China Supply Chain Subsidies: Breaking the Grip on Global Trade

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

China’s subsidies distort trade and weaken global competition They give China power across the whole supply chain Fair trade now needs rules that restore balance

In 2024, approximately 75% of new electric vehicle batteries worldwide, 80% of solar modules, and nearly 70% of refined critical minerals were produced under “Made in China” labels. According to the OECD, industrial subsidies worldwide reached over 108 billion US dollars in 2023, reflecting a significant increase in government support for manufacturers, including through preferential loans, tax incentives, and direct state equity investments. In the average support extended to firms in high-income countries. This substantial subsidy is far from a minor discount; rather, it functions as a systemic financial transfer that significantly lowers production costs, consequently undermining foreign competitors and creating strong commercial dependencies on Chinese suppliers. What initially began as an effort to boost exports has, over time, evolved into an entrenched structural advantage. Consequently, contemporary policy debates should pivot away from familiar tariff disputes and focus instead on this emergent economic power dynamic.

The Scale and Design of China’s Subsidies

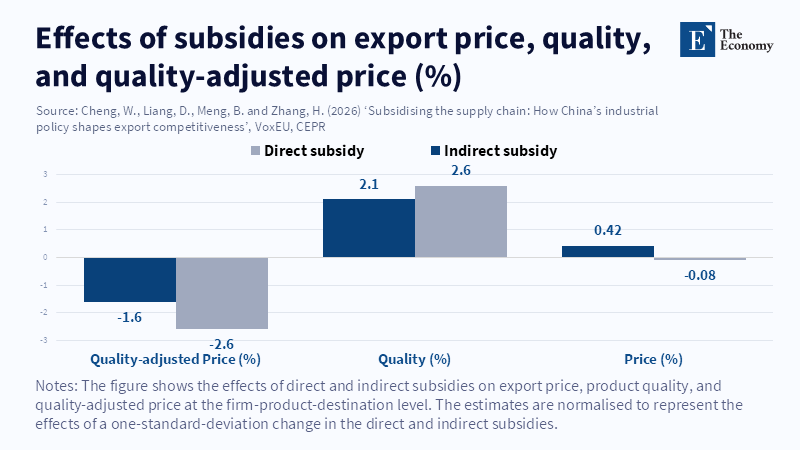

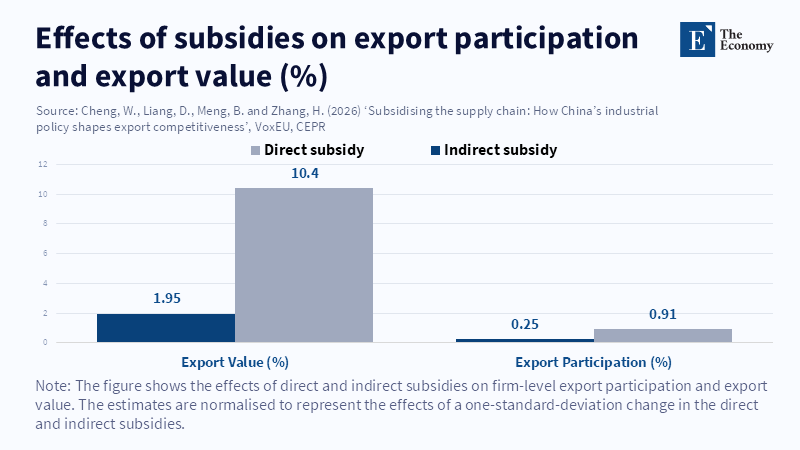

Proponents defending China’s policies acknowledge that subsidies are a legitimate economic instrument used by many nations. However, the scale and design of these interventions justify careful consideration. The most recent OECD synthesis reveals that over half of China’s subsidies are applied at upstream stages and permeate entire value chains. For example, a subsidy for polysilicon production cascades through subsequent processes, such as wafer slicing and module assembly, eventually affecting retail electricity costs in foreign markets. This layered effect creates a “subsidy multiplier” that amplifies Chinese competitiveness even where the direct subsidies appear modest. Viewed through this all-encompassing framework, the issue transcends isolated dumping incidents and instead constitutes the establishment of subsidy-conditioned ecosystems. Such ecosystems structurally expose trading partners to considerable vulnerabilities, as they hinge on deeply embedded supports rather than conventional market forces.

