CBDC Neutrality and the Next Digital Safety Net

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

CBDC neutrality feeds outgoing funds straight back to banks, keeping the system calm Automatic, wide-access backstops can avert SVB-style stampedes in sovereign digital money We must lock neutrality into courses, drills, and law before the next flash run arrives

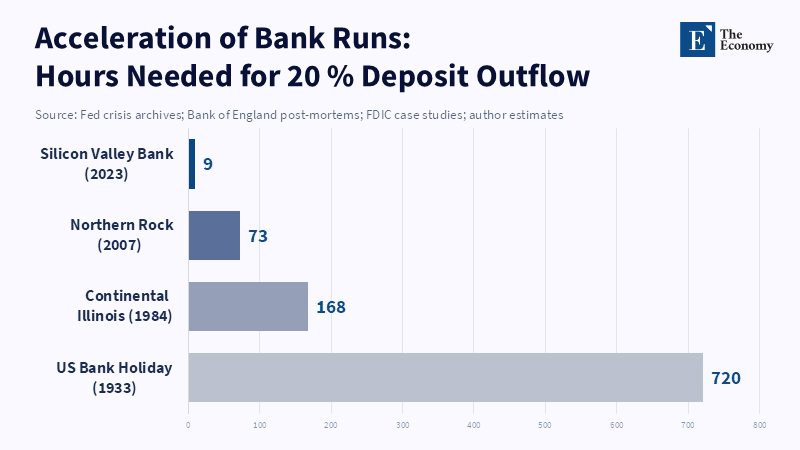

On March 9, 2023, Silicon Valley Bank lost about $42 billion of its deposits—roughly a quarter of its total—in just nine hours of trading. The following morning, before regulators intervened, it faced another potential loss of 62 percent. This event revealed two main points. First, digital money can drain even well-funded banks extremely fast. Second, confidence can disappear in minutes without an immediate stabilizing force. As central bank digital currencies (CBDCs) shift from theory to practice, the question isn’t whether a similar rush could happen in digital sovereign money, but how to prevent it. The crux lies in the idea of CBDC neutrality—the principle that any liquidity CBDCs take from banks must be returned promptly by the central bank on terms similar to those of its usual emergency lending. If done properly, digital finance can be as stable as traditional systems; if not, a panic triggered by quick digital withdrawals could disrupt lending to the real economy before regulators can respond.

The Case for CBDC Neutrality

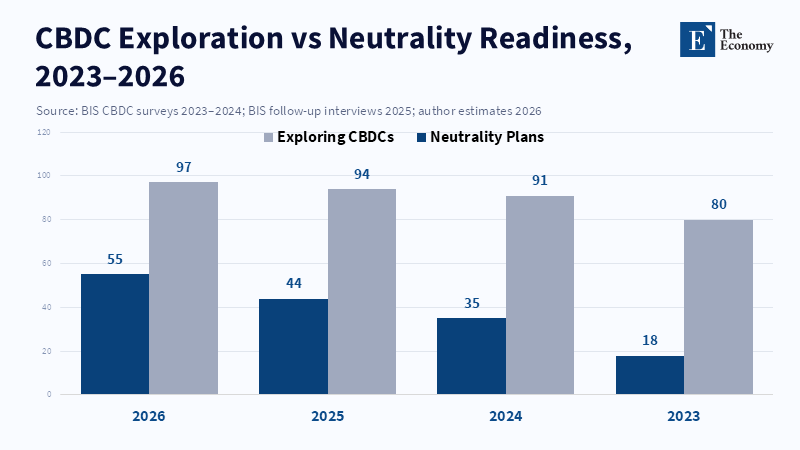

CBDC neutrality isn’t simply a technical detail; it’s central to preserving trust. Each unit of digital currency issued by the central bank may replace an equal amount of bank deposits. This shift doesn’t cause problems if the central bank simultaneously provides liquidity to banks through tools like standing facilities or term funding, on terms comparable to or better than those available in wholesale markets. A 2024 survey of 93 monetary authorities found that 91% were exploring CBDCs. According to a report from the Bank for International Settlements, central banks are progressing with their digital currency initiatives at their own chosen pace, adopting varied strategies and exploring different design options.

