CBDC and Banking: How Central Bank Digital Currency Could Transform the Financial System

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

CBDC could redefine how money works It may shift deposits away from banks Policy design will determine its impact

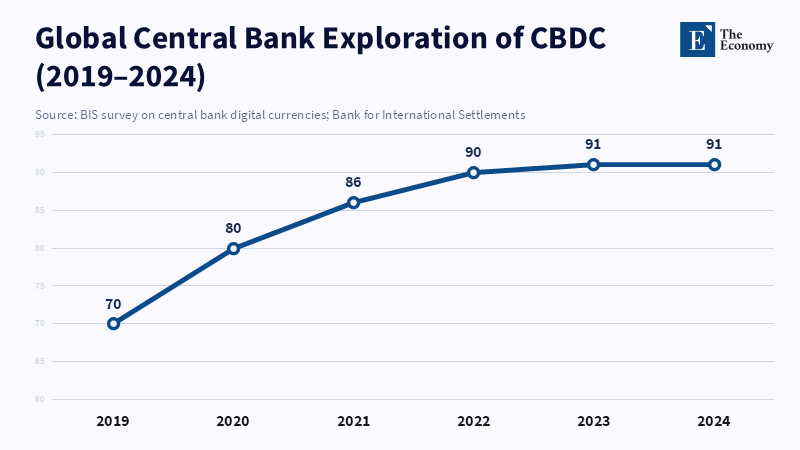

Global central banks are not just tweaking payment systems; they are fundamentally changing the very nature of money. A 2024 survey by the Bank for International Settlements revealed that 91% of the 93 central banks surveyed are thoroughly investigating a retail or wholesale central CBDC digital currency (CBDC). This number indicates a clear intention to place central-bank-issued digital money directly in the hands of individuals and companies. If this becomes widespread, the implications will go well beyond faster transactions or fewer physical coins. CBDCs could change where savings are held, how credit is provided, who profits from money creation, and which entities provide everyday financial services. This is an important topic for teachers and decision-makers. Finance, regulation, and public policy programs need to prepare citizens and institutions for a monetary system that will look and function differently from the traditional world of paper money and banks.

CBDCs and banking represent a fundamental change in the structure of the monetary system

Money has consistently served dual purposes: as a payment method and as a store of trust. With fiat money, governments became the guarantors of trust. A CBDC extends this concept to the digital sphere, turning central bank liabilities into digital units accessible in individual digital wallets. This change is fundamental. When individuals can directly hold central bank money, deposits no longer exclusively represent the public's claim on the financial system; public money becomes a retail asset. As a result, banks may face a sustained decrease in low-cost deposit funding, even in sound economic times, and an increased risk of flight to safety during crises. Research suggests two possible scenarios. First, gradual substitution, where a portion of deposits slowly shifts to CBDCs over time, reduces the deposit base and increases bank funding expenses. Second, rapid substitution, where deposits quickly move to CBDCs during periods of instability, could worsen bank runs because CBDCs are seen as a safer option than private bank deposits. These are not simply theoretical concerns. Recent scenario analyses and models have quantified the potential for deposit substitution and its subsequent effect on lending and bank profits.

The scale of this substitution is very important. Careful modeling shows that even a small, ongoing shift of deposits to CBDCs can noticeably reduce lending activity. For instance, simulations by the IMF suggest that a CBDC without interest that captures a small percentage of deposits can decrease overall lending to a measurable degree because banks will have to replace cheap deposits with more expensive funding sources, like wholesale funding or central bank borrowing. The influence is not uniform. Smaller banks that depend heavily on deposits will be most affected because they lack easy access to wholesale markets. These different effects among different bank sizes, regions, and business models require us to rethink standard banking regulations.

Also, the overall structural change depends on how the CBDC is designed. A CBDC is not a single, standardized product but rather a set of possible designs. Whether the CBDC earns interest, whether there are limits on holdings, whether wallets require a bank account, and whether central banks reinvest converted deposits back into the banking system—each of these design choices will alter the economic outcome. Design choices are policy tools and should not be considered secondary. They determine whether a CBDC remains simply a payment advancement or becomes an essential restructuring of the financial system.

Monetary history helps instructors understand the shift from gold to digital currency

History shows us that money is an institutional equilibrium. Early forms of money relied on valuable commodities, then gold guaranteed convertibility, and, after 1971, fiat money depended on collective trust and established institutions. According to the Bank for International Settlements, central national bank digital currencies (CBDCs) give the public direct access to digital money issued by a central bank, removing the credit risk associated with money provided by commercial banks or e-money issuers. For educators, this requires a fundamental shift in teaching: students need to understand money not simply as an account record but as a programmable infrastructure that is sensitive to policy decisions.

