China Spillovers and the New Capability Shock in Education

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

China now shapes more than growth, trade, and prices In key sectors, its spillovers can weaken other countries’ industrial capacity Education policy must respond or skills will lose their economic value

In 2024, China was responsible for 80% of global battery cell production. That is not just a trade fact. It is a map of where industrial learning now happens, where engineers solve hard problems at scale, and where suppliers, technicians, and applied researchers gain real experience. For years, policymakers have read China spillovers mainly as a macro story. They looked at growth, inflation, commodity prices, and trade balances. That view is useful, but it is no longer enough. When one country holds that much weight in sectors that now sit at the heart of energy, transport, and advanced manufacturing, the spillover no longer looks like a normal external shock. It becomes a capability shock. It starts to shape which countries still make complex things, which universities can turn research into production, and which education systems can still promise that learning will lead to good work.

China spillovers are no longer just about growth

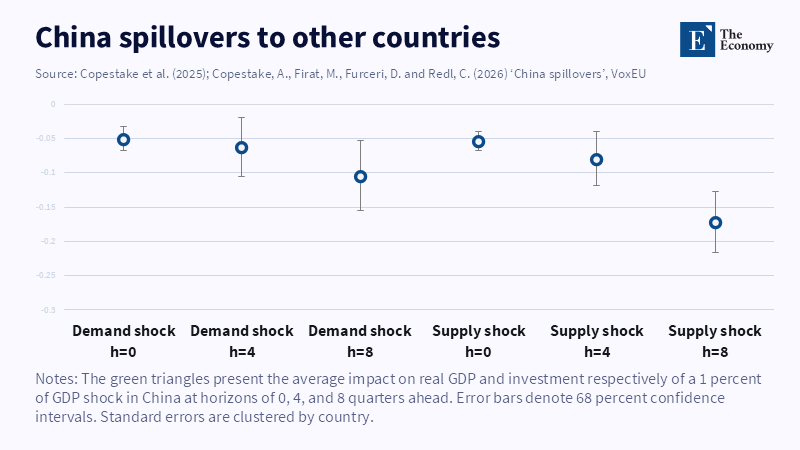

Recent research leaves little doubt that China's spillovers are now global in reach. A report from the International Monetary Fund, published in April 2025, assesses global growth and policy changes but does not provide specific findings on the worldwide economic impact of shocks from China relative to other emerging economies, nor does it offer precise estimates of how Chinese demand or supply shocks would affect oil prices. Earlier IMF work also found that slowdowns in China affect not only countries but firms, with foreign revenues and profits falling in clear ways. Another recent line of work shows that Chinese monetary policy travels outward through trade, commodities, and production links more than through the classic financial channel linked to the United States. Put simply, what happens in China now moves through the real economy of the rest of the world.

But the standard macro view still misses the part that matters most for long-run policy. It is one thing for a large economy to move commodity prices or lower foreign inflation for a few quarters. It is another for it to change the industrial shape of its trading partners. ECB scenario work from 2024 already points in that direction. According to VoxEU, when China’s export prices decline, this directly lowers import prices in the euro area and the US, which can have a disinflationary effect and increase competition in global markets. Those are not small moves. More importantly, they are overall effects that likely understate what happens inside exposed sectors, regions, and labor markets.

This is where the lens has to change. If China spillovers are broad and cyclical, governments can answer mostly with macro tools, temporary income support, or exchange-rate moves. But if China spillovers are concentrated in sectors where scale, subsidies, and supply-chain control matter, the issue is no longer just stabilization. It is whether other economies still keep the ability to learn by producing, refining, designing, and upgrading. Education policy cannot sit outside that question. Schools, colleges, and universities do not train people for “the global economy” in the abstract. They train people for real production systems, research settings, and local career ladders. Once those systems thin out, education starts to promise skills that the domestic economy cannot use well.

China spillovers in strategic sectors are different

The difference becomes clear once we move from the whole economy to strategic sectors. The IEA reports that China’s share in all major stages of solar panel manufacturing exceeds 80%. It has also invested more than USD 50 billion in new solar PV supply capacity and created more than 300,000 manufacturing jobs across the value chain since 2011. In batteries, the concentration is just as stark. The IEA’s 2025 outlook shows that China accounted for 80% of global battery cell production in 2024, almost 85% of cathode active material production, and more than 90% of anode active material production. In several stages of these supply chains, the world is not dealing with a normal leading exporter. It is dealing with a learning curve, cost base, and supplier network that have become heavily concentrated in one place.