Why does this readiness gap matter? Liquidity deficits don’t just increase steadily—they worsen sharply after a certain point. According to a 2025 article from the Bank for International Settlements, introducing a retail central bank digital currency (CBDC) could reduce financial soundness because it provides a storage option at scale, making rapid transfers from banks to CBDC accounts more attractive during periods of stress, possibly exacerbating withdrawals and increasing risks to the banking sector. When people exchange bank deposits for CBDCs, banks automatically receive funding from the central bank to maintain stable reserves. According to a recent report from the International Monetary Fund, a system could be implemented in which banks receive CBDC balances during the day at little or no penalty, with these credits being reversed as payment flows return to normal. The authors emphasize that a clear understanding of such digital backstops should be included in money and banking courses so that people are well informed rather than apprehensive about these developments.

There’s also a fairness aspect. Without neutrality, large banks get wholesale funding first, while smaller or regional banks must limit lending or sell assets, worsening inequalities. A clear rule linking liquidity support directly to CBDC inflows prevents this disequilibrium. For those managing local payment systems, the message is sharp: unless outflows are matched by equal injections, a local digital currency may actually increase financial exclusion rather than reduce it.

Speed, Panic, and the Digital Run

The Silicon Valley Bank collapse offers a harsh lesson in speed. Earlier runs took days, but mobile banking cut this to hours. Instant payment systems and social media shortened decision times. Within 36 hours of the first warning, 85 percent of uninsured deposits were withdrawn or lined up for withdrawal. Regulators guaranteed deposits to stop the crisis, but bond losses had already spread risks widely.

CBDCs speed things up even more. According to an article by Todd Keister and Cyril Monnet, a well-designed central financial digital currency (CBDC) may actually reduce, rather than increase, financial fragility, challenging the idea that instant settlement and full transparency necessarily make digital deposits more prone to herd behavior. But design matters. Measures like limiting transaction speeds, charging higher fees for large transfers, and requiring identity checks can slow panics without blocking normal activity. Most importantly, neutrality reassures banks. Knowing liquidity flows back as fast as it leaves helps banks avoid forced asset sales and keeps customers calm.

Stress tests now reflect these lessons. According to the Federal Reserve Board, the 2023 bank stress test scenarios were released to assess whether large banks could continue to lend to households and businesses even during a severe recession. Such updated scenarios should be part of risk management teaching, and regulators need to build real-time dashboards tracking CBDC migration. According to the Financial Soundness Institute of the Bank for International Settlements, new dashboards would display overall financial flows while keeping individual banks' data confidential to avoid stigma.

Stablecoins and the Liquidity Gap

Private stablecoins bring another challenge. According to Chainalysis's Global Crypto Adoption Index 2023, while the report covers how cryptocurrencies are being adopted worldwide, it does not provide details on stablecoin transaction volumes or specific growth rates. This structure splits custody, blurs accountability, and invites regulatory omissions. When markets are stressed, users may abandon unstable coins in favor of a CBDC’s apparent security. Without neutrality, the central bank would drain liquidity from commercial banks at peak risk moments.

Some believe stablecoin users understand risks well. That confidence was shaken in May 2025, when two major multi-issuer stablecoins lost their pegs for two days. According to a 2022 article on systemic liquidity risks and synthetic central monetary authority digital currencies, over $12 billion was queued for redemption, and spreads between redemption and secondary market prices increased sixfold, indicating a significant real-world test of the risks associated with CBDC substitution. According to the European Central Bank, euro area banks have limited the pass-through of policy rates to overnight depositors, resulting in a shift toward term deposits.

Regulators should link stablecoin liquidity rules to CBDC preparedness. One idea is a pre-funded buffer: stablecoin issuers would keep high-quality collateral at the central bank, covering a safe fraction of coins. In a crisis, this buffer could cover redemptions before CBDC runs increase, reducing the need for large-scale neutrality operations. Policymakers thinking about stablecoin laws should build this buffer early, rather than rushing to impose neutrality programs under stress.

Putting Neutrality Into Practice

Turning CBDC neutrality from concept to practice requires three main elements. First, liquidity support needs to be automatic. An algorithm should hourly connect digital currency outflows to reserve injections, crediting banks without waiting for requests. This avoids stigma and matches outflow and inflow speeds. Second, all banks—community and large money-center banks—must have equal access to digital collateral channels, or neutrality might unfairly favor bigger players and hurt financial inclusion. Third, transparency should be balanced: daily reports on overall neutrality support help markets understand conditions, but specific bank data should remain confidential to avoid panic.

