Mortgage Interest Impact on Consumption: The Hidden Lesson for Europe’s Educators

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

Mortgage repricing shapes consumption more than many policymakers assume Lower-income borrowers feel the pressure first, and the effects last beyond rate moves Education budgets should track mortgage exposure as closely as inflation or wages

Recent administrative data from the United Kingdom, encompassing approximately 6 million real-world refinancing cases involving expiring fixed-rate mortgages, indicate that a 1 percentage-point reduction in mortgage interest rates corresponds to an approximate 3% increase in household consumption within 6 months. According to a 2024 report from Spain's National Statistics Institute (INE), average household expenditure increased by 4.4% to 34,044 euros; rising mortgage payments have played a major role in shaping household budgets and could reduce retail consumption across the euro area by billions of euros, drawing comparisons to the scale of national education budgets. budget. This statistical relationship extends beyond mere economic observation; it compels a reconceptualization of monetary policy as a subtle yet powerful force that shapes citizens’ financial capacity to invest in education, nutrition, and savings. Consequently, understanding how mortgage interest rates affect consumption patterns transcends specialized monetary policy circles and becomes critical knowledge for policymakers involved in education planning, university funding distribution, and public budgeting.

How Mortgage Rate Shifts Reshape Household Spending

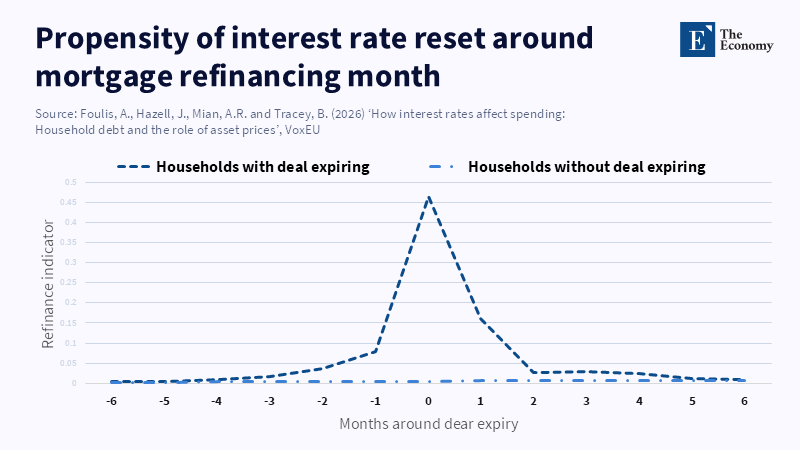

The impact of fluctuations in mortgage interest rates on consumption patterns is significantly altering household financial management. Established interpretations have emphasized debt-service ratios—defined as the proportion of monthly income devoted to interest payments—as the primary channel through which changes in interest rates affect consumer spending. However, recent micro-level analyses challenge this system. According to research from the Bank of England, UK households that benefited from rising house prices have tapped into their home equity through refinancing, enabling them to maintain or even increase their spending despite changes in mortgage costs.

This distinction is becoming more important in today’s economy. According to TheGlobalEconomy.com, the average euro-area mortgage interest rate rose to 2.42% as of December 2025, reflecting central bank policy changes during this period. Crucially, the impact on household cash flow manifests only upon contract repricing events. According to the European Central Bank, expectations for mortgage interest rates have risen slightly, with the latest survey showing an increase from 4.6% in November to 4.7% in December.

The Regressive Burden: Who Bears the Greatest Risk

Three distributional considerations point up the criticality of this issue for policy design. First, households in the lower income quintiles are disproportionately exposed to adjustable-rate mortgages or soon-to-be repriced loans—73% compared to 31% among the highest income quintile. Second, by 2024, the lowest-income group was already subject to average mortgage interest rates of approximately 3%, compared with rates just over 2% for the wealthiest cohort. Third, nearly half of euro-area mortgage holders reported reducing their spending in response to increased rates in the previous year, while a similar proportion anticipate further cutbacks in the coming year. These patterns highlight a lagged and regressive dynamic: the monetary strain from mortgage repricing waves tends to impact lower-income families first and most severely, often well after central bank policy alterations have occurred.

The UK’s micro-level estimates stem from difference-in-differences methodologies that track consumption using debit-card data around refinancing events. According to the European Central Bank, comparable figures for the euro area are calculated by combining mortgage interest rate data with survey-based micro-level weights, assuming that loan origination spreads remain stable after March 2025.

