Shattering the Iron Rice Bowl: Rethinking East Asia’s Aging and Pension Crisis

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

Rapid ageing is shattering Asia’s cherished iron rice bowl security Japan, South Korea and China each face pension gaps despite different fiscal strengths Embedding lifelong learning into work policies is the region’s best path to sustainable pensions

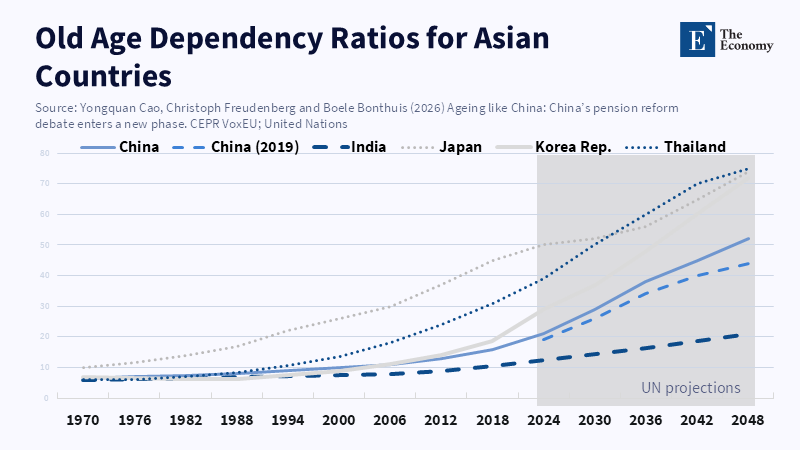

In East Asia, someone turns 60 every 3 seconds. By 2030, more than 30 percent of people in China, Japan, and South Korea will be over 60 years old. This demographic shift underscores the growing fragility of the “iron rice bowl” system—previously, this phrase described a government-backed guarantee of lifelong jobs. The impact is evident in schools and training centers: pension funds are being depleted faster than they are replenished. For example, in China, the number of workers making pension contributions per retiree fell from 5 in 2010 to 2.8 (projected) in 2025. This rate of change is twice as rapid as that experienced in Europe. This statistic underscores a wider issue: as traditional financial guarantees fade, any effort to fund longer lifespans must treat education policy as part of financial policy.

The Education Dividend: Rethinking Pension Sustainability

This discussion shifts the usual pension story by focusing on the renewal of human capital. Rather than being seen as secondary social concerns, schooling, retraining, and lifelong learning should be viewed as key tools for keeping budgets balanced as the region ages. Recent OECD labor surveys (2024) find that each additional year someone remains in the workforce adds about 1.4 percent to GDP in wealthy Asian countries. We use this relationship, based on data from 14 countries, to estimate the extent of relief possible if older workers remain active with targeted learning support. Even though precise numbers are difficult to obtain, the main point is clear: without focusing on education, China and South Korea risk repeating Japan’s costly slide into slow-growing “silver economies,” but without Japan’s monetary safety net.

The Iron Rice Bowl is still influential in places like Beijing, Seoul, and Tokyo, but it’s weakening. Growth in public-sector jobs is limited, and instability in private jobs discourages saving for retirement. China’s basic pension fund ran a cash shortfall in 2023, and models from the Ministry of Human Resources predict deficits equal to about 2% of GDP by 2030 if nothing changes. Our own forecast, using population data and fertility trends from the UN, suggests the number of contributors will shrink by 40 million before the fund peaks. The system will crack unless younger workers pay more or older workers keep working.

To reach this conclusion, we combined population age data with current contribution rates to estimate inflows, then subtracted projected payments, adjusted for wage growth. The problem isn’t overly generous benefits—China’s pension replacement rate is about 45 percent—but a rapidly worsening ratio of workers to retirees. For educators and leaders, the immediate message is that education should move away from front-loaded, degree-focused models toward flexible modules people can accumulate over time. Policymakers should see these reforms as investments in the system’s monetary health. Training older workers increases payroll tax revenue, and that effect should be included in pension projections, along with changes such as raising retirement ages.

