Beyond Rare Earths: What the Hormuz Helium Shock Reveals About the Critical Minerals Supply Chain

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

Supply chain risk goes far beyond rare earths Hormuz now matters for tech inputs, not just energy Resilience needs diversification and better risk mapping

In 2024, the Strait of Hormuz facilitated over one-quarter of global seaborne oil trade and approximately one-fifth of worldwide liquefied natural gas (LNG) trade. A wider audience soon realized that this same corridor can also limit the flow of helium, a gas often linked with balloons but vital for manufacturing semiconductors, medical imaging, and the broader digital economy. According to an OECD report, disruptions in a few key regions can quickly unsettle semiconductor supply and affect many other sectors, underscoring that the critical minerals supply chain has become a central issue in energy security. Public discourse has long oversimplified supply vulnerabilities by focusing on a single narrative—that China’s dominance in rare earth elements necessitates diversification away from it. While this remains valid, it is insufficient. The underlying challenge is in the complex network of narrow logistical channels, processing hubs, and specialized inputs upon which modern industry depends. A disruption originating in a single location can propagate far beyond the initial product, making headlines. Therefore, comprehending the critical minerals supply chain requires regarding it as an interconnected network rather than a mere inventory of materials.

Beyond Rare Earths: The Hidden Chokepoints

Recent events in the Strait of Hormuz make it clear that addressing rare-earth supply concerns in isolation is insufficient. According to an analysis by the International Energy Agency, upcoming export controls by China on lithium-ion batteries could also put pressure on global supply chains, exposing the broader vulnerabilities in critical mineral markets. um production is closely linked with other energy systems using shared infrastructure and security conditions. Scientific American noted that the closure of this passage trapped roughly one-third of global commercial helium. According to a report from the Global Energy Prize, preliminary estimates from the US Geological Service indicate that in 2023, Qatar and Russia together were responsible for over 80 percent of the growth in global helium production, increasing their output by a combined 10 million cubic meters. Although these figures differ slightly, the strategic implication remains stable: helium, often viewed as marginal, becomes critical when transportation is interrupted. According to a 2025 report on rare earth supply chains, vulnerabilities in critical mineral supply often stem from factors such as geographic concentration, logistical obstacles, and other challenges.

This highlights that commodities like helium, which also play an essential role in markets such as cryogenics and semiconductors and for which substitutes are limited, can create crucial supply bottlenecks, calling into question the notion that supply risk is unique to rare earth elements. The earlier narrative—wherein China’s concentration of mining and processing posed the main risk—fails to capture the full complexity. The Hormuz incident exposes additional vulnerabilities: shipping routes, processing facilities, and interconnected industries likewise contribute to systemic risk. Since helium is a byproduct of natural gas processing, energy shocks can rapidly translate into disruptions within semiconductor supply chains. Analogous dynamics occur throughout the system; disruptions to shipping lanes, water access, refining capacity, or export licensing may curtail supply well before mine closures occur. The U.S. Energy Information Administration reports that, through 2024 and into early 2025, traffic through Hormuz accounted for more than one-quarter of global seaborne oil trade and around one-fifth of LNG trade, much of it destined for Asia. The efficiencies accrued through free trade have linked these parts tightly, but this interconnection also creates vulnerabilities where a narrow geographic corridor can affect critical infrastructure, such as semiconductor fabrication plants, hospitals, educational institutions, and cloud services located far downstream.

