Inflation Expectations and the Euro Area Phillips Curve: Why Expectations Now Drive Inflation Dynamics

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

Inflation expectations now shape inflation more than traditional economic slack Regional evidence in Europe shows that household and firm beliefs strongly influence price dynamics Effective monetary policy must manage expectations, not just interest rates

Inflation expectations serve as the mechanism through which current price levels determine future economic behavior. When individuals and establishments anticipate rising costs, they adapt accordingly: establishments may increase their prices, employees may negotiate for higher wages, and individuals may modify their spending habits or secure loans earlier. This mechanism is important, as short-term expectations spiked during the economic turbulence of 2021-2023 and have only gradually decreased. According to the European Central Bank (ECB)'s micro-survey, the average consumer’s one-year inflation expectation stood at 2.5% in October 2024, after a pronounced rise in 2023. Meanwhile, experts predict a return to around 2% headline inflation in the medium term (with average figures from the Survey of Professional Forecasters (SPF) at 2.4% for 2024 and 1.9% for 2025-2026). These expert predictions exist alongside a wide range of views held by individuals and establishments. In practical terms, current inflation appears to be less a direct consequence of capacity and more a balanced outcome resulting from the interactions among expectations among many economic participants. If central banks and financial planners view expectations as only a secondary factor rather than a primary element, they might misjudge the extent to which demand management can, in reality, alter costs.

Inflation Expectations: Revisiting the Phillips Curve in a Diverse Monetary Union

