Gold Is Rising, but the US Dollar Reserve Currency Still Has Time

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

Gold is rising, but the dollar still anchors the system Reserve currencies change only when power shifts run deep Today’s trend is diversification, not real displacement

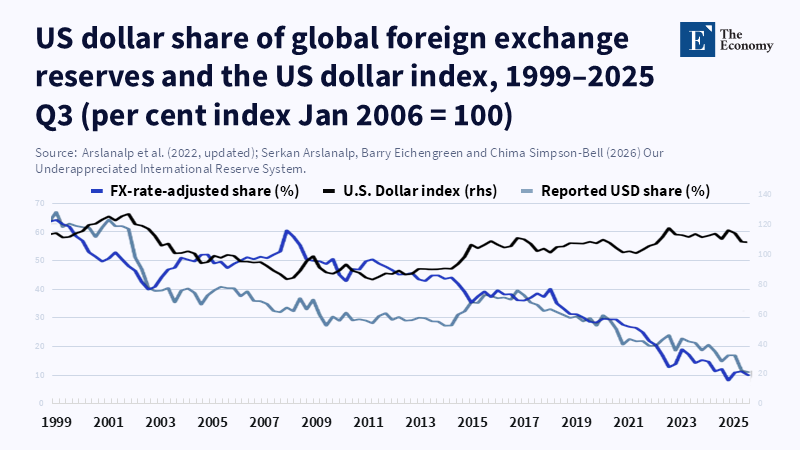

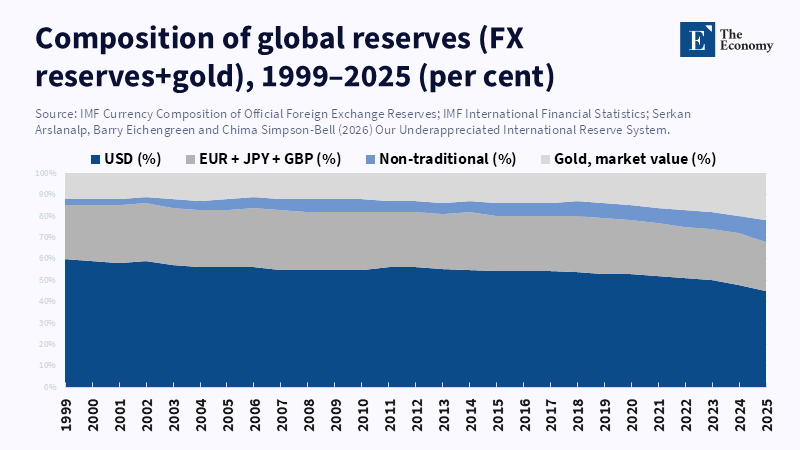

The US dollar’s role as the main global reserve currency is weakening at the edges but remains strong at its core. This distinction is important. According to the Federal Reserve's 2025 report, the U.S. dollar comprised about 58 percent of globally reported foreign exchange reserves in 2024. The report also notes that, measured at market prices, gold made up around 20 percent of total official reserves as central banks increased their gold purchases and benefited from rising gold prices. Some interpret these numbers as evidence that the world is quickly moving toward a system without the dollar at its center. That interpretation goes too far. Reserve currency frameworks do not shift simply because one asset gains or another loses ground. They change when elements such as economic size, military power, legal confidence, market depth, payment infrastructure, and crisis management all move together. That is a much bigger change. Gold’s rise is real, and there is a slow trend away from a concentrated reserve system. But neither fact means that the US dollar is close to a historic collapse.

Gold as a Hedge, Not a Replacement

Much of the current debate treats reserve currency status as if it were just about investment choices. The argument goes: if central banks buy less US debt and more gold, the dollar’s dominance must be ending. This view is too simplistic. Gold is not replacing the dollar like the dollar once replaced sterling. Unlike a currency, gold has no issuer backing it, no fiscal support, no payment system, and no last-resort lender. It acts as a hedge, not a full monetary system. Central banks buy gold because it is less exposed to sanctions risk, retains value in times of disorder, and helps diversify portfolios when interest rates, conflicts, and politics are uncertain. These reasons are important, but they don’t add up to a new monetary order. Instead, they reflect caution. So the recent increase in gold mainly signals a search for insurance rather than the rise of a successor to the dollar.