Addressing doubt about the relevance of UK data for the euro area, it is important to recognize that the UK mortgage market’s prevalence of short-term fixed-rate contracts has been viewed as an amplification mechanism for interest rate changes, which longer-term fixed contracts common in continental Europe ostensibly mitigate. Nonetheless, recent euro-area data challenge this assumption. According to the European Central Bank, in the euro area, about one-quarter of mortgages are adjustable-rate mortgages, and a little over one-third have rates fixed for longer than ten years, with the rest set to be repriced after several years, indicating that changes in mortgage rates could have varying impacts on aggregate demand depending on the country. According to a report from Banco de Portugal, the share of foreign citizens in Portugal’s housing loans increased from 6.9% to 8.2% between December 2022 and June 2024. ECB assessments of mortgage affordability confirm that even after projected policy easing in mid-2025, mortgage repayments will consume a larger proportion of disposable income than at any time since 2013.

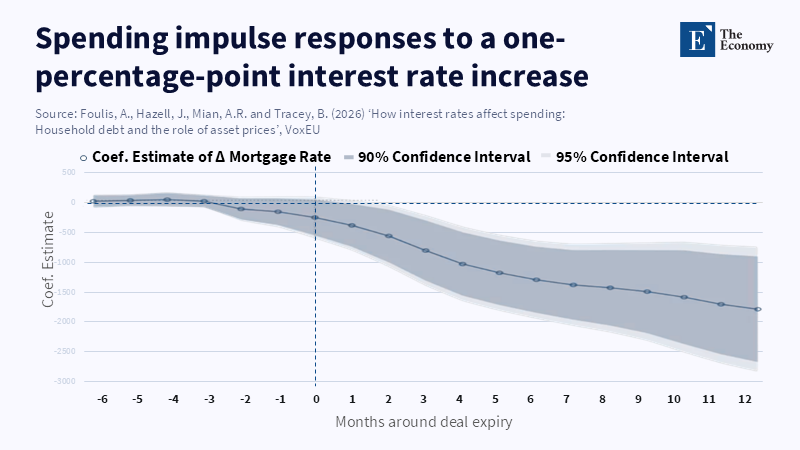

The behavioral repercussions are increasingly observable. According to a recent report from the European Central Bank, discretionary retail card spending has decreased by about 4% year on year during periods when mortgage repricing surges have surpassed the average of the previous five years. The analysis shows that roughly one-third of this decline can be attributed to immediate cash-flow pressures, while the remainder is attributable to balance-sheet effects as homeowners cut back on borrowing. against home equity that has diminished in perceived affordability. This implies that shifts in asset-price expectations, rather than changes in interest payments alone, predominantly influence consumption dynamics.

Implications for Education Funding and Public Budgets

These economic effects bear direct consequences for educational providers and public administrators. Declines in retail activity affect municipal revenue bases, including sales taxes that fund after-school programming. Simultaneously, constraints on housing equity limit parents’ ability to finance private educational services such as tutoring and higher education fees. Even temporary rate increases can lead to sustained budgetary shortfalls for educational institutions if mortgage repricing spans multiple years.

From a policy perspective, several implications emerge. First, financial aid programs for education, including tuition assistance and meal subsidies, should consider mortgage-related risk indicators alongside income thresholds. Households with significant adjustable-rate debt may reduce education expenditures disproportionately during periods of rate volatility, suggesting that targeted grants could preserve educational investment more efficiently than uniform tuition adjustments.

Second, local governments should incorporate mortgage-linked consumption scenarios into financial planning and stress-testing exercises. In jurisdictions where variable-rate mortgages account for over 50% of the market, modest rate increases of about 75 basis points may reduce retail revenues—and, correspondingly, discretionary education budgets—by approximately 1%. Integrating granular data from sources such as the Consumer Outlook Survey with fiscal models would improve early identification of fiscal vulnerabilities.

Third, coordination among central banks, finance ministries, and education departments is imperative when navigating rapid changes in monetary policy. When rate reductions are anticipated, the presence of substantial mortgage portfolios subject to upward repricing may delay intended expansions in household spending, dampening the stimulative effect. Implementing transitional measures, such as time-limited mortgage payment deferrals or equity-release programs contingent on educational expenditures, may facilitate more prompt economic transmission supporting human capital development.

Finally, there is an urgent necessity to update financial literacy curricula to reflect these conditions. Instruction on the distinction between nominal and real mortgage interest rates, and on the relative roles of debt-service burdens and collateral effects, should be integrated alongside traditional quantitative subjects. Incorporating modules that explain how mortgage financing influences consumption across the life cycle would improve long-term household resilience.