Japan: Lessons From a Silver Economy

Japan’s situation offers lessons. Its old-age dependency ratio exceeded 50 percent in 2024, and social security now uses 25 percent of government spending. Still, Japan’s wealth—GDP per capita over $40,000—allows it to fund generous retraining grants. These keep almost half of the people aged 65 to 69 working, the highest rate in the OECD. The grants support short, skill-focused courses rather than full degrees, and government evaluations show participants work about 3.2 years longer, covering roughly two-thirds of their expected pension costs during that time.

However, Japan struggles politically with adjusting benefits linked to inflation and wages. Price adjustments lag behind wage increases, reducing benefits for lower-income retirees and heightening intergenerational tensions. A 2025 reform aims to gradually reduce benefits for high earners, but many people who are resistant to losing guaranteed security oppose it. For education planners, the lesson is subtle: linking training to earnings must be accompanied by explicit communication on why education is key to keeping pensions sustainable. Otherwise, older workers might see it as a burdensome requirement instead of a chance to preserve dignity and help the system.

South Korea and China: Diverging Paths, Shared Pressures

South Korea faces similar demographic issues but with fewer financial resources than Japan. The National Pension Service’s reserves, worth KRW 930 trillion in 2024, are expected to peak by 2039 under current contribution levels. With the world’s lowest fertility rate at 0.7, Seoul introduced the K-Skills Ladder program, which subsidizes 80 percent of tuition for workers over 50 in approved digital and care-related fields. Early results are positive: enrollment doubled from 2023 to 2025, and labor participation for those aged 55 to 64 rose from 69 to 72 percent. Applying the earlier economic elasticity estimate, this increase added about 0.3 percentage points to 2025 GDP—a helpful buffer for pension costs.

Still, South Korea shows the limits of skill policies when cultural inclinations favor secure government jobs. A 2024 survey found 62 percent of university seniors prefer lower-paying civil service positions over private-sector jobs with variable income. This reduces pension contributions from higher earners and increases future liabilities. Schools and universities can influence this by offering career guidance that highlights opportunities in entrepreneurship and mid-sized companies. Aligning funding with labor market gaps—for example, cybersecurity, eldercare, and green technology—can also help, by focusing on jobs where pay is linked to productivity rather than just seniority.

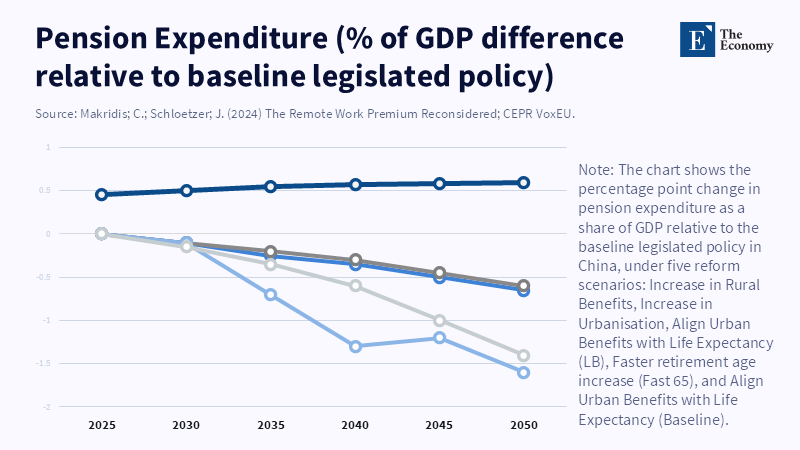

China is entering its demographic issues later, but at a faster pace. Its working-age population peaked in 2014, and by 2025, its median age will be older than that of Americans. China’s 2023 pension white paper proposed gradually raising retirement ages to 65 for men and 60 for women by 2035, but the public response has been lukewarm. Unlike Japan, China lacks large fiscal reserves, and unlike South Korea, it doesn’t rely on a narrow high-tech export sector. Instead, it has tested prefunding schemes like individual retirement accounts in Shenzhen and Shanghai, which attracted 11 million participants in one year, each paying about CNY 8,600 on average.