How does this work in real life? According to the Bank of England’s 2026 Liquidity Readiness Framework, banks are required to prepare for potential rapid digital withdrawals and hold assets that can be used for same-day liquidity. The framework also recognizes the risks associated with central digital currency (CBDC) flows and mandates quarterly testing that includes scenarios such as payment system errors and the rapid spread of rumors online. A paper from the European Central Bank explores a two-tier remuneration system for central financial institution digital currencies, intended to manage risks such as bank disintermediation and large-scale withdrawals during financial stress. S. laws would make neutrality a formal part of the Federal Reserve’s responsibilities, linking CBDC issuance and reserve management.

Instructors can bring this into the classroom. Simulation exercises in which students adjust CBDC flows, liquidity swaps, and capital buffers under stress will help them grasp neutrality in practice rather than in theory. Administrators running local payment pilots, such as campus meal plans using tokens, should analyze how PDP migration might affect their banks and plan in advance to provide matching reserve support.

Lastly, central banks need to adapt their communication. Crisis briefings should include a “digital liquidity barometer” showing CBDC uptake, collateral use, and neutrality lending in language that ordinary people can understand. Transparency creates trust, and trust slows withdrawals. According to research by Barucci, Gurgone, Iori, and Azzone, a macroeconomic agent-based model was used to examine how introducing a Central Digital Bank Digital Currency can impact economic security and welfare, but there is no reported behavioral experiment from the Netherlands in 2025 involving users and simulated digital bank runs in the provided source.

To summarize, the SVB collapse showed how quickly trust can vanish with a swipe. CBDC neutrality acts as a firewall, enabling sovereign digital currencies to operate rapidly without jeopardizing the system. This policy isn’t new or complicated—it adapts classic emergency lending principles into digital systems. But it will only work if educators teach it, administrators practice it, and decision-makers embed it into law before the next digital crisis. We need to build this safety valve now, or face relearning these lessons during an emergency.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Acharya, V. and Shin, H. (2025) Rapid runs and digital panic: evidence from real-time payment data. Princeton University Working Paper.

Bank for International Settlements (n.d.) Central bank digital currencies: legal and system design considerations.

Bank for International Settlements (2025) Basel III monitoring report: digital liquidity addendum.

Barrdear, J. and Kumhof, M. (2023) The macroeconomics of central bank digital currencies. Bank of England Staff Working Paper, No. 943.

Bouis, R., Gelos, G., Nakamura, F., Miettinen, P. A., Nier, E. and Soderberg, G. (2024) Central bank digital currencies and financial stability: balance sheet analysis and policy choices. IMF Working Paper.

Bossone, B. (2026) ‘CBDC neutrality, bank liquidity and the hybrid nature of bank deposits’. VoxEU, 20 March.

Brousse, C., Joyez, J. and Riesi, C. (2024) Digitalisation – a potential factor in accelerating bank runs? Banque de France Publication.

Chang, H., Grinberg, F., Gornicka, L., Miccoli, M. and Tan, B. J. (2023) Central bank digital currency and bank disintermediation in a portfolio choice model. IMF Working Paper.

Duffie, D. (2024) ‘Payment system challenges after the Silicon Valley Bank run’. Journal of Financial Regulation, 10 (2), pp. 145–168.

European Central Bank (2025) Digital euro progress report.

European Systemic Risk Board (2025) Report on stablecoins, crypto-investment products and multi-function groups.

Financial Stability Board (n.d.) Report on global stablecoin arrangements.

Fund, I. M. (2024) Thinking through central bank digital currency. IMF Institute.

Global Business and Finance Magazine Editorial Team (2025) ‘Multi-issuer stablecoins: a threat to financial stability’. Global Business and Finance Magazine, 27 October.

Illes, A., Kosse, A. and Wierts, P. (2025) Advancing in tandem – results of the 2024 BIS survey on central bank digital currencies and crypto. BIS Papers, No. 159.

International Monetary Fund (2020) Central bank digital currencies: principles and policy considerations. Fintech Notes.

Kaminska, I. (2025) ‘Faster than fear: the mechanics of modern bank runs’. Financial Times, 7 July.

Niepelt, D. (2026) Insulating banks: neutrality conditions for CBDC. CEPR Discussion Paper, No. 21141.

Reuters (2026) ‘Bank of England strengthens digital liquidity framework’, 17 March.

Sablik, T. (2024) ‘Central bank lending lessons from the 2023 bank crisis’. Econ Focus, Q3.

Tuinstra, M. and de Vries, E. (2025) Behavioural responses to digital run scenarios: evidence from Dutch households. De Nederlandsche Bank Occasional Study, 19 (4).

Weinstein, A. (2023) ‘Silicon Valley Bank: withdrawals of $42 billion attempted a day before US bank’s collapse’. NDTV, 11 March.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.