This shift requires three updates to the curriculum. First, money-creation mechanisms: instructors must teach how central bank balance sheets interact with commercial banks when deposits are converted into CBDCs. The central bank will no longer be a distant stabilizer behind commercial deposits; its balance sheet choices—asset purchases, loans to banks, collateral rules—will determine whether the system continues neutral or creates imbalances. Second, the political economy of distribution: who benefits when the government offers retail savings accounts that are safe and potentially profitable? The answer depends on policy design, and design is a political decision. Third, crisis dynamics: deposit insurance, lender-of-last-resort operations, and macroprudential tools will all be affected when retail balance sheets can move to central bank liabilities at digital speeds. Educators need to teach scenarios, not just formulas. Clear, simulation-based modules that allow students to see balance sheet shifts and policy responses will make conceptual theories understandable.

There should be an integration of the technical and public policy aspects. Addressing offline capabilities, privacy protections, and interoperability requires us to balance convenience, inclusion, and the risk of surveillance. These decisions will be made in civic and academic discussions. To prepare students for this, courses should combine cryptography, payments engineering, and normative theory. The currency of the future will require expertise in many fields.

What will happen to bank business models under CBDCs in Europe?

What happens to the bank business model when central bank money is available at retail? It depends on funding flexibility and policy design, but banks have to change from deposit reliance and consider choices that alter risk profiles. Analyses and working papers in Europe show that retail-available CBDCs could reduce banks’ deposit bases and encourage them to seek wholesale funding, sell assets, or seek assistance from the central bank. When banks rely on wholesale markets, they can obtain funding at lower rates when things are good, but experience more volatility during a crisis. For the European banking sector, where many institutions rely heavily on retail deposits, those changes could be material. The European Economy volume on CBDCs says that design features—interest rates, holding limits, conversion rules, and balance-sheet recycling—influence how serious those effects will be.

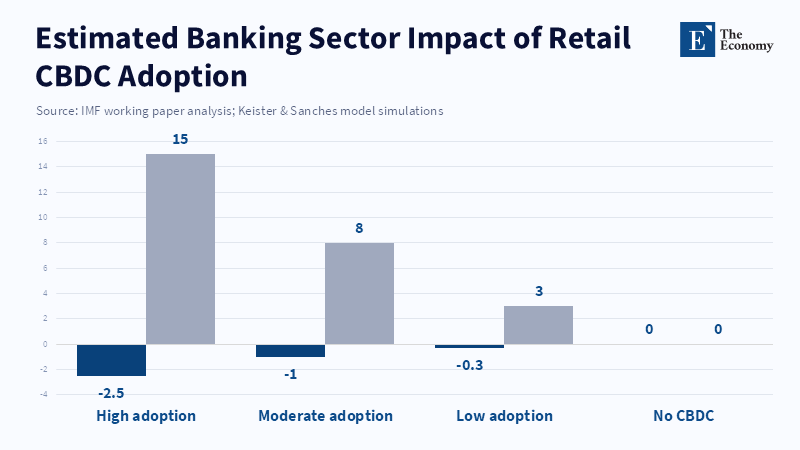

Quantitative analysis delivers useful estimates. Keister and Sanches’ conceptual framework and related studies show that a CBDC that substitutes for deposits can capture a noticeable share of deposits, reduce lending, and increase funding expenses. The IMF’s scenario analysis gives similar estimates: in one scenario without interest, a CBDC might capture around 8% of the deposit market and reduce lending by about one percentage point in model runs. These are not big numbers, but they are important for economies that strongly depend on credit and for small banks that lack easy funding channels. Policy design and central bank balance sheet management can lessen or increase these effects.

From a policymaker’s perspective, the discussion in Europe shows two lessons. First, there is no one-size-fits-all solution: regulatory structures, reserve levels, and banking systems vary across countries, so the best CBDC design will vary accordingly. Second, mitigation requires precommitment: limits on holdings, tiered interest rates, or required recycling of CBDC conversions into bank lending are helpful tools, but each has drawbacks. Limits can reduce the risk of bank runs, but they also limit the CBDC's usefulness as a universal public instrument. The European discussion is educational as it balances the social benefits of a public digital option against distribution and stability costs.