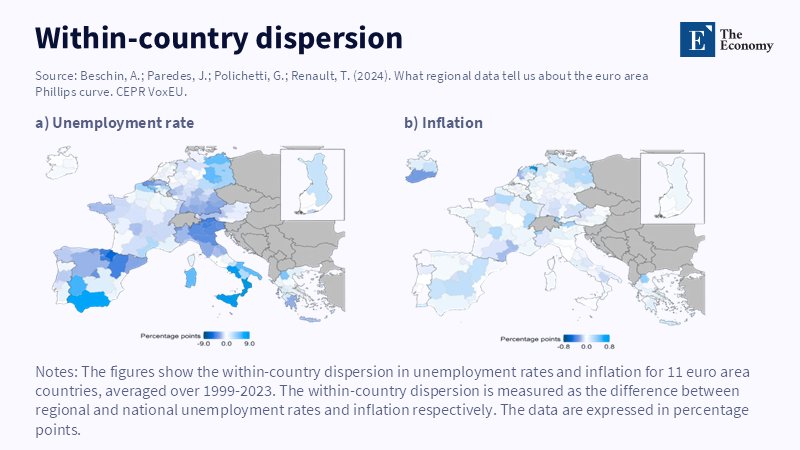

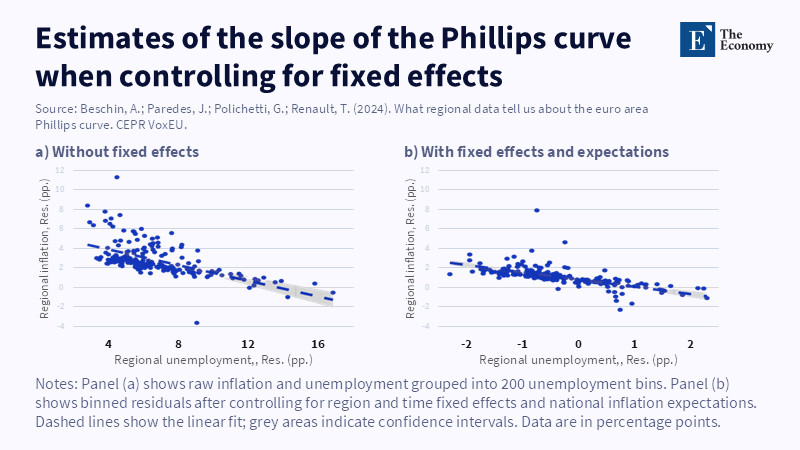

The typical interpretation of the Phillips curve suggests a simple relationship between unemployment and inflation. In reality, this connection varies. Examination of regional data within the euro area reveals details that challenge this standard understanding. First, there are significant differences in inflation and unemployment rates across countries; regional data show distinct histories regarding economic impacts, demand composition, and information availability. According to a 2022 analysis published by Intereconomics, researchers found that general inflation expectations strongly influence how regions in the euro area respond to inflation, beyond local economic elements. The study notes that when these broader expectations are taken into account, the measured influence of local conditions on regional inflation decreases substantially.t regional analysis) and might even approach zero when considering country-specific changes across time. Essentially, much of what seems like a ‘Phillips effect’ at the regional level disappears once we consider what people expect inflation to be.

Why is this relevant now? Recent years have seen significant, noticeable cost increases that individuals and businesses have experienced firsthand. Direct experiences determine how beliefs are formed. Data show that individuals heavily consider their recent inflation experiences when forming short-term expectations. In contrast, establishments and managers use available details and projections to update their views and then change prices accordingly. In a monetary union as diverse as the euro area, shared financial strategies may not perfectly offset differences in government fiscal situations, employment regulations, or media coverage that shapes expectations across regions. Logically, the central bank’s standard method — adjusting interest rates to manage overall demand — has a secondary influence that can either amplify or attenuate the intended impact. Overlooking this secondary influence is akin to a surgeon using a blunt instrument when a precise tool is needed.

This changed thinking points out why regional evidence varies from national aggregate data. National aggregate data averages out regional diversity, possibly obscuring the transmission of beliefs. At a regional level, diversity is visible in both the distribution of expectations and the flow of influence from expectations to actions. This variety underscores the constraints of uniform, counter-cyclical policies and explains why dependable control of expectations — over periods relevant to wages, establishment pricing, and individual agreements — becomes the main policy goal alongside general targeting.

Inflation Expectations in the Data: Evidence and Quantifiable Effects

Substantial, varied, and reliable data support the importance of expectations. Central bank surveys indicate that expectations among individuals and establishments shifted noticeably during the latest inflation period, exhibiting significant continuity and diversity. The ECB’s Consumer Anticipations Survey indicates that average perceived inflation decreased from its peak in September 2023 (8.4%) to considerably smaller figures by October 2024, and one-year expectations stabilized near 2.5% in late 2024. Supporting this individual-level evidence, the ECB’s expanded establishment survey (SAFE) finds that establishments revise their plans for costs, pay, and work based on projections: a 1% increase in establishments’ inflation expectations leads to about a 0.3% planned rise in prices, according to the survey. This is a relevant relationship: beliefs change real pricing plans, which then affect measured inflation.

Experts occupy a separate place in the evidence. The ECB’s Survey of Professional Forecasters recorded general expectations of about 2.4% for 2024 and 1.9% for 2025–26 in late-2024 reports, indicating confidence in eventual deflation, even though individuals and establishments showed greater variation in their predictions. The concurrence of steady, expert views and more unstable individual/establishment views is important because each type of expectation influences different areas — financial markets and long-term contracts on one side, and spending and pricing decisions on the other. The International Monetary Fund (IMF)'s analysis has noted that long-term expectations are important to sustain faith, but short-term expectations from individuals and establishments strongly predict short-term inflation outcomes and can alter the impact of strategies.

Inflation Expectations and Policy: Recommendations

If expectations are key, then these recommendations follow. First, the collection of expectation measurements should be seen as a shared resource. Governments and educators have to prioritize understanding inflation, not as an isolated theory but as a common idea that shapes contracts, financial choices, and budgets. Central banks and statistical organizations have improved survey infrastructure (for example, the ECB’s CES and SAFE sections); academic institutions should integrate clear descriptions of survey results into money planning so that local bodies can use the same information that experts use.

Second, communicate clearly and with local awareness. Establishing trust requires consistent messages that reach different groups in different ways, not just press conferences. The SAFE results show how forward-looking details can continuously change establishment plans. Central banks and financial authorities should customize communication tactics — including regional updates and alliances with local businesses — to counter disruptive signals from the media that might heighten private expectations.

