When Higher Taxes Become Exit Signals: UK Tax Competitiveness and the Dubai Pull

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

UK tax changes are sending stronger exit signals to mobile wealth Dubai is turning tax clarity into a real platform for family offices and capital Britain risks slow competitive drift if it raises taxes without a stronger locational offer

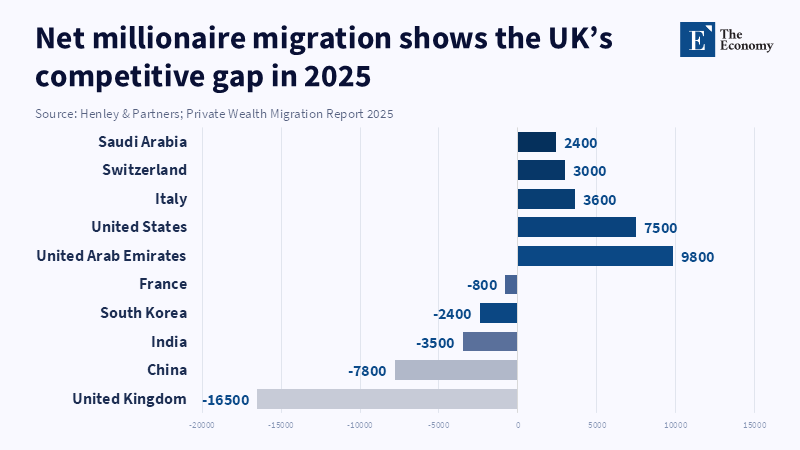

The strongest sign that UK tax competitiveness has become a genuine policy issue did not show up in a Treasury table; it showed up in a migration forecast. By 2025, the UK was due a net outflow of 16,500 millionaires, the biggest in the world, while the UAE would be due a net inflow of 9,800. This is much more than a story of personal wealth; it will inform where the founders are and where the family offices and advisers will go and where the money will start to gather. As soon as that process gathers even a little pace, its effects will travel on well beyond tax revenues and resonate through private markets, investment decisions, legal and accountancy services, philanthropy and eventually the whole knowledge economy. Britain had long been confident of a resilient London which would neither be shaken nor even ruffled by a more ambitious tax policy, but this now seems far too hopeful. In a truly mobile world of capitals and firms, the question for the UK is no longer only tax; it is whether a country can still keep its most mobile of capitals in its yard.

How the UK's tax competitiveness problem has now become more than a mere tax policy problem

The debate is very much oversimplified: as if the message should be that rich people like to pay less tax. In fact, the real debate is more subtle; the current argument is that rather than responding to any given policy measure, mobile actors respond to a collection of signals, which have been overwhelmingly negative since 2024. Britain has phased out the remittance basis tax regimes from 6 April 2025 by implementing a residence based a tax regime, with a four year window for foreign income and gains to do business in if you entered the country as a non, resident; from 30 October 2024 capital gains taxes increased for most assets from 10 and 20% respectively to 18 and 24%. From April 2025, carried interest moved to a single 32% rate and then to a new income tax structure from April 2026. Although it's very true that no single actor determines the long-term course of a country, they are significant signals. And countries are listening.

Therefore, France should be viewed separately. Europe's competitive edge is so significant at present that a heavier UK tax load would be irrelevant. And that is one of the exceptions that prove the rule. The bigger point is that the UK has given a message, post-2024, of what it is willing to do by way of taxing ICT, multi-millionaires and even the residually domiciled, more than it can. And this cannot be interpreted as an overall neutral investment signal. It is one of many signals that are being sent, which can only be interpreted as: you can charge me more, but can I take my wealth with me? Like any strategic message, that one will be factored in smoothly or elsewhere long before it shows up on the bottom line. So, if the message is that no place is better to build from than Britain, then the options are known well in advance.

That is the problem with believing it only takes education. Britain does not have to gamble everything and the existence of Oxbridge and the legal class will match its other larger long-term tax signals. Holding on to mobile capital depends on at least three factors. Relativity of the clusters of advantage, the permanence of the offer and the narration of the guide. The more schools, advisors, investors and companies move elsewhere, the less they will be inclined to settle in the remaining economy. And this is where the education story follows on from, not where it leads. And this is why the UK does not need to give the farm. Giving the tax boost to relatively well-connected capital requires a more positive story in which location optimism can thrive. This requires clarity: predictability, simple messages, fewer mixed messages, a clearer medium,term roadmaps, a smoother process of acquiring visas and an immovable story that sets out a warm vision of how the opening race for growth will be ahead of the present politics of the election.

How has Dubai become the largest target city?