It’s important to look closely at reserve composition data. According to the International Monetary Fund, gold accounted for 18.3 percent of total official reserves in 2024, rather than the often-cited 20 percent figure. But looking at disclosed foreign exchange reserves alone, the dollar remained far ahead at about 58%, with the euro around 20% and China’s renminbi roughly 2%. These details matter because they separate a story about valuation and risk management from one about currency replacement. For teachers and policymakers, this distinction is vital. Public discussion often blurs the issue, leading people to mistakenly believe the dollar is losing its throne simply because gold ranks second among reserve assets. A clearer lesson is that reserve systems can diversify without losing their main anchor. A hedge can grow without becoming the central currency.

Lessons from History: How Reserve Currencies Actually Change

History also suggests that reserve currency changes happen only with considerable stress. The US became the world’s largest economy well before the dollar fully dominated the postwar system. Monetary leadership didn’t shift neatly or quickly from sterling to the dollar. Research shows the dollar surpassed sterling in central bank reserves by the mid-1920s, earlier than previously thought, but that wasn’t the final shift. Sterling regained ground in the 1930s due to imperial ties, political alliances, and the structure of the sterling area. This shows that reserve leadership depends on more than economic output — it also involves commercial relationships, access to financial markets, political groups, and the issuing country's reach.

This earlier transition is often misunderstood. It didn’t happen because investors suddenly preferred the dollar. Instead, it unfolded through war, depression, debt crises, imperial decline, capital controls, and eventually a new postwar order centered on American power. In other words, reserve hierarchy changes when political and economic power shift together, usually under conditions of severe stress. Today, the US still offers the deepest pool of safe assets, the largest and most liquid government bond market, a wide military reach, and key legal and financial institutions vital to international contracts. These foundations have not vanished. Without a major war between powers, a collapse in US state capacity, or a rival system with comparable trust and depth, the dollar is likely to decline slowly rather than collapse suddenly.

The Dollar’s Enduring Role in Global Transactions

The case for caution grows stronger when we compare reserve data to actual currency usage. Although the dollar’s share of reserves has declined over the past two decades, it remains dominant in global transactions. The Federal Reserve’s 2025 review shows the dollar’s wide international use has changed little in the last five years. The Bank for International Settlements reports that the dollar accounted for nearly 90% of foreign exchange transactions in 2022, making it the dominant currency in global markets. The same Fed review indicates the dollar dominates trade invoicing well beyond the US share of world trade, especially in the Americas and much of Asia-Pacific. These network effects are what matter. Reserve managers hold dollars not because they admire Washington, but because firms invoice, banks fund, commodities price, and crises demand liquidity in dollars.

That is why gold’s rise should be seen as a warning to the US rather than a countdown to dollar collapse. Central banks appear to want more protection against geopolitical fragmentation. This is important, especially for countries concerned about sanctions or changes to US policy. But a signal is different from a new system. Gold cannot finance trade credit, manage trillions in routine reserve management, such as US Treasury securities, or underpin global private contracts. Even the renminbi, often called a potential rival, still lacks sufficient openness, convertibility, and institutional trust to replace the dollar broadly. According to a recent report from the IMF, the euro’s share of global foreign exchange reserves increased to 21.13 percent in the second quarter of 2025, largely due to valuation effects, while the dollar’s share remained steady; the euro continues to play an important but stable role among reserve currencies. The world is diversifying slightly but not replacing the dollar at the center.

Policy and Education Implications

In economic education and public policy, the key task is to teach reserve-currency politics as institutional and historical, not as driven by headlines. Too often, commentators treat every gold purchase, sanction episode, or BRICS statement as proof that a new monetary era has arrived. This encourages drama over greater understanding. Universities and policy schools ought to focus on helping students distinguish between reserve composition, currency use in transactions, invoicing power, and supply of safe assets. These are connected yet different aspects of the system. With that framework, the current situation becomes clearer: the system is less concentrated, and hedging is more visible, but the dollar market still forms the core. Economics courses should include more financial history, political economy, and institutional analysis so that students grasp how monetary power persists and evolves.