That matters because concentrated China spillovers behave differently from broad China spillovers. Cheap imports can help consumers and can speed up the green transition. That part is true. The IEA is explicit that China has helped cut solar costs around the world. But lower prices are only part of the story. The same IEA work also warns that this degree of concentration creates resilience risks. The WTO’s 2024 trade policy review adds a second warning. It notes both the lack of transparency regarding certain aspects of China’s government support and the difficulty of measuring its effects because relevant data are not publicly available. When concentrated supply is paired with opaque support, trade surpluses, and export controls on strategic materials, the spillover becomes leverage. It can lower prices today while narrowing other countries’ room to build, learn, and compete tomorrow.

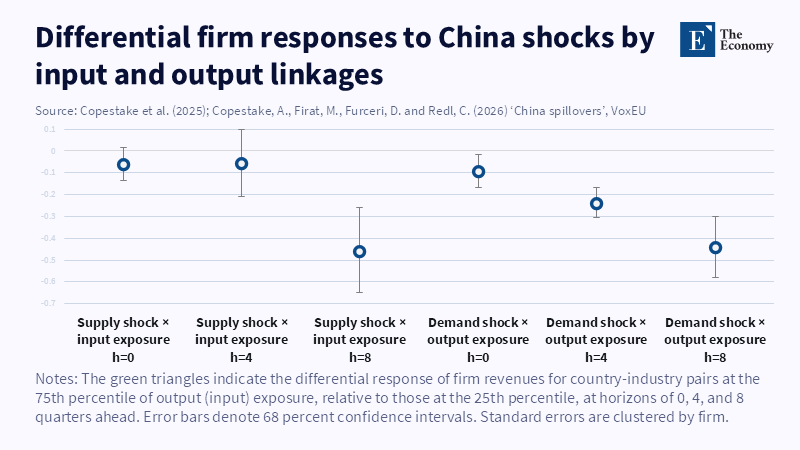

The newer industrial policy research points in the same direction. A 2026 working paper on industrial policies, global imbalances, and technological hegemony argues that when high-tech tradable sectors are pushed by unbalanced industrial policy, the result is not only bigger trade surpluses. It is also a shift in innovation and productivity toward the country using those policies, while the tradable sector in deficit economies shrinks. OECD work from 2025 heightens concerns. Industrial subsidies reached their highest level since the global financial crisis, and the most subsidized sectors over 2005–23 were solar cells and modules, semiconductors, aluminum, shipbuilding, and steel. Firms based in China continued to receive much larger subsidies relative to revenue than firms based elsewhere. Some China spillovers, then, are no longer best read as ordinary trade spillovers. They are policy-shaped transfers of know-how and industrial weight.

China spillovers are becoming education policy

Once China's spillovers are understood as capability shocks, the education effects come into view. An education system grows strong when it is tied to demanding firms, skilled suppliers, serious labs, and sectors that keep moving up the value chain. Learning does not happen only in classrooms. It happens in pilot plants, test lines, design teams, supplier checks, and production failures, all of which force workers and managers to improve. If a country loses these sites of learning, it does not just lose output. It loses feedback loops that keep curricula relevant. It loses apprenticeship markets. It loses mid-career technical roles that make engineering, chemistry, materials science, and industrial design attractive to students in the first place. It also loses faith that study will lead to a solid future. That loss is slow at first. Labs still publish. Degrees still look modern. But the day-to-day link between study and production weakens, and with it the practical knowledge that no syllabus can fully replace.

This is why an education policy that answers with generic talk about “more STEM” will fail. The question is not how many students can be pushed into broad technical fields. The question is whether training is tied to sectors that still exist locally at a meaningful scale. Europe’s current position is a warning. According to the International Energy Agency, the direct costs of producing lithium-ion battery cells are significantly lower in China than in the European Union, underscoring a notable cost gap between the two regions. When those gaps grow large enough, the education system starts training students for jobs, firms, and supply chains that are increasingly elsewhere. That weakens not only employment. It weakens the public trust that education still connects effort with reward.

The research side tells a similar story. OECD data released in 2025 show that China’s R&D spending grew by 8.7% in 2023, far faster than the OECD average, the United States, or the European Union. Measured in PPP terms, China’s R&D spending had risen to 96% of the US level by 2023. In higher education, China has reached 74% of the US level. WIPO’s 2025 indicators add another sign: China’s patent office received 1.8 million patent applications in 2024, or 49.1% of the world total. These figures do not mean that quantity equals quality in every case. But they do show where research effort, commercial pressure, and scale are gathering. For universities and technical institutes elsewhere, the risk is not that China suddenly teaches better lessons in every classroom. The risk is that the world’s most important industrial classrooms are moving offshore.

