Fiscal Consolidation After the Energy Shock: Why the Old Textbook Is Not Enough

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

Fiscal consolidation is harder when inflation is driven by energy shocks and war Monetary policy cannot always cushion austerity in a supply-shock economy Governments should protect education and core public investment while restoring fiscal credibility

Global public debt is climbing toward a level that once looked extreme. In 2025, the IMF warned that world public debt could move close to 100% of GDP by 2030. Later that year, it said debt could rise above that line by 2029, a level not seen since the late 1940s. That headline seems to point to one clear answer: tighten budgets, calm bond markets, and trust monetary policy to soften the hit. But that answer is too neat for the world we live in now. Fiscal consolidation still matters. In many countries, it cannot be avoided. Yet its real cost depends on what kind of inflation the economy faces and whether central banks can safely support demand. When inflation comes from oil, gas, food, and war-driven supply shocks, that support becomes less reliable. The question is no longer whether governments should adjust. The real question is how they can do it without cutting growth, widening inequality, and weakening core public goods such as education.

Fiscal consolidation works only when the policy mix works

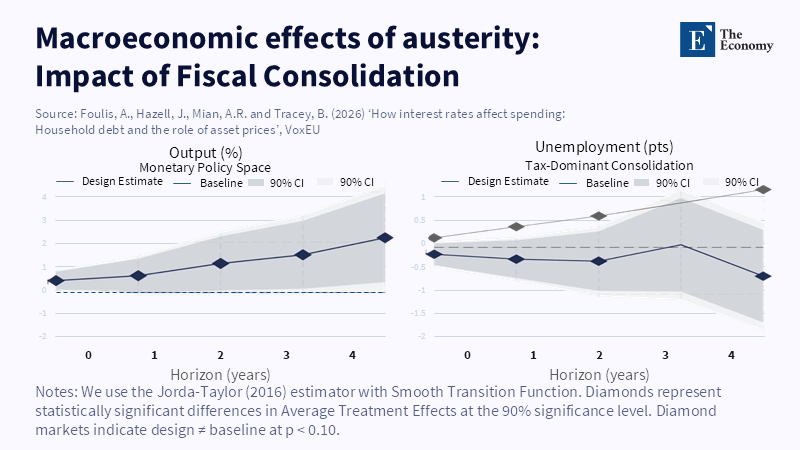

The basic lesson from the recent fiscal consolidation debate is clear. Budget tightening causes less harm when it is well-designed and when monetary policy has room to lean the other way. That is the part of the old textbook that still holds. If a government cuts its deficit while the central bank can ease, borrowing costs can fall, private demand can hold up, and the fall in output can be smaller. Recent work on fiscal consolidation also stresses that the choice of instrument matters. Packages that rely more on taxes and less on blunt cuts to public services can reduce some of the social damage. That matters most when governments are trying to protect poor households and avoid a rise in inequality. In that sense, fiscal consolidation is not one policy. It is a set of choices, and those choices shape who pays, how much demand is lost, and what kind of recovery is still possible.

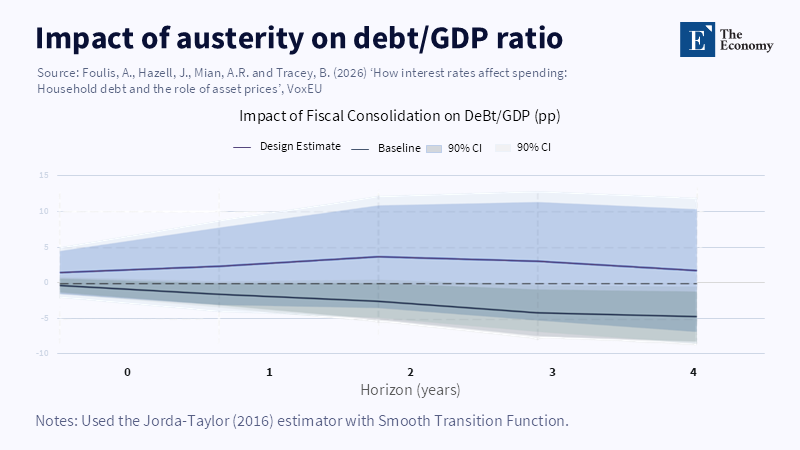

The broader evidence is less comforting. IMF research has long found that fiscal consolidation usually cuts output and raises unemployment in the short run. It also tends to widen inequality, and spending-based packages often do more harm than tax-based ones. The World Bank’s new review of 124 consolidation episodes reaches a similar but harder conclusion. Fiscal consolidation often helps to stop debt from rising. But it rarely delivers all the goals at the same time. According to the World Bank, global poverty reduction has slowed, with nearly 700 million people still living in extreme poverty. The report highlights that setbacks from COVID-19, low economic growth, and greater fragility have hindered progress in reducing poverty. Fiscal consolidation can work. But it does not work cheaply on its own. It has to be well timed, well designed, and supported by the rest of the macro policy.