The risks associated with such dependency remain measurable and have considerable implications. Data from the International Energy Agency demonstrate that China refines the majority of the nineteen strategic minerals essential for clean energy technologies, controlling, on average, about seventy percent of the global market share. Supply disruptions, such as output curtailments and stockpiling activity, led to higher alumina prices in early 2023, according to S&P Global. According to the International Energy Agency, the supply chain for LFP batteries is heavily concentrated in China, with over 98% of both LFP cathode material and battery cells produced there. This concentration means that any significant disruption in Chinese processing, even for a few months, could have a major impact on global battery pack deliveries, showing how effective supply chains can also become critical points of vulnerability.

The consumer benefits derived from low prices associated with Chinese manufacturing are also diminishing. Investigations reported by the Guardian show that while Chinese electric vehicle manufacturers secured a 76% share of global sales by late 2024, the average battery cost outside China declined by just 9%, compared with a 30% reduction within China itself. According to the International Energy Agency, battery pack prices in China were 30 percent lower than in the United States and 35 percent lower than in Europe in 2025. This ongoing price differential has contributed to market consolidation, resulting in fewer non-Chinese battery cell producers with production capacities exceeding five gigawatt-hour between 2020 and 2025. The number contracted from twelve to five. The decline in competition frequently heralds the erosion of price advantages transferred to consumers.

Policy Responses and Their Limitations

Furthermore, the dominance fostered by subsidy-driven policies also has repercussions for labor markets. According to a study by Yuxue Chi and colleagues published in 2024, supply-side shocks in China's upstream basic metals sector are able to disrupt downstream manufacturing industries by causing supply contract issues, which may negatively affect employment in related sectors across global supply chains. This deterioration is often invisible in national economic accounts until plant closures occur, at which point the social and economic costs materialize palpably in depopulated communities rather than in conventional financial indicators.

Dealing with these challenges necessitates a shift from responsive measures towards structural reform in regulatory systems. Retaliatory tariffs, although commonly employed, offer a blunt instrument that misdiagnoses the problem. While tariffs may equalize price differences at borders, they do not restore lost production capacity nor facilitate the diversification of supply sources. Moreover, they risk provoking reciprocal actions that fracture global markets into fragmented blocs. Although the idea of making tariff exemptions dependent on transparent disclosure of non-commercial financing in imported goods could potentially encourage companies to reveal the extent of subsidies embedded in their products, the report by Cornago and colleagues does not specifically mention such conditional access regimes as a recommended measure. In cases of non-disclosure, import duties can be applied based on the best available estimates. The legal foundations for such mechanisms exist under the WTO Agreement on Subsidies, although coordinated enforcement remains lacking.

Building Structural Safeguards

Another policy approach is to align public procurement practices with supply diversity objectives. For instance, when institutions such as school districts procure solar installations or transit authorities acquire electric buses, procurement criteria can be structured to award higher scores to bids that source critical components from at least two distinct geographic regions. This strategy does not exclude Chinese products but aims to reduce systemic dependence on them. According to a report by Steve Murphy, Geoff Crittenden, and Tim Buckley, including local content requirements in Australia’s renewable energy tenders helps ensure that local businesses, communities, and workers, including First Nations people, can benefit directly from the country’s accelerated energy transition.

Finally, it is important for international partners to invest cooperatively in shared production capacity rather than engaging in parallel subsidy competitions. Developing joint facilities, such as cathode refining operations in Indonesia or wafer slicing plants in India, can help spread risk more effectively without having every country duplicate every stage of the value chain. Assuring reliable and secure access to critical minerals is a top priority for the United States as it intends to maintain leadership in areas such as solar panels, electric vehicles, batteries, and semiconductors, according to James Guild. While some critics note that this approach replicates China’s state-led strategy, the difference is in governance structures: consortium-based financing entails transparent covenants and defined end provisions, in contrast to covert state subsidies lacking accountability.

Reestablishing equilibrium in the fragmented international economic order requires a subtle understanding of the trade-offs involved. Skeptics doubt whether consumers genuinely bear losses if another country assumes part of the subsidy burden. The main factor is temporal: subsidies transfer wealth from foreign taxpayers to domestic consumers in the short term but impose concentration risks over the longer horizon. According to the OECD, since at least 2020, semiconductor firms in China have received larger subsidies relative to their revenue compared to other regions, even as government support for the semiconductor industry has increased across most major economies.

Addressing Counterarguments

Others argue that efforts to confront China may merely incentivize Beijing to intensify its subsidy policies. However, available evidence indicates that collective international action can produce contrary effects. According to data from the General Administration of Customs cited by Mysteel, Chinese stainless steel exports actually rose by nearly 26 percent year-on-year in 2024, reaching an all-time high, despite international anti-dumping measures introduced in 2023.