Third, adjust demand management to the expectation climate. If the influence of economic conditions diminishes once expectations are taken into account, then forceful rate increases to reduce demand may yield diminishing results and cause unnecessary difficulties. According to a recent IMF report, policymakers ought to weigh the use of strengthened communication and targeted actions such as pay guidelines, indexing reforms, and temporary assistance for vulnerable groups, as these measures may help handle inflation expectations with fewer trade-offs. The IMF highlights that expanding policy tools does not replace the need for interest rate moves, but rather, such measures should complement rate changes to better shape expectations.

Instructors in universities and educational programs should redesign curricula. They should teach students how expectation surveys are conducted, how to read regional data, and how broad communication affects economic behavior. According to research by D’Acunto, Hoang, and Weber, providing local officers with means to manage and communicate expectations can help guide economic decisions and boost financial planning during periods of expectation-driven instability.

Inflation Expectations: Potential Critiques and Rebuttals

“Surveys are unreliable; we should trust market measurements.” Rebuttal: Surveys do contain inaccuracies, but they capture how spending and pricing decisions unfold. Market results reflect financial markets’ views; experts capture informed consensus. Surveys record consumer and pricing reactions.

“Expectations will decrease; no action is needed.” Rebuttal: Expectations do respond, but they react differently to experiences. Individuals grow concerned as inflation rises, but they may be resistant to reductions. Survey data suggest that views on past inflation strongly influence short-term expectations, particularly among lower-income individuals, which can delay the return to normal without policy action.

“Regional discoveries are a statistical coincidence; policy should remain focused at the national level.” Rebuttal: Broad data hides diversity. Regional work indicates that once country-level expectations dynamics are taken into account, links between the local situation and inflation decrease. This is an important change to policy thinking: it may alter the projected cost of reducing inflation.

Across these rebuttals, the message is that measuring and managing expectations are central to understanding how policy affects decisions.

In conclusion, inflation expectations matter. They are how price shocks turn into reality. Local survey data has turned that from a thought into a proven fact: people form opinions that influence prices; experts may stabilize long-run views, but personal views push prices; and the influence of economic conditions diminishes once expectations are taken into account. For educational staff, the lesson is clear: incorporate understanding of expectations into programs. For authorities, the lesson is this — keep the policy rate ready, but also put money into information and actions that mold views. That approach is the best way to price stability without excess cost.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Adrian, T., 2023. The role of inflation expectations in monetary policy. International Monetary Fund.

Baumann, U., Ferrando, A., Georgarakos, D., Gorodnichenko, Y. and Reinelt, T., 2024. How euro area firms’ inflation expectations affect their business decisions. European Central Bank Working Paper Series.

Baumann, U., Ferrando, A., Georgarakos, D., Gorodnichenko, Y. and Reinelt, T., 2025. Firms’ inflation expectations in a monetary union. Federal Reserve Bank of San Francisco Working Paper No. 2025-29.

Beschin, A., Paredes, J., Polichetti, G. and Renault, T., 2026. What regional data tell us about the euro area Phillips curve. ECB Research Bulletin No. 140.

Blot, C., Bozou, C. and Creel, J., 2022. Inflation expectations in the euro area: trends and policy considerations. European Parliament Think Tank.

Burban, V. and Guilloux-Nefussi, S., 2025. The anchoring of inflation expectations in the euro area. Banque de France.

European Central Bank, 2024. ECB Consumer Expectations Survey results – June 2024. European Central Bank.

International Monetary Fund, 2023. Monetary policy and inflation. In: Monetary Policy in the New Normal, Chapter 18.

Intereconomics, 2022. Determinants of inflation expectations in the euro area. Intereconomics, 57(2), pp. 85–92.

European Central Bank, 2022. Inflation expectations and monetary policy in the euro area. European Central Bank.

Economic Modelling, 2021. Unconventional monetary policy and inflation expectations in the euro area. Economic Modelling, 102, p. 105564.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.