of Official Foreign Exchange Reserves. IMF Data Brief, 20 December.

Hughes, K. (2015) What is the IMF’s currency basket? World Economic Forum.

International Monetary Fund (2024) Special Drawing Rights (SDRs). International Monetary Fund.

International Monetary Fund (2024) IMF Data Brief: Currency Composition of Official Foreign Exchange Reserves. IMF Data Brief, 20 December.

Kikuchi, T. (2026) East Asia’s dollar dilemma. East Asia Forum.

Melo, F., Seal, K. and Salomao, V. (2024) 2024 Revised Basel Core Principles for Effective Banking Supervision. IMF Policy Paper No. 2024/037. International Monetary Fund.

Organisation for Economic Co-operation and Development (2026) Global Debt Report 2026. OECD Publishing.

Perez-Saiz, H. and Zhang, L. (2023) Renminbi Usage in Cross-Border Payments: Regional Patterns and the Role of Swap Lines and Offshore Clearing Banks. IMF Working Paper. International Monetary Fund.

Pistilli, M. (2026) How would a new BRICS currency affect the US dollar? Investing News Network.

Reuters (2025) Percent of global FX reserves in dollars ticks up, amounts fall, IMF data shows. Reuters.

Shirono, K. (2007) Real Effects of Common Currencies in East Asia. IMF Working Paper. International Monetary Fund.

Smith, G. (2025) Shared BRICS money: a basket currency or a basket case? Official Monetary and Financial Institutions Forum.

SWIFT (2025) RMB Tracker. Society for Worldwide Interbank Financial Telecommunication.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.