A further contention centers on the legitimacy of subsidies, noting that many advanced economies also provide industrial support. While this is accurate, the issue is one of scale and symmetry. According to the OECD, government support for renewables under the Inflation Reduction Act in the United States is expected to amount to 38 billion dollars per year from 2023 to 2033, in addition to 25 billion dollars annually from the Bipartisan Infrastructure Bill between 2021 and 2025. Together, these measures represent about 0.3 percent of US GDP in 2023, which is half the share of EU countries’ spending on renewable energy subsidies, which reached 0.6 percent of GDP in 2020. The OECD does not provide evidence that China’s combined subsidies and concessional credit exceed those of the European Union and the United States combined. Accepting current imbalances as normalized effectively rewards the dominant actor and penalizes those exercising greater fiscal restraint.

Accordingly, trade policy must transition from episodic tariff conflicts to establishing durable structural safeguards. Measures such as enhanced transparency requirements, incentives that promote supply chain diversification, and coordinated planned investments can progressively narrow subsidy disparities without resorting to protectionism. Such policies recognize China as both a partner, where interests converge, and a competitor, where interests diverge—thus sustaining an open yet resilient international market architecture.

Returning to the initial statistics, the conclusion is unequivocal. Provided that China’s subsidization continues to control roughly three-quarters of the essential inputs underpinning modern economies, any supply disruption, policy tension, or domestic challenge in Beijing reverberates globally. The objective should not be to marginalize China but to moderate the overbearing influence exercised through public financial support. If educational institutions, procurement agencies, and decision-makers commit to this objective—through promoting transparent cost accounting, adopting diversified sourcing policies, and enforcing resilience-oriented regulations—the current asymmetric value chains can evolve into genuinely global networks. Absent such efforts, upcoming crises will serve as clear reminders of the concentrated power embedded within today’s economically vital supply chains.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Australian Institute of International Affairs (2024) ‘It’s you, not me’: China’s subsidies and global trade tensions. Australian Outlook, 21 October.

Bureau of Economic Analysis (2012) ‘How are the measures of production and income in the national accounts affected by a disaster?’. U.S. Bureau of Economic Analysis FAQ, 28 November.

Cheng, W., Liang, D., Meng, B. and Zhang, H. (2025) ‘Subsidising the supply chain: How China’s industrial policy shapes export competitiveness’. VoxEU, 2 July.

Chi, Y., Jing, Z., Liu, Z. and Zhou, X. (2024) ‘Risk spillovers in Chinese production network: A supply-side shock perspective’. Humanities and Social Sciences Communications, 11(1), pp. 1–16.

Crowe, D. and Rawdanowicz, Ł. (2023) ‘Risks and opportunities of reshaping global value chains’. OECD Economics Department Working Papers, No. 1762. Paris: OECD Publishing.

Global Trade Alert, The New Industrial Policy Observatory and the Competition Research Policy Network (2024) The state of play of industrial subsidies: 2024 update. London: CEPR Press.

Gourley, P. (2025) ‘Free Trade vs Fair Trade’. Econ Soapbox, 31 March.

Guild, J. (2026) Advancing resilient critical mineral supply chains in Indonesia: A triumvirate approach. Seattle, WA: The National Bureau of Asian Research.

International Energy Agency (2025a) Global Critical Minerals Outlook 2025. Paris: IEA.

International Energy Agency (2025b) Global EV Outlook 2025. Paris: IEA.

International Energy Agency (2026) ‘Global battery markets are growing strongly – and so are the supply risks’. IEA Commentary, 13 February.

International Monetary Fund (2001) Trade policy conditionality in Fund-supported programs. Washington, DC: International Monetary Fund.

OECD (2023a) OECD Competition Trends 2023. Paris: OECD Publishing.

OECD (2023b) Economic Policy Reforms 2023: Going for Growth. Paris: OECD Publishing.

OECD (2025a) ‘The state of play of industrial subsidies as of 2023’. OECD Policy Briefs, No. 22. Paris: OECD Publishing.

Ruta, M. and Sztajerowska, M. (2025) ‘Shifting advantages: Do subsidies shape cross-border investment?’. IMF Working Papers, WP/25/80. Washington, DC: International Monetary Fund.

S&P Global Commodity Insights (2023) ‘Trade review: Q2 alumina balance hinges on supply disruption risks, lackluster aluminum demand’. S&P Global Commodity Insights, 18 April.

S&P Global Market Intelligence (2023) ‘The Fiscal Responsibility Act: Reduced fiscal risks, modest fiscal restraint’. S&P Global Market Intelligence, 14 June.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.