China spillovers demand a capability agenda in education

A serious response should avoid two easy mistakes. The first is denial. It is no longer credible to claim that education can remain neutral while the industrial structure shifts beneath it. Educators do not control trade policy, but they do shape how societies adapt to it. The second mistake is panic. A blanket retreat from openness would raise costs, slow diffusion, and hurt research cooperation. The goal is not educational nationalism. It is strategic realism. Countries should stay open to knowledge, trade, and scientific exchange while becoming far less casual about losing entire layers of industrial learning in sectors that matter for future productivity, wages, and social trust.

That means a different agenda for educators, administrators, and policymakers. Vocational systems should be tied to mission-critical sectors, not just to current vacancy lists. Universities should be rewarded not only for papers and patents but for building durable links with domestic production, testing, and scale-up. Public procurement in energy, transport, health technology, and digital infrastructure should be used to create predictable demand for local capability, giving education providers a real industrial partner to train with. Funding should flow into materials science, power electronics, battery chemistry, advanced manufacturing, grid engineering, and industrial software, as well as into technician pathways, applied institutes, and short reskilling routes for workers already in the system. The point is simple: if countries want students to believe in technical education, they must rebuild the sectors that make technical learning worth the effort.

The central fact remains the one we started with. When one country produces 80% of the world’s battery cells, the issue is no longer only trade exposure. It is where the future is being learned. China spillovers now reach far beyond prices and growth rates. In strategic sectors, they shape where production clusters, where R&D scales, where supplier knowledge deepens, and where students can realistically expect advanced work to exist. An education policy that ignores that shift will become ceremonial. It will keep talking about skills while the ecosystems that reward skill move elsewhere. The right response is neither nostalgia nor fear. That is the real education risk of this decade. It is a capability agenda: protect openness, but rebuild the local institutions of learning by doing. If we want education to remain a ladder into productive work, we have to care again about where the rungs are made, tested, and improved.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Abdel-Latif, H. and Popescu, A. (2025) Spillovers from Large Emerging Economies: How Dominant Is China? IMF Working Paper No. 25/27. Washington, DC: International Monetary Fund.

Cantor, C. and Gonzalez, L. (2025) ‘Building Out the Midstream’, ZETA, 22 April.

Cesa-Bianchi, A., Ferrero, A., Fornaro, L. and Wolf, M. (2026a) Industrial Policies, Global Imbalances and Technological Hegemony. CEPR Discussion Paper No. 21253. Paris and London: CEPR Press.

Cesa-Bianchi, A., Ferrero, A., Fornaro, L. and Wolf, M. (2026b) ‘Industrial policies, global imbalances, and technological hegemony’, VoxEU.org, 27 March.

Copestake, A., Firat, M., Furceri, D. and Redl, C. (2023) China Spillovers: Aggregate and Firm-Level Evidence. IMF Working Papers, 2023(206). Washington, DC: International Monetary Fund.

Copestake, A., Firat, M., Furceri, D. and Redl, C. (2026) ‘China spillovers’, VoxEU.org, 31 March.

Dieppe, A., Frankovic, I. and Liu, M. (2024) ‘China exports and spillover disinflation: Three scenarios’, VoxEU.org, 27 June.

Draghi, M. (2024) The Future of European Competitiveness. Brussels: European Commission.

EFE and Granda, M. (2025) ‘La china CATL gana un 15% más en 2024 e incrementa su dominio sobre la producción mundial de baterías’, Cinco Días, 15 March.

Ferriani, F. and Gazzani, A. (2025) ‘The international transmission of Chinese monetary policy and the commodity channel’, VoxEU.org, 3 March.

International Energy Agency (2022) Solar PV Global Supply Chains. Paris: IEA.

International Energy Agency (2025a) Estimated Direct Costs of Fully Domestic Lithium-Ion Battery Cell Production in the European Union and China, and Key Drivers to Reduce the Cost Gap. Paris: IEA.

International Energy Agency (2025b) Global EV Outlook 2025. Paris: IEA.

Mayger, J. and do Rosario, J. (2026) ‘IMF says China’s economic model is hurting the global economy’, Los Angeles Times, 18 February.

Miranda-Agrippino, S., Nenova, T. and Rey, H. (2026) The Ins & Outs of Chinese Monetary Policy Transmission. NBER Working Paper No. 34626. Cambridge, MA: National Bureau of Economic Research.

OECD (2025a) ‘R&D spending growth slows in OECD, surges in China; government support for energy and defence R&D rises sharply’, Statistical release, 31 March. Paris: OECD.

OECD (2025b) The State of Play of Industrial Subsidies as of 2023. OECD Policy Briefs, No. 22. Paris: OECD Publishing.

World Intellectual Property Organization (2025) World Intellectual Property Indicators 2025. Geneva: WIPO.

World Trade Organization (2024) Trade Policy Review: China. Report by the Secretariat, WT/TPR/S/458. Geneva: World Trade Organization.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.