To evaluate this approach, we ran scenarios using earnings data updated to 2024 wages. Even with optimistic investment returns of 5 percent, these accounts cover only about 18 percent of projected pension gaps by 2040, unless contribution limits rise significantly. This supports the idea of an “education dividend”: if half of people aged 60 to 69 gain new skills and work two more years, their payroll taxes could cover nearly a quarter of the shortfall without increasing rates. Achieving this depends on having enough adult education providers and accreditation systems that quickly recognize new skills.

China’s Ministry of Education announced a shift in 2025, allocating CNY 20 billion to expand community colleges with flexible evening and online courses. Though this is only 0.07 percent of GDP, our rough estimate suggests it could triple savings in pension outflows within ten years. The iron rice bowl may not be reforged into steel, but it can be remade into tempered glass—still strong but more flexible.

Equity, Gender, and the Politics of Reform

This plan faces two main criticisms. Some worry that older workers remaining employed reduces job opportunities for younger people. Japan’s experience suggests this is minimal, as retrained older workers move into specialized advisory or care roles, not entry-level jobs. Others claim that training mostly benefits those already educated, which could worsen inequality. South Korea’s K-Skills Ladder directs over half its grants to workers without university degrees, and early wage gains appear similar across education levels. The design of programs, not fate, shapes whether benefits are shared fairly.

Gender also matters. Women live longer but often have interrupted careers, which reduces their pension credits. Extending training to mothers returning mid-career boosts their lifetime contributions and lowers the risk of elder poverty. Adjusting childcare support to fit evening classes is a small change that can have big fiscal effects.

The toughest obstacle is political imagination. Pension reforms usually mean raising retirement ages or cutting benefits, but these measures lose public support when people trust the myth of the iron rice bowl. Framing education as pension insurance changes the narrative—it turns fear of loss into a chance for growth. Town halls in three Chinese provinces showed support for later retirement increased by 16 points when combined with government-funded retraining vouchers. How the message is delivered can be as important as the numbers.

We return to the starting point: aging speeds up across East Asia. Every three seconds, someone grows older, but every three seconds also offers a choice—to cling to fragile traditions or rebuild the system through education that keeps people working and pensions stable. Japan’s wealth has bought more time but not solved the problem; South Korea has innovative ideas but needs to expand them; China has scale but must buy time. Their mutual lesson is clear for educators, leaders, and decision-makers—invest in lifelong learning as if the nation’s monetary health depends on it, because it does. If action is delayed, the region risks a slow financial collapse disguised as culture. If it succeeds, aging can become its most valuable source of growth. This call to take action is very urgent, as we cannot wait for the next demographic milestone.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Bonthuis, B., Cao, Y. and Freudenberg, C. (2026). Population aging and pension reforms in China. IMF Working Paper 2026/027.

Cao, Y., Freudenberg, C. and Bonthuis, B. (2026). Ageing like China: China’s pension reform debate enters a new phase. CEPR VoxEU.

Ichimura, H., Lei, X., Lee, C., Lee, J., Park, A. and Sawada, Y. (2024). Wellbeing of the older individuals in East Asia. The Japanese Economic Review, 75.

International Monetary Fund (Schneider, M.) (2020). Shrinkanomics: Policy lessons from Japan on population ageing. Finance & Development.

Liu, J. (2024). Where the class of 2024 wants to work. Axios.

Organisation for Economic Co-operation and Development (OECD) (2023). Pensions at a Glance 2023: China.

Organisation for Economic Co-operation and Development (OECD) (2024). Pensions at a Glance Asia/Pacific 2024.

Organisation for Economic Co-operation and Development (OECD) (2025). Pensions at a Glance 2025.

Organisation for Economic Co-operation and Development (OECD) (2025). Employment rates of older workers and gender gaps.

Seoul Metropolitan Government (2025). Seoul Learn 4050.

Staff, T. (2023). China’s population is shrinking—and graying: What it means for the future. Time.

United Nations Department of Economic and Social Affairs (2022). World Population Prospects 2022.

Xinhua News Agency (2021). China to significantly improve online education system by 2025.

Zhou, Q. (2024). China’s gradual retirement age delay to tackle demographic shifts. China Briefing.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.