For policymakers, the message is similar. US officials shouldn’t ignore the rise of gold, since it reflects genuine concerns about fragmentation and sanctions risk. But others should not base policy on the assumption that the dollar will soon be replaced. Europe will have to build deeper capital markets and supply more common safe assets before the euro can move beyond its steady second place. China will need far greater legal openness, policy stability, and foreign investor faith before the renminbi can mount a broad challenge. Emerging economies will continue to diversify, but most will still manage crises within a dollar-centered system. Some critics could argue this outlook is too cautious, especially given the repeated use of financial sanctions and worries about US debt. Yet recent evidence points to incremental adaptation rather than a radical shift. The world seems to be moving toward a more hedged reserve mix, not a post-dollar monetary order.

Those who predict the dollar’s decline frequently argue that reserve erosion feeds on itself. This is true in theory: if enough central banks, firms, and investors move together, network effects can reverse. But that tipping point is much higher than many realize. It does not require just dissatisfaction with the current system but confidence in a full replacement. It needs more than another store of value; it demands another system for collateral, payments, borrowing, trade settlement, and emergency liquidity. According to a recent A&S Communications report, no system currently exists that can use gold at the scale needed to replace the US dollar, and experts say gold's rising value is more a sign of global uncertainty than of its ability to take on the dollar's complex role in international trade and finance. A reserve system can become more fragmented without losing its main currency. We should avoid mistaking a thicker hedge for a new leader.

The main policy takeaway is this: the future of the US dollar as the primary reserve currency will not be decided by one chart showing gold outpacing the euro, a few quarters of diversification, or the desire of some countries to reduce US exposure. It will depend on whether the foundations of American power weaken simultaneously and whether another bloc can deliver a full alternative system. History shows the transitions are rare, slow, and linked to major upheavals. Until such a moment arrives, the more prudent interpretation holds. The rise of gold deserves attention, and dollar pessimism justifies careful examination, but the burden of proof lies with those claiming that an asset without an issuer and a world without a clear successor can end the dollar’s era. They cannot. This is the more difficult but realistic lesson that students, officials, and financial commentators need now. The immediate challenge is not to predict a dramatic collapse that may never happen, but to understand the real conditions that must be met before reserve diversification becomes displacement. This question is important for classrooms, governments, and central banks alike.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Arslanalp, S., Eichengreen, B. and Simpson-Bell, C. (2024) ‘Dollar dominance in the international reserve system: An update’, IMF Blog, 11 June.

Arslanalp, S., Eichengreen, B. and Simpson-Bell, C. (2026) ‘Our underappreciated international reserve system’, VoxEU, 21 March.

Bacalu, V., Fleuriet, V. and Qureshi, A. (2017) ‘Two things that keep central banks’ reserve managers awake at night’, IMF Blog, 29 March.

Bertaut, C., von Beschwitz, B. and Curcuru, S. (2025) ‘The international role of the U.S. dollar – 2025 edition’, FEDS Notes. Washington, DC: Board of Governors of the Federal Reserve System, 18 July.

Bolhuis, M., Roy, A., Schneider, P. and Zhang, Z. (2025) ‘Good policies (and good luck) helped emerging economies better resist shocks’, IMF Blog, 6 October.

Drummond, I.M. (1981) ‘Introduction: The sterling area in the 1930s’, in The Floating Pound and the Sterling Area, 1931–1939. Cambridge: Cambridge University Press, pp. 1–27.

Eichengreen, B. and Flandreau, M. (2009) ‘The rise and fall of the dollar, or when did the dollar replace sterling as the leading reserve currency?’, European Review of Economic History, 13(3), pp. 377–411.

Financial Stability Board (2022) Liquidity in Core Government Bond Markets. Basel: Financial Stability Board.

Karlstroem, B.S. (1967) ‘How did they become reserve currencies?’, Finance & Development, 4(3), pp. 209–217.

Lagarde, C. (2025) ‘Earning influence: lessons from the history of international currencies’, speech at the Jacques Delors Centre at Hertie School, Berlin, 26 May.

Mora, C.E. and Nor, T.M. (2015) Reserve Currency Blocs: A Changing International Monetary System? IMF Working Paper No. 15/3. Washington, DC: International Monetary Fund.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.