A second point is easy to miss. A package can look successful on paper and still leave serious damage in its wake. A country may stabilize its debt yet still emerge from fiscal consolidation with weaker wages, lower public investment, and a thinner social state. That is why the word “sustainable” matters so much here. Fiscal sustainability is not only about the debt ratio. It is also about whether the state can continue funding the systems that sustain growth. If the adjustment protects those systems, it may strengthen credibility. If it strips them down, it may weaken the economy that is supposed to carry the debt burden later. The debate, then, is not just about whether fiscal consolidation happens. It is about what kind of state survives afterward.

Fiscal consolidation is harder when inflation comes from oil, gas, and war

The weak point in the textbook story is the belief that monetary policy can always soften austerity. That belief breaks down when inflation is imported. In March 2026, the ECB said this plainly: monetary policy cannot bring down energy prices. It can only try to prevent an energy shock from spilling into broader inflation through wages, prices, and expectations. That is a much harder job. It means a central bank may not be willing to cut rates just because fiscal consolidation is dragging on demand. If the shock persists, or if households and firms expect it to, monetary policy may remain tight for longer. In those moments, fiscal consolidation loses the safety cushion that many standard models quietly assume.

This is not a remote risk. Europe has already gone through one major energy-price shock after Russia’s invasion of Ukraine. ECB analysis now again warns that large energy shocks can pass through to broader inflation in non-linear ways. Small shocks may stay inside the energy component. Large and lasting ones can spread more widely, especially when firms reprice faster and workers still remember the last inflation surge. The global setting is also weak. The World Bank says growth is expected to edge down and remain subdued. It also says more than one-quarter of emerging and developing economies still have per capita incomes below 2019 levels. That is not a forgiving backdrop for fiscal consolidation. The need for adjustment may be real, but the margin for policy error is smaller than the textbook version suggests.

There is another limit. Fiscal consolidation does less to address the source of the problem when inflation is driven by oil, gas, food, or shipping shocks. It can curb domestic demand. But it cannot reopen a sea route, lower an import bill, or stop a war. According to the World Bank’s latest Commodity Markets Outlook, global commodity prices are expected to decline to their lowest point in six years by 2026, suggesting that when inflation is mainly caused by rising food and energy import costs, the impact of fiscal consolidation remains uncertain and should be more thoroughly discussed in public debates. A government may still need fiscal consolidation because debt is too high or interest costs are rising. But it should not pretend that budget tightening is a full inflation plan. In such periods, the better test is whether the state can narrow deficits without cutting the very investments that improve resilience, energy security, and future growth.

Fiscal consolidation becomes an education problem very fast

For education systems, this debate is not abstract. Fiscal consolidation often reaches schools and universities through the easiest channels. Hiring slows. Building repairs are delayed. Support staff vanishes. Small programs that help weaker students are called temporary and then cut. Yet education is one of the few public functions that supports both short-run resilience and long-run growth. When governments protect it, they protect human capital, labor supply, and social mobility. When they cut it deeply, they turn a budget adjustment into a future productivity problem. That is why a discussion of fiscal consolidation that focuses solely on debt ratios is too narrow for an education journal. The mix of the adjustment matters as much as the size.

The timing could hardly be worse. UNESCO reports that aid to education fell sharply in 2024 and is expected to decline by more than 25% by 2027. It also estimates an annual financing gap of almost $100 billion if countries are to meet education targets by 2030. The World Bank and UNESCO’s Education Finance Watch 2024 adds another warning. Total education spending per child has either decreased or stagnated worldwide, with the pressure strongest in poorer countries. UNESCO has also stressed that domestic financing, above all tax revenue, remains the main source of education funding in low- and middle-income countries. That makes fiscal consolidation a direct education issue. If governments lean on blunt spending cuts in a weak economy, education systems absorb the shock. If they use better tax measures and protect core learning budgets, the odds improve.