Addressing the Counterarguments

Anticipating critique, three common counterarguments merit consideration. First, some posit that elevated household savings buffers accumulated during the pandemic offset mortgage-related shocks. While aggregate savings remain elevated by approximately €700 billion, survey data indicate that only a minority—around 12%—of budget-constrained households intend to draw down these reserves; most prefer to accelerate principal repayments when rates rise, thereby limiting the buffer’s impact on consumption smoothing.

Second, assertions that wage growth compensates for higher mortgage costs warrant scrutiny. According to a report from the European Central Bank, in the euro area, around one-quarter of mortgages are adjustable-rate, and a sizable proportion are fixed for several years before being repriced at current market rates. This leads to marked increases in mortgage payments for those with repricing loans, which can greatly affect borrowers, especially younger households with higher loan-to-income ratios.

Third, arguments that show the insulating effect of the prevalence of fixed-rate mortgages in countries such as Germany overlook monetary policy’s cross-border externalities. For example, reduced discretionary travel spending by Spanish households can adversely affect German tourism revenues, illustrating the linkages of economic activity across the region.

Lastly, concerns that discussions of mortgage finance exceed the remit of education-focused publications are misplaced. Educational institutions serve as sites where societies prepare individuals to address future economic challenges; therefore, explicating the implicit curriculum embedded in monetary policy is germane to their mission.

In conclusion, the initial statistic, that a one percentage-point reduction in mortgage interest rates may trigger a 3% increase in consumption, should be regarded not as a mere anecdote but as a key indicator of continuing economic dynamics. The euro-area mortgage landscape persists, characterized by a protracted and uneven repricing pipeline determined by prior monetary tightening. Without incorporating mortgage-exposure metrics into education funding models and budgetary frameworks, policymakers and administrators risk planning for economic conditions that are unlikely to materialize. A coordinated agenda that demands the integration of mortgage sensitivity data, the promotion of refinancing mechanisms that mitigate fiscal strain, and advanced educational programming on the implications of interest rates is essential. Allowing the complications of monetary transmission to influence social investment invisibly weakens efforts to build economic resilience plus sustain human capital development.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Banco de Portugal (2024) Financial Stability Report – November 2024.

Bank for International Settlements (2025) Debt service ratios – overview. BIS Data Portal.

Bank of England (2025) Monetary Policy Report – May 2025. London: Bank of England.

Baptista, P., Dossche, M., Hannon, A., Henricot, D., Kouvavas, O., Malacrino, D. and Zimmermann, L. (2025a) ‘The transmission of monetary policy: from mortgage rates to consumption’, ECB Economic Bulletin, Issue 4/2025, Article 1.

Baptista, P., Dossche, M., Hannon, A., Henricot, D., Kouvavas, O., Malacrino, D. and Zimmermann, L. (2025b) ‘Monetary policy transmission: from mortgage rates to consumption’, ECB Blog, 28 May.

Ciganović, M., Gagliardi, E.S. and Tancioni, M. (2025) Disentangling the distributional effects of financial shocks in the euro area. arXiv preprint arXiv:2510.11289.

Cooper, D., Garga, V. and Luengo-Prado, M.J. (2025) ‘The mortgage rate channel of monetary policy transmission: A tale of two countries’, Macroeconomic Dynamics, 29, e163.

European Central Bank (2025) ‘The ripple effects of monetary policy on housing and consumption’, ECB Blog, 31 July.

Foulis, A.K., Hazell, J., Mian, A.R. and Tracey, B. (2026a) ‘How interest rates affect spending: Household debt and the role of asset prices’, VoxEU, 26 March.

Foulis, A.K., Hazell, J., Mian, A.R. and Tracey, B. (2026b) How do interest rates affect consumption? Household debt and the role of asset prices. Bank of England Staff Working Paper No. 1173.

Foulis, A.K., Hazell, J., Mian, A.R. and Tracey, B. (2026c) How do interest rates affect consumption? Household debt and the role of asset prices. NBER Working Paper No. 34911.

Instituto Nacional de Estadística (2025) Household Budget Survey (HBS). Year 2024. Final results.

Lin, C.C., Semelsberger, S., Al Saeed, A., Weiss, J., Navarro, R.A. and Gianakos, A.L. (2023) ‘Perception of debt during resident education: A systematic review’, The Permanente Journal, 27(3), pp. 99–109.

Liu, L. (2023) The demand for long-term mortgage contracts and the role of collateral. Bank of England Staff Working Paper No. 1009.

OECD (2024) OECD Economic Surveys: United Kingdom 2024. Paris: OECD Publishing.

Swiss National Bank (2022) Financial Stability Report 2022.

TheGlobalEconomy.com (2025) Euro area: Mortgage credit interest rate.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.