Measuring Supply Chain Stress: Tools and Their Limits

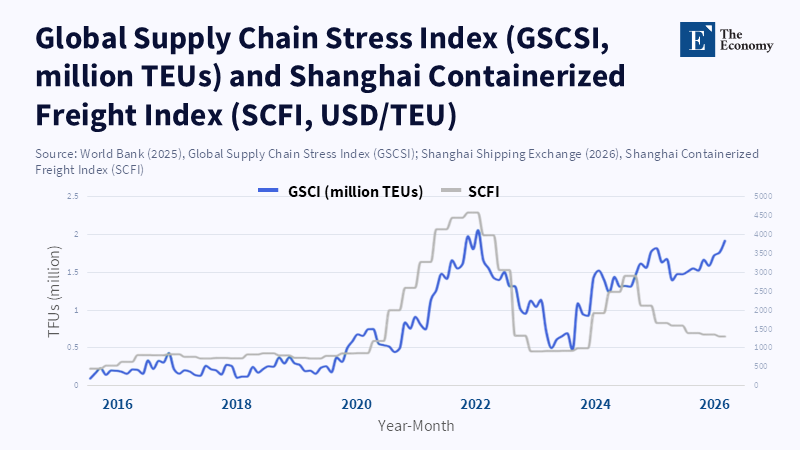

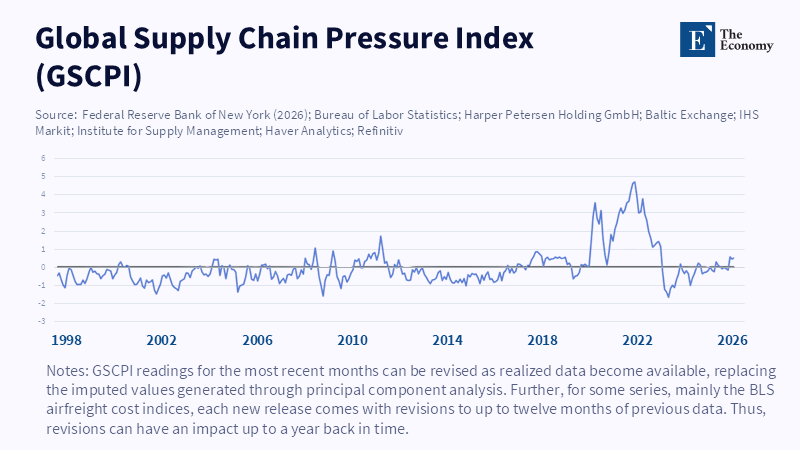

As a consequence, policy approaches must move beyond merely enumerating critical materials. Mere identification of critical inputs is inadequate if risk monitoring employs overly broad or delayed metrics. The World Bank’s Global Supply Chain Stress Index and the New York Federal Reserve’s Global Supply Chain Pressure Index exemplify progress alongside limitations. The World Bank’s index focuses on maritime disruptions by tracking container delays measured in TEUs, while the New York Fed’s index integrates transportation costs and manufacturing indicators to assess systemic pressures. These measures capture different facets of supply chain status: one highlights physical shipping bottlenecks, while the other indicates broader economic stress costs and delivery challenges. When combined judiciously, they offer a more comprehensive picture; when misinterpreted, they risk fostering complacency.

Divergences between these metrics observed in 2024 and 2025 illustrate this point. The Richmond Federal Reserve analysis noted that the World Bank’s measure indicated stress comparable to levels seen in 2021–22, whereas the New York Fed’s metric appeared near-normal. This discrepancy should not be read as a contradiction but rather as a warning signal: physical disturbances and price pressures are not always synchronous. Shipping networks may remain constrained even as inflationary signals moderate. The International Monetary Fund’s study on the Red Sea bottleneck reinforces this, showing that in early 2024, trade through the Suez Canal dropped by 50 percent year-over-year, while trade through the Panama Canal declined by 32 percent. Firms rerouted shipments, costs increased, and delays lengthened, but these conditions didn’t immediately manifest in headline economic data. Thus, an apparently subdued macroeconomic signal does not necessarily indicate a healthy critical minerals supply chain; instead, it may reflect that disruptions have yet to propagate to retail prices or official production statistics.

The 2025 OECD Supply Chain Resilience Review builds on this argument, cautioning that broad sectoral models can obscure the specific products most critical during crises, including semiconductors and minerals essential to strategic technologies. Aggregating raw materials across broad industrial categories tends to produce an overly optimistic view of substitutability. This opacity contributes to policymaker surprise: while “chemicals” or “electronics” may appear generally vulnerable, it remains unclear which specific materials, magnetic elements, or processing stages will trigger production halts. Research by the European Central Bank offers a more nuanced framework, characterizing critical dependencies as strategically important inputs with limited import diversification, scarce supply, and minimal domestic capacity. This product-level perspective is more in line with current governmental requirements, reflecting the increasing complexity of the critical minerals supply chain that cannot be adequately addressed by broad averages or political slogans.

Rethinking Concentration Risk Beyond China

The emphasis on China’s role, while still relevant, represents an incomplete analysis. According to the International Energy Agency’s Global Critical Minerals Outlook 2025, the mining sector may see gradual diversification for certain materials, but refining processes remain highly concentrated. Projections for 2035 suggest China could continue supplying over 60 percent of refined lithium and cobalt, as well as approximately 80 percent of battery-grade graphite and rare earth elements. These concentrations constitute significant strategic risks; nonetheless, they are not the sole source of vulnerability. The European Commission’s Critical Raw Materials Act is noteworthy precisely because it frames resilience beyond China-centric concerns, establishing a benchmark whereby, by 2030, no more than 65 percent of any strategic raw material’s annual requirements at any relevant processing stage derive from a single non-EU country. This portfolio approach recognizes that excessive dependence on any single source—be it China, Qatar, the Democratic Republic of Congo, Indonesia, or a particular shipping route—can create strategic fragility.