How to teach policy trade-offs and practical steps for teachers and policymakers

Educators and program designers should use CBDCs as a subject for a policy lab. Begin with simple balance-sheet simulations that allow students to adjust design choices and see their direct impact on bank liquidity ratios, lending, and central bank balance sheets. Use a small set of model scenarios—no CBDC, CBDC without interest, CBDC with interest and account limits, and fully open CBDC—to reveal the policy consequences. Pair those simulations with real-world examples: the Bahamas’ Sand Dollar, Nigeria’s eNaira, and Project mBridge experiments show how different political and technical choices perform out. These examples ground the abstract models in real results.

For decision-makers, three guidelines should be considered. First, the legal and functional status should be clear prior to the launch: new laws, anonymous or identified wallets, will define its possible designs. Second, there must be a plan for balance-sheet recycling: if widespread conversions of deposits are expected, central banks must specify how they will handle new obligations. They can purchase government bonds, increase lending to banks, or accept a smaller banking sector. Each choice has consequences for distribution and inflation. Third, regulators have to coordinate: prudential rules, deposit insurance, and macroprudential buffers must be in sync to prevent displacement effects that shift risk. These steps are not optional. They decide whether CBDCs improve society or simply shift financial fragility.

Addressing frequent criticisms strengthens the policy discussion. Critics worry that CBDCs could enable surveillance or block private innovation. While these constitute valid concerns, they are not inevitable. Privacy can be incorporated into the design, while innovation can be encouraged through compatible standards and APIs that allow private companies to build on public platforms. The more serious worry concerns financial stability: even small CBDC adoption can affect funding costs, and stress scenarios could worsen bank runs. This concern is only valid if policymakers fail to use the available design features.

A practical appeal to act

The move to a retail CBDC is not a minor update to payments; it is a possible restructuring of where public money sits and how credit is funded. The BIS survey’s 91% figure is a signal: most central banks are moving from study to tests and decisions. The period for influencing policies is now. Teachers must update curricula to teach balance-sheet mechanics, political economy, and programmable money design. Policymakers have to select designs that balance ease of use, privacy, and stability, and they must commit to recycling and coordination rules to prevent deposit substitution from harming the system. In practice, this means running pilots, merging legal reform with planning, and building classroom modules that let decision makers and industry leaders see consequences.

If we agree that money is an institutional equilibrium, then CBDC is an institutional change. We should view it as such: not as a payment feature, but as a governance decision that should have public discussion, educational attention, and clear policy commitments. The task for educators, regulators, and leaders is clear: give people the information to assess designs, ensure accountability, and make sure that money is a tool for everyone, not just markets.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Abad, J., Barrau, G.N. and Thomas, C. (2023) CBDC and the operational framework of monetary policy. BIS Working Papers No. 1126. Bank for International Settlements.

Bidder, R., Jackson, T. and Rottner, M. (2024) Will the digital euro strengthen financial stability? Yes, within certain limits. Deutsche Bundesbank Research Brief, No. 66.

Bouis, R., Gelos, G., Nakamura, F., Miettinen, P.A., Nier, E. and Soderberg, G. (2024) Central Bank Digital Currencies and Financial Stability: Balance Sheet Analysis and Policy Choices. IMF Working Paper No. 2024/226. International Monetary Fund.

Chang, H., Grinberg, F., Gornicka, L., Miccoli, M. and Tan, B.J. (2023) Central Bank Digital Currency and Bank Disintermediation in a Portfolio Choice Model. IMF Working Paper No. 2023/236. International Monetary Fund.

Fund, I.M. (2023) Central Bank Digital Currency and Bank Disintermediation in a Portfolio Choice Model. IMF Working Paper No. 2023/236. International Monetary Fund.

Fund, I.M. (2024) Central Bank Digital Currency: Progress and Further Considerations. International Monetary Fund Policy Paper.

Gentle, P.F. (2024) A famous commodity money: Gold standard in the United States. International Research Journal of Economics and Management Studies, 3, pp. 80–82.

Gross, M., Miccoli, M., Verrier, J. and Villegas-Bauer, G. (2025) Evaluating the implications of CBDC for financial stability. IMF FinTech Notes.

Niepelt, D. (2024) Central bank digital currency, the future of money, and politics. CEPR VoxEU Column.

Paul, P., Ulate, M. and Wu, J.C. (2025) A macroeconomic model of central bank digital currency. NBER Working Paper No. 33968.

UNSW Centre for Innovation and Business Law (CIBEL) (2021) The future of money: Why central bank digital currency is a game changer.

European Economy (2024) CBDC: Issues and prospects. European Economy Discussion Papers.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.