This also changes what “efficiency” should mean. In many fiscal consolidation plans, efficiency becomes a polite word for doing more with less forever. That is not real reform at all. Real efficiency means reducing waste, leakage, weak procurement, and poor targeting so that teachers, classrooms, and basic learning support are protected. IMF work on education spending in surveillance points to such a trade-off. Countries under adjustment are often advised to improve the quality and efficiency of education spending while creating fiscal space through wider public finance reform. That can make sense. But only if efficiency protects function instead of hiding cuts. Fiscal consolidation that hollows out education may help a budget line in the short run. It weakens growth capacity in the long run.

Fiscal consolidation should be judged by what it protects

A common reply is that this view is too soft on debt. According to a recent IMF working paper, data from 17 OECD countries and 14 nations in Latin America and the Caribbean show that expenditure-based fiscal consolidation is often more effective than revenue-based measures at stabilizing or reducing public debt. Governments with severe debt problems need credibility, and spending control is often part of that. But debt stabilization is only one test of success. If a package lowers debt while growth weakens, inequality rises, and education systems are cut back, the state may win a narrow accounting fight while losing productive strength. The whole purpose of linking fiscal sustainability to sustainable development is to stop treating those losses as side notes.

The stronger lesson is more disciplined, not less. Fiscal consolidation should be timed with care, coordinated with monetary policy where possible, and built around measures that protect vulnerable households and future growth. That means more caution about cutting education, health, and basic public investment. It means greater openness to progressive, broad-based tax reform. It means admitting that when inflation is being driven by energy shocks, central banks may not be able to rescue a badly designed adjustment. And it means rejecting the lazy claim that all fiscal consolidations work the same way. It does not. Some packages reduce debt and preserve state capacity. Others reduce debt while eating away at the base of future growth.

The debt headline from the start still matters. High debt, high interest costs, and weak growth force hard choices. But the lesson is not that governments should trust the old sequence of austerity first and relief later. The lesson is that fiscal consolidation now has to be built for a world of supply shocks, geopolitical risk, and fragile social investment. In that world, the best adjustment is not the one that cuts fastest. It is the one that proves the state can restore credibility without cutting into its own future. For educators, administrators, and policymakers, that means defending education inside the fiscal debate, not after it. It also means treating teachers, school systems, and basic learning support as productive assets, not easy savings. Once learning capacity is lost, a budget may look better on paper while the economy grows poorer in every way that counts.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Bhasin, K. and Loungani, P. (2026) ‘Designing fiscal consolidation to achieve fiscal sustainability and the sustainable development goals’, VoxEU, 30 March.

Di Lorenzo, P. and Lacey, E.A. (2025) A Primer on Restoring Fiscal Space and Sustainability. Washington, DC: World Bank.

Global Education Monitoring Report Team, UNESCO Institute for Statistics and World Bank (2024) Education Finance Watch 2024. Paris and Washington, DC: UNESCO and World Bank.

International Monetary Fund (2025a) Fiscal Monitor, April 2025: Fiscal Policy Under Uncertainty. Washington, DC: International Monetary Fund.

International Monetary Fund (2025b) Fiscal Monitor, October 2025: Spending Smarter. Washington, DC: International Monetary Fund.

Lagarde, C. (2026) ‘Navigating energy shocks: risks and policy responses’, keynote speech at The ECB and Its Watchers conference, Frankfurt am Main, 25 March.

Prospects Group, World Bank (2026) Global Economic Prospects, January 2026. Washington, DC: World Bank.

Soto, M., Palomba, G., Brollo, F., Carroll, N., Munkacsi, Z., Tumino, A., Atashbar, T., Shang, B. and Tessema, D. (2025) IMF Engagement on Education Spending in Surveillance and Program Work. IMF Technical Notes and Manuals 2025/07. Washington, DC: International Monetary Fund.

UNESCO (2025a) Aid to Education: Time for Tough Decisions. Paris: UNESCO Global Education Monitoring Report.

UNESCO (2025b) Monitoring SDG 4: Education Finance. Paris: UNESCO.

UNESCO (2025c) Investing in Education Increasingly Requires Domestic Resource Mobilization. Paris: UNESCO.

Woo, J., Bova, E., Kinda, T. and Zhang, Y.S. (2013) Distributional Consequences of Fiscal Consolidation and the Role of Fiscal Policy: What Do the Data Say? IMF Working Paper 13/195. Washington, DC: International Monetary Fund.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.