Hence, policy should pursue diversification tempered by realism. Complete self-sufficiency is largely unaffordable for most economies, and full decoupling could incur its own costs. Analysis by the European Central Bank suggests that the economic burden of comprehensive geopolitical decoupling would likely exceed that of critical dependencies, without effectively eliminating risk. Similarly, IMF research indicates that strategically diversifying targeted upstream imports can enhance resilience and overall welfare, especially under scenarios with heightened risk of substantial trade shocks, despite associated efficiency losses. This balance favors neither isolation nor complacency; instead, it calls for deliberate redundancy, manifesting in dual sourcing, stockpiling of inputs difficult to substitute, increased recycling, greater transparency regarding refining infrastructure, and strengthened cooperation through allied procurement partnerships. Thus, resilience should not be construed as antithetical to trade, but rather as a different configuration of trade relationships.

Furthermore, conceptualizing supply risks solely through a monopoly framework is inadequate. Many risks originate within oligopolies, chokepoints along transportation routes, or critical nodes identified in network analysis as single points of failure. The European Central Bank’s findings show that critical dependencies can generate disproportionate losses even when they constitute only a minor fraction of total intermediate inputs. In the United States, inputs designated as critical dependencies represent a small share of production inputs, yet an abrupt disruption could have far greater effects due to their irreplaceability and centrality to downstream manufacturing. Consequently, policy attention frequently overlooks these inputs because of their limited trade volume, yet their strategic importance arises precisely from their scale and specialization, which complicate substitution under duress. In this light, the critical minerals supply chain is vulnerable at its narrowest juncture rather than its broadest.

Building Intellectual Resilience Through Education

This analysis is particularly relevant to education policy, which must address an emerging gap in intellectual resilience ahead of industrial challenges. According to a recent article by Kegenbekov, Alipova, and Jackson, current educational systems often treat trade policy, engineering, and technology governance as separate fields, thereby limiting their connections to critical minerals and supply chain challenges. The authors note that this compartmentalized approach no longer matches today’s economic realities, highlighting the need for greater integration across these disciplines. For instance, students studying artificial intelligence without a grounding in upstream supply dependencies receive only a partial understanding of the ecosystem. Similarly, public administrators procuring technological goods or infrastructure without awareness of upstream vulnerabilities operate with limited insight. The European Union’s policy frameworks, such as the Critical Raw Materials Act, underscore this by linking supply security to research, innovation, and skills development through initiatives such as skills partnerships and the Raw Materials Academy. While labor markets increasingly recognize supply security as an essential capability, education systems are still adapting.

In practical terms, this necessitates training students to trace products across extraction, processing, transport, and end use. They should learn to interpret different analytical tools—for example, comparing the World Bank’s Global Supply Chain Stress Index and the New York Fed’s Global Supply Chain Pressure Index—to discern their respective insights and limitations. Future policymakers must be equipped to pose critical questions, such as which inputs defy substitution, which actors dominate refining rather than extraction, and which ports or maritime routes serve as intermediaries between mines and factories. According to research by Abramo, D'Angelo, and Di Costa, universities are positioned to collaborate with industry based on factors like their size, location, and research quality. While educational institutions may not directly set industrial policy, they play an important role in shaping the expertise of analysts, engineers, civil servants, and procurement officers. For this reason, universities, hospitals, technical schools, and educational networks should consider initiating their own mapping of dependencies on essential technologies to enable early identification of bottlenecks. Persisting with an oversimplified narrative centered exclusively on China’s rare earth supply risks perpetuates reactive policy postures.

Historically characterized primarily as an oil chokepoint, the Strait of Hormuz has seen recent disruptions that reveal this characterization is insufficient. The Strait influences the critical minerals supply chain by shaping major shipping routes and affecting the operation of refineries and the production of specialized materials, aspects that are sometimes overlooked in public discussion. According to the USGS, even small disruptions to global production of materials like copper can occur due to external risks such as natural disasters, highlighting the broader vulnerabilities that extend beyond the more visible effects of supply shocks to commodities like helium. Future supply shocks may arise from materials such as graphite, nickel sulfate, gallium, or obscure processing stages unfamiliar to most stakeholders. Consequently, policymakers should expand their focus beyond mining locations to encompass refining capacity, shipping logistics, insurance frameworks, key transit routes, and potential failure points within the network. Education systems should parallel this expanded focus. Nations capable of comprehensively mapping dependencies prior to crises will not eliminate risk but will reduce the likelihood of surprise, constituting a critical benchmark of economic maturity.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Ahn, J. and Tan, B.J. (2025) ‘Supply chain diversification and resilience’, IMF Working Papers, 2025(102). Washington, DC: International Monetary Fund.

Arvis, J.-F., Rodrigue, J.-P., Ulybina, D. and Rastogi, C. (2026) ‘A metric of global maritime supply chain disruptions: The global supply chain stress index - maritime (GSCSI-M)’, Journal of Transport Geography, 131, 104575.