To many, Dubai is still regarded as only a sunny climate plus a bag of light taxes. That perception is a thing of the past. A high-tax country cannot just tweak its rate schedule by decree, but a nation offering light taxes can build a more solid platform for aspiring businesses and families. As revealed by a report from the DIFC Funds Center, Dubai has been talking about building its assets and wealth management business for a long while. The headline-grabbing rapid growth of Dubai International Financial Center, an intrinsic strength of what stands behind the city as a regional premier financial hub, rather than merely popular lifestyle terminology, is visible in the density of institutions and related proxies. In the 2025 report, the DIFC announced that over 1,200 families and related entities and over 1,200 foundations had migrated to the region with respective annual growth rates of 61 and 67% each. This is not merely a piece of dust members to a sunny landing spot, but indicative of a long-term organizing hub of intergenerational wealth. Family offices, independent consulting firms and other sophisticated private wealth assemblies do not gather opportunities over hours. They hubs when a city begins to appear in the eyes of the world as a long-term international hub.

However, Dubai's rise is not without risks. The fear over the Ukraine and Iran conflicts has created a tangible fear for the Gulf club era. Last week, the IMF lowered its 2026 forecast for the Middle East & North Africa to a modest 1.1%, well below its previous newsletter expectations, a direct demonstration of the knock that this conflict has had on shipping, energy infrastructure and output. It is a natural worry if hostilities endure that some options are beginning to look painfully slow or too risky. But it is a scare that should be avoided, since geopolitics can easily divert capital flows, but it does not necessarily mean they stop. The trendline remains powerful: for hundreds of mobile British families and capital owners, Dubai is still the preferred comparison since it involves the broadest weave of tax certainty, global access, wealth, energy and international influence. It is closer, surely, but that does not make it less enticing.

What should not matter to Britain if education is a 'reporter's secondary story'

The greatest danger is not the pollution of the roads with the horses on the way out. It's a gravitational outflow of layers of wealth: first to the families, then to the managers, then to the investment choices, then to the infrastructural bases enjoying their presence, then to the cities benefiting from their choices. an. According to S& P Global, pressures on private equity measures over time can and are likely to translate into wider gaps in the capacity of countries to drive new private financial flows, attract new business know-how, stimulate additional consumer activity and attract additional talent. The impact on higher education is likely to take place later, once the wealth has already become concentrated in certain places, as opposed to leading the way. It is not that it is not relevant, but that it will follow the drives and flows.

And this matters because British responses are too often built on a premise that prestige gets you everything. Britain assumes that its legend, its prestige, its history, its universities, or its institutions will make this unquenchable. But the evidence implies otherwise. And it is not just about prestige. It is about a larger expectation. International investors would like to know whether or not it is going to be easier or harder to build the long-term future from any particular place. That is when the answer starts to tilt toward the harder candidate; the decision is already made far away from the data. And this is the insight I want to return to time and again throughout articles about tax responsiveness: countries are not different because owners are not working in empty space. The real story in Britain has nothing to do with the fact that they will now be taxed more, but that they will now be taxed more in a world that has become consumed by unpredictable signals. The Britain.com agenda for the G20 now is: the UK government has suggested that it wants to ensure its tax system is 'fair' and 'internationally competitive' and that this will be achieved by 'personally incentivizing talented individuals to attract the investment that supports economic growth.' What is this conception of Britain's tax competitiveness in comparison to Dubai, Singapore, Switzerland, or Abu Dhabi?

What then should the tax competitiveness of the UK be compared against?

Britain does not need to be in a competitive race to the bottom, squeezing every state institution to the demands of private equity firms and billionaire households. But we do need an honest conversation about the trade-offs here. When a state raises its tax burden, it need not be surprised if more of that capital becomes mobile. If investors are willing to pay higher fees and charges, they must also be offered a set of attractive locational factors and incentives, which include increased certainty, fewer mixed messages, faster visa processing and an absence of more political than practical considerations. A country's competitiveness need no longer be read as a call for lower taxes. Instead, it is the country's strategic question: are you still providing an attractive enough set of reasons for corporate owners and wealthy households to remain? That is surely the key determinant of Britain's long-term future competitiveness.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Bilicka, K., Patel, E. and Seegert, N. (2026) ‘Why firms’ responses to corporate taxes differ across countries’, VoxEU, 8 April.

Dubai International Financial Centre (2026) ‘Dubai International Financial Centre announces landmark annual results for 2025’, 5 February.

Henley & Partners (2025) Henley Private Wealth Migration Report 2025. London: Henley & Partners.

HM Revenue & Customs (2024a) ‘Carried interest: rates of Capital Gains Tax’, policy paper, 30 October. London: HM Revenue & Customs.

HM Revenue & Customs (2024b) ‘Changes to the rates of Capital Gains Tax’, policy paper, 30 October. London: HM Revenue & Customs.

HM Revenue & Customs (2024c) ‘Reforming the taxation of non-UK domiciled individuals’, policy paper, 30 October. London: HM Revenue & Customs.

Ranking News Editor (2026a) ‘National Competitiveness Indices and Their Role in Economic Policy Reform’, Ranking News, 16 March.

Ranking News Editor (2026b) ‘When Cities Compete: How Urban Rankings Influence Global Investment Flows’, Ranking News, 16 March

Reuters (2026) ‘IMF slashes growth forecast for Middle East as Gulf exporters reel from impact of war’, 14 April.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.