Attinasi, M.-G., Boeckelmann, L., Gerinovics, R. and Meunier, B. (2025) ‘Unveiling the hidden costs of critical dependencies’, ECB Economic Bulletin, 5/2025.

Baker, T. (2026) ‘The AI boom’s hidden weakness: how Iran’s conflict exposed a helium bottleneck for chip manufacturing’, Silicon Canals.

Béchard, D.E. (2026) ‘The AI boom is dangerously dependent on helium’, Scientific American.

Benigno, G., di Giovanni, J., Groen, J.J.J. and Noble, A.I. (2022) ‘The GSCPI: A new barometer of global supply chain pressures’, Federal Reserve Bank of New York Staff Reports, No. 1017.

Berthou, A., Haramboure, A. and Samek, L. (2024) ‘Mapping and testing product-level vulnerabilities in granular production networks’, OECD Science, Technology and Industry Working Papers, No. 2024/02. Paris: OECD Publishing.

European Commission, Directorate-General for Internal Market, Industry, Entrepreneurship and SMEs (2023) European Critical Raw Materials Act. Brussels: European Commission.

Essers, D., Lebastard, L., Mancini, M., Panon, L. and Timini, J. (2025) ‘Critical input disruptions – mapping out the road to EU resilience’, ECB Research Bulletin, No. 128.

Federal Reserve Bank of New York (2026) Global Supply Chain Pressure Index (GSCPI). New York, NY: Federal Reserve Bank of New York.

Global Energy Association (2024) ‘Qatar to become a new leader in the helium market’, Global Energy Association.

Gulley, A.L. (2024) ‘The development of China’s monopoly over cobalt battery materials’, Mineral Economics, 37(3), pp. 619–631.

International Energy Agency (2025) Global Critical Minerals Outlook 2025. Paris: International Energy Agency.

Jaiswal, K.S., Luco, N., Schnebele, E.K., Nassar, N.T. and Otarod, D. (2024) Quantitative Risk of Earthquake Disruption to Global Copper and Rhenium Supply. U.S. Geological Survey Open-File Report 2024–1028. Reston, VA: U.S. Geological Survey.

Kamali, P., Koepke, R., Sozzi, A. and Verschuur, J. (2024) ‘Red Sea attacks disrupt global trade’, IMF Blog, 7 March.

Le Monde (2026) ‘Closure of Strait of Hormuz is “greatest global energy security threat in history,” warns IEA chief’.

Mathews, A. (2025) ‘Strait of Hormuz accounted for one-fifth of global LNG trade flows in 2024’, OilMonster.

Nassar, N.T., Shojaeddini, E., Alonso, E., Jaskula, B. and Tolcin, A. (2024) Quantifying Potential Effects of China’s Gallium and Germanium Export Restrictions on the U.S. Economy. U.S. Geological Survey Open-File Report 2024–1057. Reston, VA: U.S. Geological Survey.

Neal, A.W. (2026) ‘After Nord Stream: four security dilemmas in critical maritime infrastructure protection’, International Affairs, 102(1), pp. 207–225.

OECD (2023) OECD Skills Outlook 2023: Skills for a Resilient Green and Digital Transition. Paris: OECD Publishing.

OECD (2024) Mapping and Testing Product-Level Vulnerabilities in Granular Production Networks. Paris: OECD Publishing.

OECD (2025) OECD Supply Chain Resilience Review. Paris: OECD Publishing.

OECD (2026) Semiconductors. Paris: OECD.

O’Trakoun, J. (2025) ‘How constrained are global supply chains?’, Macro Minute, Federal Reserve Bank of Richmond, 20 May.

QatarEnergy LNG (n.d.) Ras Laffan Helium. Doha: QatarEnergy LNG.

Rooks, T. (2026) ‘Iran war triggers helium shortage, hits semiconductor supply’, Deutsche Welle.

Shanghai Shipping Exchange (2026) Shanghai Containerized Freight Index (SCFI). Shanghai: Shanghai Shipping Exchange.

U.S. Energy Information Administration (2025) ‘Amid regional conflict, the Strait of Hormuz remains critical oil chokepoint’, Today in Energy, 16 June.

U.S. Geological Survey (2024) ‘USGS critical minerals study: bans on gallium and germanium exports could cost the U.S. billions’, U.S. Geological Survey News Release, 19 November.

U.S. Geological Survey (2025) ‘Helium’, in Mineral Commodity Summaries 2025. Reston, VA: U.S. Geological Survey.

World Bank (2025) Global Supply Chain Stress Index. Washington, DC: World Bank.

Zhang, H. (2025) ‘Resilience of critical transition minerals supply chain in the context of strategic rivalry: implications for the national policy and regulatory frameworks’, Journal of Energy & Natural Resources Law, pp. 1–27.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.